From grass to glass: The future for dairy companies on the path to net zero

- 21 March 2024

- Commodities, Food & Agri Sustainability

An increasing number of large dairy companies have plans to become net zero in the future. Measures on farms play a crucial role in reaching targets but often raise costs for farmers. Paying out a sustainability premium of a couple of cents per litre of milk to farmers would make a difference, but dairy producers struggle to pass on such premiums to customers

CO2 reduction targets are now commonplace in the dairy industry

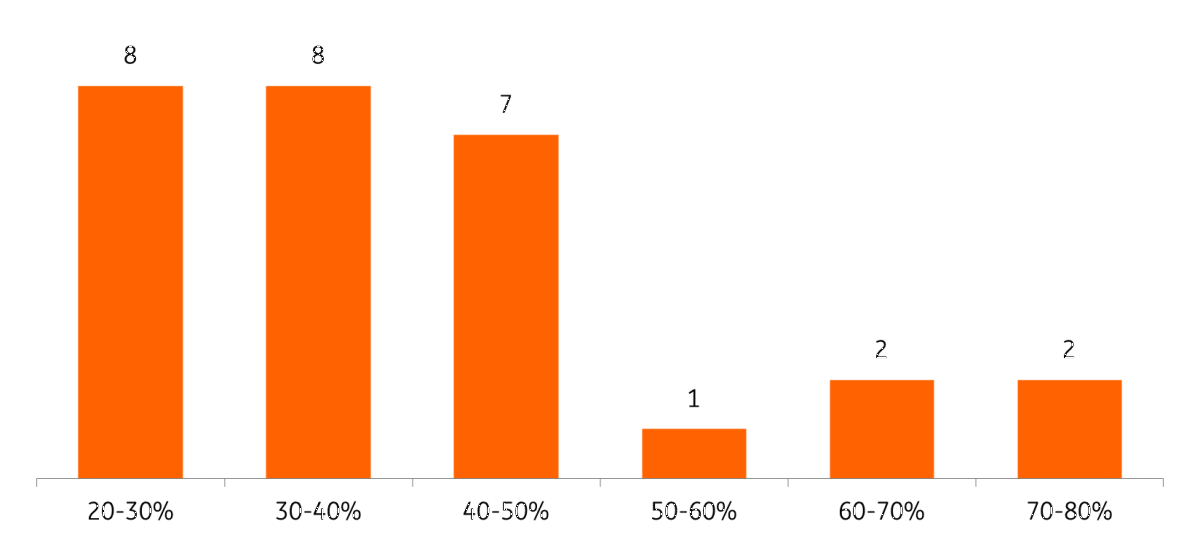

CO2 reduction targets have been widely adopted in the global dairy industry. Among the 30 largest dairy processors in Europe, North America, New Zealand, Australia and China, almost every company has communicated a CO2 reduction target for their own operations (Scope 1 and 2). On average, dairy companies aim for a 38% reduction in 2030 compared to 2020. Still, there are large differences between companies. Some only briefly mention their targets, while in other cases, targets have also been submitted to and validated by third parties. The same is true for underlying strategies, which range from being quite concise to very elaborate.

Major dairy companies usually have a carbon reduction target for their own operations that ranges between 20% and 50% in 2030

Number of companies ranked according to their scope 1 and 2 emission reduction, compared to a 2020 base year

If dairy processors want to become net zero in 2050, they need to look beyond their own operations; around 95% of the greenhouse gas emissions from dairy products happen either upstream or downstream in their value chain (Scope 3). Emissions on farms in the form of methane (enteric fermentation, manure), nitrogen (fertiliser use) and carbon (land use change, energy use) are the predominant factor and account for 65% to 80% of all the emissions from grass to glass.

Currently, two-thirds of the 30 dairy companies in our selection have a target for their value chain (Scope 3). In many cases, these are intensity targets, meaning that companies aim to reduce their emissions per kilogram of milk. However, just steering on intensity targets can create tension with national emissions targets for agriculture that require an absolute reduction. We also see absolute targets gaining traction since they’re often required by the Science Based Targets initiative (SBTi), a non-profit that supports companies in establishing targets aligned with climate science.

