French GDP fall estimated at 5.8% in 1Q

- 30 April 2020

- France

The first estimate of the French GDP contraction in the first quarter shows that the economy is likely to have shrunk by 5.8% from the previous quarter. However, the first estimate relies mainly on previously published surveys and does not shine much light on how the French economy performed during the lockdown

This is a first estimate

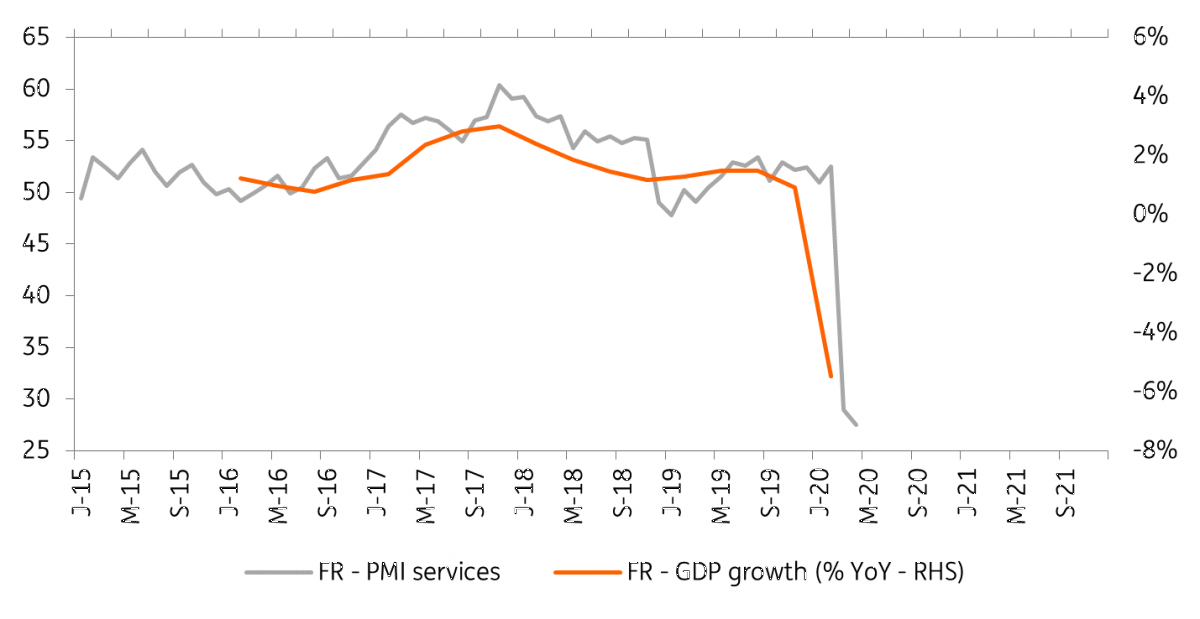

In France, first quarter GDP statistics are far from having revealed their secrets. We have only a first estimate, which indicates a contraction in GDP of 5.8% in the first quarter, slightly below the contraction observed in the second quarter of 1968, which was the strongest contraction since 1949. This figure is consistent with earlier INSEE estimates of an economy operating at 65% of capacity in the last two weeks of March. Consumers, confined to their homes, reduced their non-food purchases : consumption fell by 6.1%. Investments are also practically at a standstill (the drop is estimated at 11.8%), and import and export activities have also stagnated.

A nasty profile

This estimate is particularly fragile

The first estimate of GDP is based on partial data as the last weeks of the last month are always missing, which is a big problem this time around. Available surveys and econometric models generally allow a very accurate result despite the lack of data for the last weeks of the quarter, a result that is marginally revised thereafter. The current situation is of course peculiar and INSEE's methodological precautions provide more information than the result itself.

Data are complete only for some sectors (mainly industrial production, custom data, retail trade and energy). For services and construction, INSEE has estimated the activity during the lockdown according to its business survey (during the early days of the lockdown). Therefore, "these estimates can be interpreted as the drop in activity in the week from 23 to 29 March 2020 related to the lockdown measures taken on 17 March. In order to estimate the change over the whole month of March, the assumption used is that there is no year-on-year change on the first half of March and that the change is equal to the instantaneous drop in activity or consumption in the second half of the month measured in the Business Conditions Survey".

This means that the first estimate is largely based on the surveys carried out and published a few weeks ago and does not bring us much new information about what really happened outside industry during the lockdown.

This estimate is a valuable starting point

If only part of the estimate is based on new elements, it nevertheless has the merit of providing a reference point. Indeed, a major revision is to be expected, especially if the reality should prove to be different from what the surveys showed at the beginning of the lockdown. In fact, the scale of the current estimate revision will provide crucial information: did these surveys, which showed an economy operating at 65% of its capacity, reflect reality? If so, the estimates for 2Q20, and therefore for the 2020 contraction, will also be more accurate.

Thus, if the final figures confirm this first estimate, the gap in GDP compared to the level expected in 1Q20 (without lockdown) is 6.5%. This gap is expected to widen to around 20% in 2Q20, after an even greater contraction due to the higher number of weeks spent in lockdown in 2Q20 (six instead of two). This should bring total GDP growth in 2020 to around -9%, assuming a rapid recovery in the third quarter.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more