FX intervention: A monetary, macro-prudential or mercantilist policy?

- 8 February 2021

- FX Switzerland

On a day in which the Bank of Israel announces a staggering $6.8bn of FX intervention in January alone, we review some of the factors driving this activity and look at how the theme of FX intervention will develop through the year. We suspect the new US Administration will have little tolerance for those they believe are preventing an orderly $ adjustment

2021’s early movers

In our prior article on this subject, we highlighted how Sweden, Chile and Israel had all pre-announced FX reserve building programmes for this year.

In fact, Israel has today announced that in January alone it spent $6.8bn of its $30bn full-year programme. We have also seen the Reserve Bank of India Governor Shaktikanta Das outline that emerging nations, in order to mitigate global spillovers, ‘have no recourse but to build their own FX reserve buffers’.

This broader concern of FX reserve adequacy firmly sits in the macro-prudential bucket of reasons to increase FX reserves – similar to the rationale that Chile announced in early January. But when it comes to FX reserve building, which countries can really justify reserve adequacy considerations and when does it cross into a more mercantilist measure to protect local exporters? In fact, Israel even admitted that FX intervention was partially designed to protect exporters and prevent import substitution.

Below, we look at a couple of FX reserve adequacy metrics to identify which emerging countries have the most – and least - justification for an FX intervention programme.

Emerging market FX reserve adequacy: Does India have a case?

For emerging market economies, FX reserves play an essential role in sovereign credit metrics as their currencies do not benefit from reserve currency status and many public and private creditors tend to borrow in foreign currencies, primarily the US dollar and euro.

Thus, adequate FX reserves are key to ensuring financial stability (notably the ability to ease pressure on the exchange rate in times of shocks) and provide confidence in a country’s ability to repay FX-denominated debt. Notably in early 2020 when the pandemic triggered a broad-based currency depreciation in emerging markets, we have seen many central banks stepping in to support their currencies, resulting in a drop in FX reserves. Nonetheless, most central banks have since been able to rebuild FX reserves in a prudent manner and thus for most countries, FX reserves have increased in 2020 (by an aggregated +4.4% for the 22 emerging market economies we have included here).

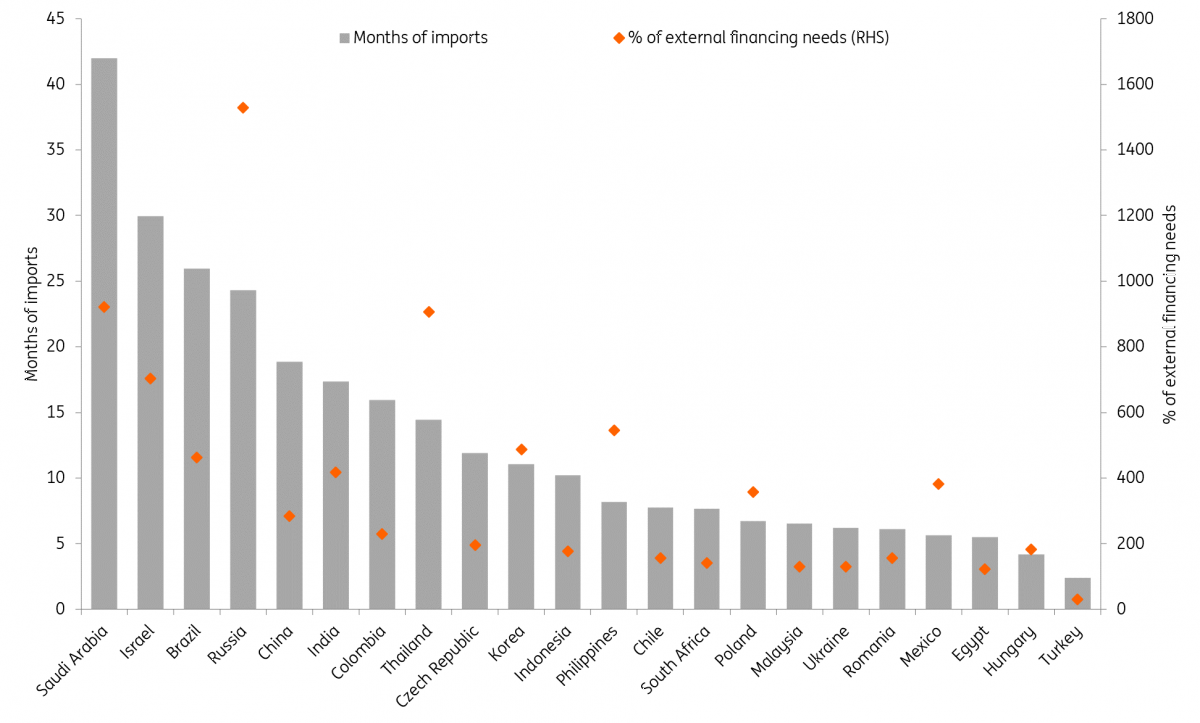

Two commonly-used metrics to compare FX reserves are three-months’ worth of import cover while the second is the percentage cover of external financing needs

Below, we look at two commonly-used metrics to compare FX reserves (based on IMF figures on total reserves excluding gold for December 2020) and note a stark divergence across emerging markets economies.