Most emissions in the life cycle of dairy products arise at beginning of the value chain

Schematic breakdown of emissions from the perspective of a dairy processor

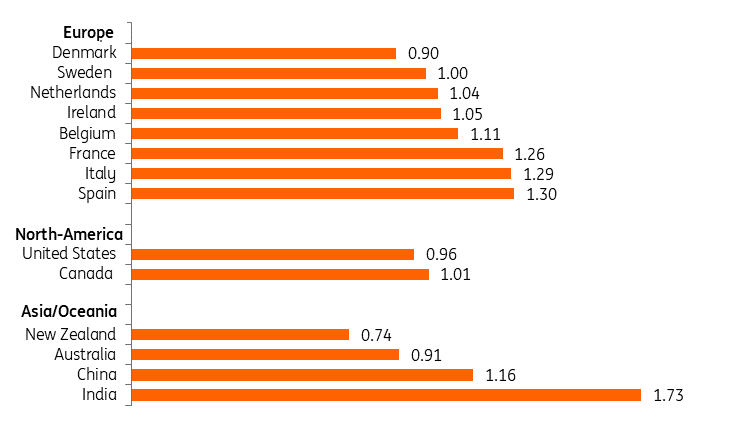

It takes about a kilogram of CO2 to produce a kilogram of milk in key dairy regions

The carbon footprint of producing a kilogram of milk is a key metric for both dairy farmers and processors and is increasingly being used as a benchmark. Countries with a relatively low number generally benefit from factors such as their favourable climates, sophisticated farm management practices and advanced animal breeding. Dairy farms in countries like New Zealand and Ireland operate in an extensive grass-based system and require less external input. On the contrary, dairy farms in the United States, China and Denmark operate in a more intensive system and manage to reduce their footprint by achieving a higher milk output per cow. Both systems offer opportunities to reduce the carbon footprint but also have limitations.

We'll be focusing on carbon emissions in this article, but aspects like animal welfare and biodiversity are also important features in sustainability strategies. Making progress on these fronts can sometimes be at odds with lowering emissions.

Producing milk is more carbon intensive in some countries compared to others

Emissions, in kilogram of CO2 equivalent, associated with the production of a kilogram of milk (fat and protein corrected) in main dairy producing regions

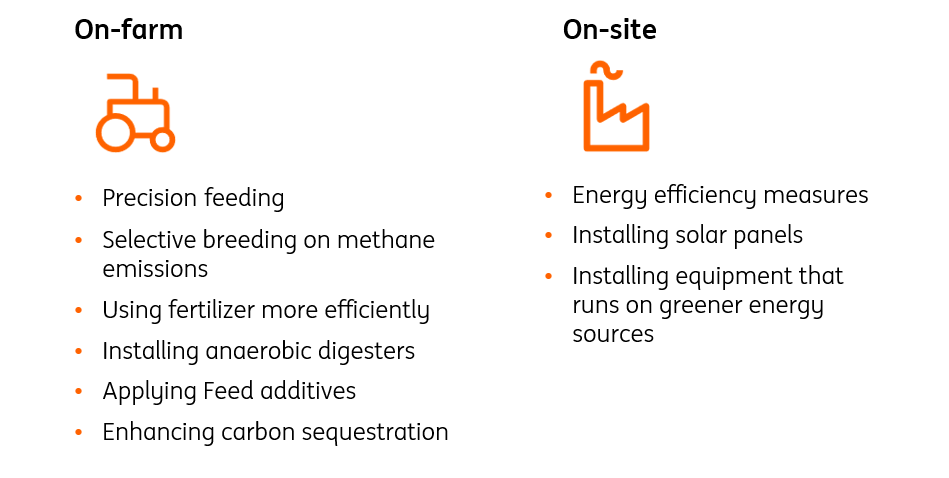

Feed, animal health and manure management are key areas for on-farm measures

Scientific studies mention around 150 individual measures that farmers can employ to decrease the carbon footprint of milk production. These on-farm measures are usually clustered in three broad groups: feed production and efficiency, animal health, and manure management.

The effectiveness of various measures largely depends on individual farmers and their local situations. Dairy farms vary greatly in size, with some housing just 20 cows and others accommodating over 5,000. On top of that, there are other differences, such as geography and location, farmer characteristics (such as age), and regulations. Regardless of these differences, all farmers have opportunities to reduce the footprint of their milk by being as efficient as possible in growing and applying animal feed, ensuring that their herd is in optimal shape over their full lifespan and managing manure and fertiliser use. However, these improvements often come at a cost, whether financial or in terms of time and specific skills required

Examples of carbon reduction measures that can be taken on dairy farms and in processing plants

Spotlight on feed additives, anaerobic digesters and carbon storage in soils

In this section, we look into three types of measures that are getting a lot of attention in the industry and describe their status, potential and costs.

1. Feed additives: the proof of the pudding is in the eating

The range of feed additives that help to reduce methane emissions from (dairy) cattle is growing. Companies in all the major dairy regions are looking into this, although they acknowledge that additives tend to be less effective in pasture-based systems. Some European companies are currently scaling up their initial pilots with Bovaer from dsm-firmenich and several companies (Danone, Groupe Bel, Norwegian Q-Milk) already market milk products from cows that received Bovaer. Expectations in the dairy industry are high since additives can potentially reduce the carbon emissions of producing a kilogram of milk by 10-15% at a relatively low cost. But the roll-out will be step by step. We believe 2025 will be a crucial year because dsm-firmenich expects to have the capacity by that point to supply Bovaer to five million cows. As a reference, that would be enough for a quarter of the EU dairy herd.

Operational costs are the main hurdle here. On a typical dairy farm in the Netherlands (with 75-165 dairy cows), using such additives would raise costs by 4,000 to 10,000 euros, which is a 1% increase in total costs.

2. Greater roll out of anaerobic digesters hinges on government support

Anaerobic digesters provide an effective way of reducing methane emissions from manure. While the numbers are growing, they’re still operating at a limited number of dairy farms. In the US, there are approximately 425 digesters on dairy farms out of a total of 24,000. Transporting manure from a cluster of dairy farms to a bigger centralised digester is another option. The integration of biodigesters on dairy farms – especially the larger ones – is quite common in Denmark and California thanks to consistent policy support in the form of subsidies for green gas producers and/or blending obligations for energy companies. Meanwhile, several countries including France, the Netherlands and Ireland have ambitious plans to increase production of biomethane (also known as renewable natural gas) to replace natural gas. For dairy farmers in countries like France and the Netherlands, digesters provide an opportunity to reduce emissions from manure. In Ireland, it’s not really feasible to have digesters on dairy farms since cows tend to be outside a lot. An increase in the availability of biomethane could benefit the dairy industry by unlocking a cleaner energy source for their processing facilities and trucks. Apart from that, the digestate can be an alternative greener source of fertiliser for farmers.

Both the initial investment and higher production costs for biomethane can be major hurdles for the take-up of biodigesters. In Ireland, production costs of biomethane are estimated to be two to four times higher than the current cost of natural gas. On a typical Dutch dairy farm, the investment would be around half a million euros, assuming that other infrastructure such as a modern barn is already in place. The actual amount also depends on the size of the farm and the type of digester. California provides a good example of how hurdles can be lowered by supportive policies. In California, the capital investment for constructing a biodigester on a farm with 2500 cows is estimated at eight million euros. Revenues for Californian dairy farms include the selling price of the gas but the majority of the revenues comes from credit generation under the states Low-Carbon Fuels Standard (LCFS) program federal Renewable Fuels Standards (RFS) programmes.

3. Storing additional carbon in agricultural soils: easier said than done

Given that some emissions are unavoidable in dairy production, enhancing carbon sequestration on farms is often seen as a necessary step to offset residual emissions. However, there are three main challenges to this approach:

- The permanence of additional stored carbon is a challenge. Carbon stocks in soil are inherently dynamic, and soil carbon is often partly released when farmers cultivate their land.

- Proving that certain activities (or refraining from some activities) have led to additional carbon stocks provides another challenge.

- In some places, like New Zealand and the Netherlands, carbon levels in grasslands are already quite high, making it difficult to raise levels further.

This means that the main opportunity for storing additional carbon soils lies in (depleted) agricultural land where farmers grow feed crops and in planting trees and hedges on non-productive land.

In the US and Australia, policies and accompanying frameworks already enable farmers to sell carbon credits in voluntary carbon markets. Still, according to S&P current carbon prices in these markets are generally too low for soil carbon projects to be profitable. A complicating factor for the dairy industry is that when dairy farmers take action, generate credits and sell these credits to companies in other sectors, they’re no longer contributing to carbon reduction efforts in the dairy sector.