The first is the adequacy metric of three-months’ worth of import cover while the second is the percentage cover of external financing needs. On the latter,i a 100% coverage of short term external debt and the current account deficit is commonly seen as an important metric.

Among the countries mentioned above that have pre-announced a boost to their FX reserves, we find that India and Israel are among the countries with arguably the amplest FX reserves, thus any claims (e.g. India) to build reserves for macro-prudential measures may come under scrutiny from Washington. Others in that category include Brazil, China, Russia, Saudi Arabia and Thailand.

India and Israel are among the countries with arguably the most plentiful FX reserves

In contrast, we believe there is a need for Turkey to rebuild FX reserves (which have fallen by 46% over 2020 and only cover c.30% of external financing needs over the next year). Egypt and Ukraine, both frontier markets, have committed to gradually rebuild their FX reserves under their ongoing IMF programmes. Meanwhile, Hungary and Romania have relatively low reserves but benefit from their close ties to Eurozone countries (reflected also by the repo lines with the ECB). In the case of Chile, some prudence is also warranted given the drop in FX reserves last year and political uncertainty ahead of the constitutional convention and general elections.

Positively, we see a window of opportunity to improve external resilience through higher FX reserves, thanks to our view of a broad-based weaker dollar in 2021.

EM FX reserve adequacy: Import cover and short term external financing needs

Whisper it, what about reserve adequacy in the G10?

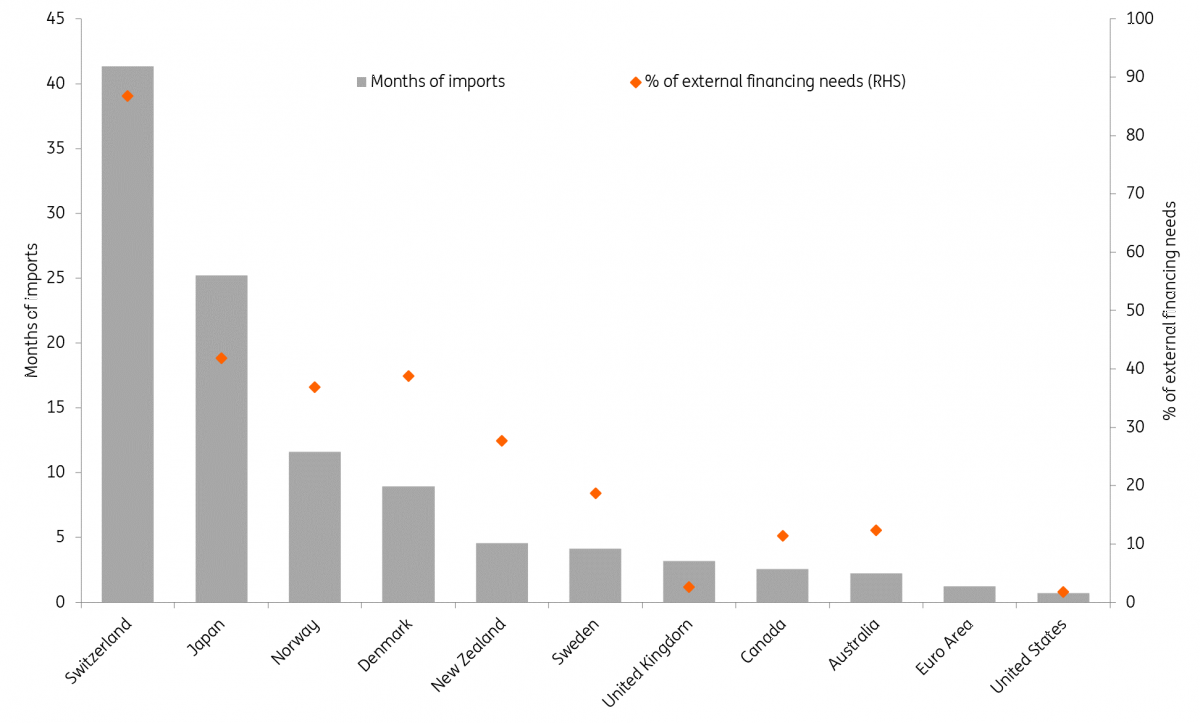

Away from the heavily interventionist Switzerland, already named a currency manipulator, what are the chances of other developed market central banks concluding that their FX reserves are too small and starting FX intervention programmes – useful if they would like to slow local currency gains through this early part of the recovery cycle?