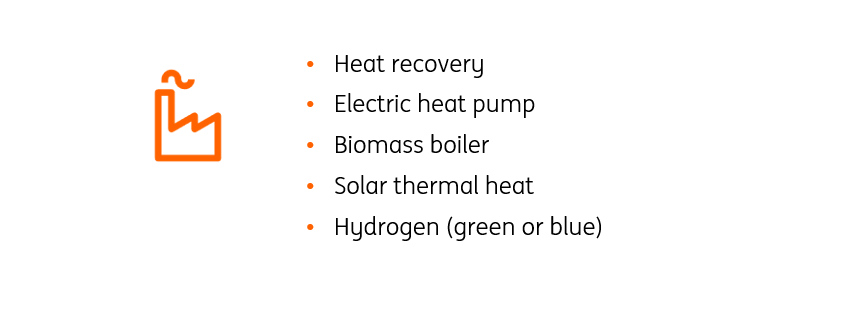

Reducing energy use and the switch to green energy

Emissions in dairy processing facilities are mainly linked to the energy used to make anything from UHT milk to infant formula to cheese. Improving energy efficiency and greening the remaining energy demand are key elements in determining the way companies approach their Scope 1 and 2 emissions.

On-site solar panels provide the default option to generate part of the total electricity demand. The remaining part can be covered by power purchasing agreements for green electricity. Moving away from gas, oil or coal to produce heat requires more of a tailor-made approach, because every processing facility has a different starting point in terms of age and types of products that it makes. In many dairy plants, processing milk into a dry powder (spray drying) is the most energy-intensive process. Many companies are now looking at ways to reduce emissions from this process.

For example, Lactalis, a French dairy company, recently switched from gas to solar thermal heat at one of its production sites. In the Netherlands, both FrieslandCampina and Nestlé announced investments in heat recovery equipment to reduce gas usage in their spray dryers. Meanwhile, Arla is investing 30 million euros in an electric heat pump at one of its sites in Denmark, and German dairy company Meggle opts for hybrid equipment that could run on hydrogen instead of gas at its site in Bavaria.

There are different routes to reduce emissions from heat demand at dairy processing sites

Rewarding farmers for their work

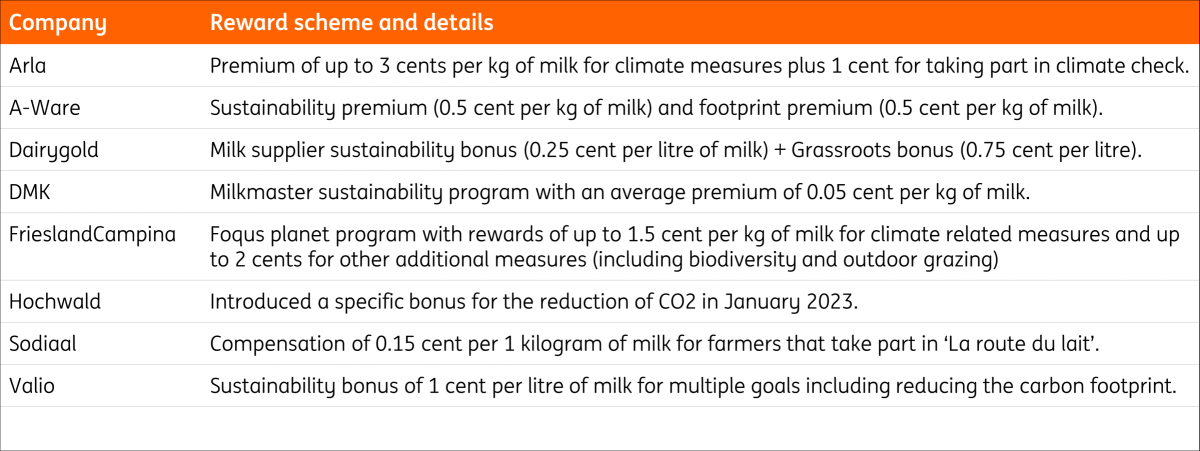

The challenge for the dairy industry lies in securing farmer cooperation. After all, if farmers can’t minimise their environmental impact, dairy companies won’t come anywhere near their net zero targets. The rise in corporate goals for carbon reduction and other sustainability-linked KPI’s provides dairy farmers with more bargaining power in discussions with their cooperatives or processors. As a result, we see growth in sustainability reward programs that include financial incentives for farmers. Dairy companies in Scandinavia and Northwestern Europe seem to be more successful in getting such sustainability premiums from the market. This is not surprising given the higher consumer purchasing power in their ‘home markets’.

A selection of sustainability related reward schemes from European dairy companies

Communicating sustainability efforts towards customers

The market for many dairy products is global and heavily commoditised, so companies that work with sustainability rewards for farmers need to pass them on to customers to remain competitive. They can do so in two ways.

- Dairy companies are looking to deepen partnerships with B2B customers. Partnerships between dairy processors and customers like FMCGs, retailers and foodservice companies are crucial for carbon reduction measures since they often depend on long-term commitment. What helps drive conversations is that more and more customers are setting or extending their CO2 reduction targets. Many large customers expect their (dairy) suppliers to reduce their emissions in line with their own targets. As a result, corporate customers will be looking for milk produced within a range of 0.6 to 0.8 kilogram of CO2 equivalents per kilogram in 2030. Dairy companies or regions that can offer milk with a low footprint have a competitive advantage.

- Product innovation can support efforts for a lower carbon dairy industry. Dairy companies often communicate with consumers about the full package of their sustainability efforts, including aspects such as animal welfare and biodiversity. By itself, carbon reduction is not a key driver in purchasing behaviour of consumers. Aspects such as price, taste and health are far more important. Still, some companies have included carbon reduction efforts (in this case, the use of feed additives) in the value proposition of their products.

Another route is through a shift in product portfolios. New Zealand dairy company Fonterra recently reported that emissions fell in 2023, in part because increased volumes of lower emission products such as UHT milk. While this was not deliberate and was likely caused by consumers trading down, it shows that shifts in products sold can have an impact on company emissions. The challenge here is to find opportunities that are also attractive from a commercial perspective.

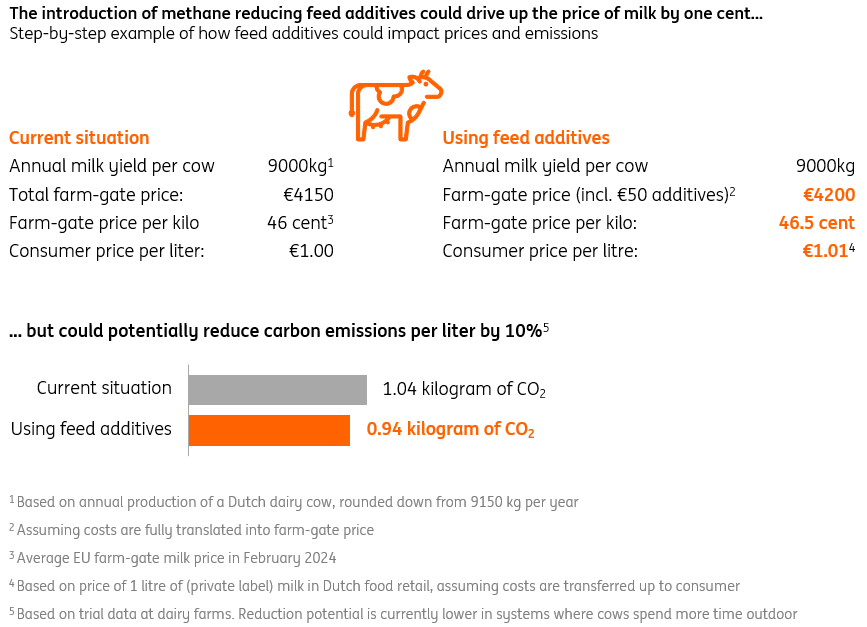

Will efforts from the dairy industry have an impact on consumer prices? We believe so, as they requires investment and efforts at both farms and at production facilities. While some investments might result in cost savings, this isn’t always the case. On balance, carbon reduction measures have an upward effect on production costs and prices. The case of feed additives provides a good example (see visual). However, since dairy processors have a hard time in getting sustainability premiums from the market, we don’t expect any steep increases in consumer prices due to sustainability efforts in the near term.

The use of methane reducing feed additives could drive up the price of milk by one cent...

Step by step example of how feed additives could impact prices and emissions

Major steps have been taken, but many more lie ahead

Many dairy companies have taken an important step on the long road towards becoming net zero by setting targets for their own operations and their value chains. While some companies are still yet to follow that example, for most it will come down to acting on these targets in the years ahead. That means identifying opportunities and securing the capital investment to upgrade processing facilities. It's even more important to get large and diverse groups of dairy farmers to rally behind these goals. This will involve a lot of missionary work from dairy companies, including providing proper tools and incentives to farmers. It also means putting their weight behind policies that can stimulate farmers to take carbon reduction measures. The fact that global dairy demand will continue to grow will make it even more challenging to reach absolute reductions in agricultural and industrial emissions that are ultimately required to limit global warming.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more