Second-tier reserve currencies, such as those issued by Australia, New Zealand and Canada would find it a tough sell marketing the view that they needed higher FX reserve levels for macro-prudential measures

We would say that those second-tier reserve currencies, such as those issued by Australia, New Zealand and Canada would find it a tough sell marketing the view that they needed higher FX reserve levels for macro-prudential measures. These countries have some of the highest sovereign ratings in the world. And, for example, tight security relationships probably mean that these countries would be quickly ‘persuaded’ by the US that trying to fight this broad dollar adjustment was not in their interest.

The chart is also a reminder that the US and the Eurozone have tiny FX reserves – a reflection of the ‘exorbitant privilege’ of issuing the world’s top two reserve currencies. It would be a huge step for either side to undertake a reserve-building programme – although there was talk of US Treasury FX intervention when the dollar was very strong in 2018/19.

DM FX reserve adequacy: Low for a reason

Reserve building as an extension of monetary policy

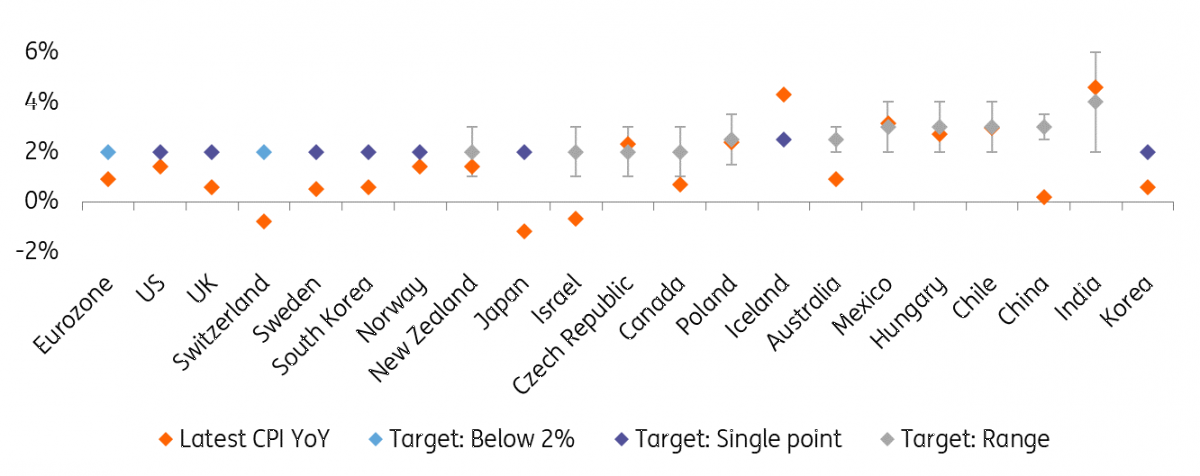

Massive FX intervention by both Switzerland and Israel falls under their auspices of monetary policy – both long sufferers of deflation.

As we highlight below, that line of justification will not be open to all. For example, India would struggle to market FX intervention from a monetary policy angle, where inflation is already above target.

This topic is also relevant for the ECB, where EUR/USD strength was seen adding to the Eurozone's travails with low inflation. Indeed, the idea has recently been floated that the ECB could cut the depo rate if EUR/USD were to rise too quickly. But the idea of the ECB building FX reserves to slow the EUR/USD advance looks far-fetched - especially in a year when Washington will be very sensitive to trading partners taking advantage of US fiscal stimulus and consumption with under-valued currencies.

Also in this section, one could assess the activity of Polish authorities, intervening to buy EUR/PLN in December in spite of Polish inflation broadly being in line with the target. Incidentally, the IMF has just said that Poland needs to explain what it is trying to achieve with its FX intervention - many think Polish intervention at year-end was actually designed to increase the value of Poland's FX reserves for budgetary purposes.

Inflation versus target: Which countries can justify intervention on monetary grounds?

Washington watches

We are bearish on the dollar this year and think that Washington will be very active in its surveillance of FX policies undertaken by its trading partners.

A lot of the US legislation written behind the US Treasury’s currency manipulation report was done so exactly for a year like this – a year in which the dollar is undergoing an orderly, market-led decline and trading partners, through FX intervention, maybe looking to interfere with that adjustment.

We are bearish on the dollar this year and think that Washington will be very active in its surveillance of FX policies undertaken by its trading partners.

That is why we think USD/Asia FX intervention over recent months looks to be more characterised by ‘smoothing’ or ‘liquidity adding’ rather than trying to defend any line in the sand.

And we’re interested in how developments proceed with Switzerland. The Swiss wholeheartedly reject accusations of ‘currency manipulation’, but let’s see how negotiations proceed between the two. We suspect the Swiss will be hoping that a pick-up in the world economy can unwind some of the market’s pre-cautionary CHF longs bought during the height of the trade war – meaning that little Swiss central bank FX intervention will be required after all.

Overall, however, we suspect the political environment means that reserve managers will only be able to slow, not reverse local currency appreciation against the dollar this year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

The only way is up, baby

- This bundle contains 8 Articles