France: Measuring the shock

- 3 April 2020

- France

As France is approaching the peak of the epidemic, lockdown measures are maintained. PM Philippe signaled this week the way out would only be gradual. While the priority is rightly to save lives, the economic consequences can start to be measured

A wartime economic contraction

The latest opinion polls by Elabe showed this week that President Macron is back at his pre “yellow vest” crisis approval rating. In early April, 39% of the French approved his action, against only 31% in early February. The improvement is especially strong among the oldest (65+) and youngest (below 24). Other opinion polls show that the French are supporting the lockdown measures and have understood how they are alleviating the pressure on hospitals which, in some regions, are running out of space. The first regional mortality figures for early March are showing unusual results, with figures up by 40% compared to the same periods of the last two years in South Corsica and at the German border. In a speech this week Prime Minister Philippe explained that the way out of lockdown measures would only be gradual, talking about a “step-by-step” process depending on the acute health care beds occupancy, and the testing capacities. This process could start at the end of this month at the earliest.

Public finances take the hit

Given the dire economic situation, the Government is beefing up its response to the crisis: direct crisis spending will increase by 50%, from €11.5bn to €17.3bn, on top of the €35bn effort made in tax postponements. The new measures include €3.1bn for medical features, €1bn support for medical staff and €2.6bn more for temporary unemployment measures. These are expected to cost around €10bn per month, with 337,000 companies having applied to the scheme for a total of 3.6 million workers.

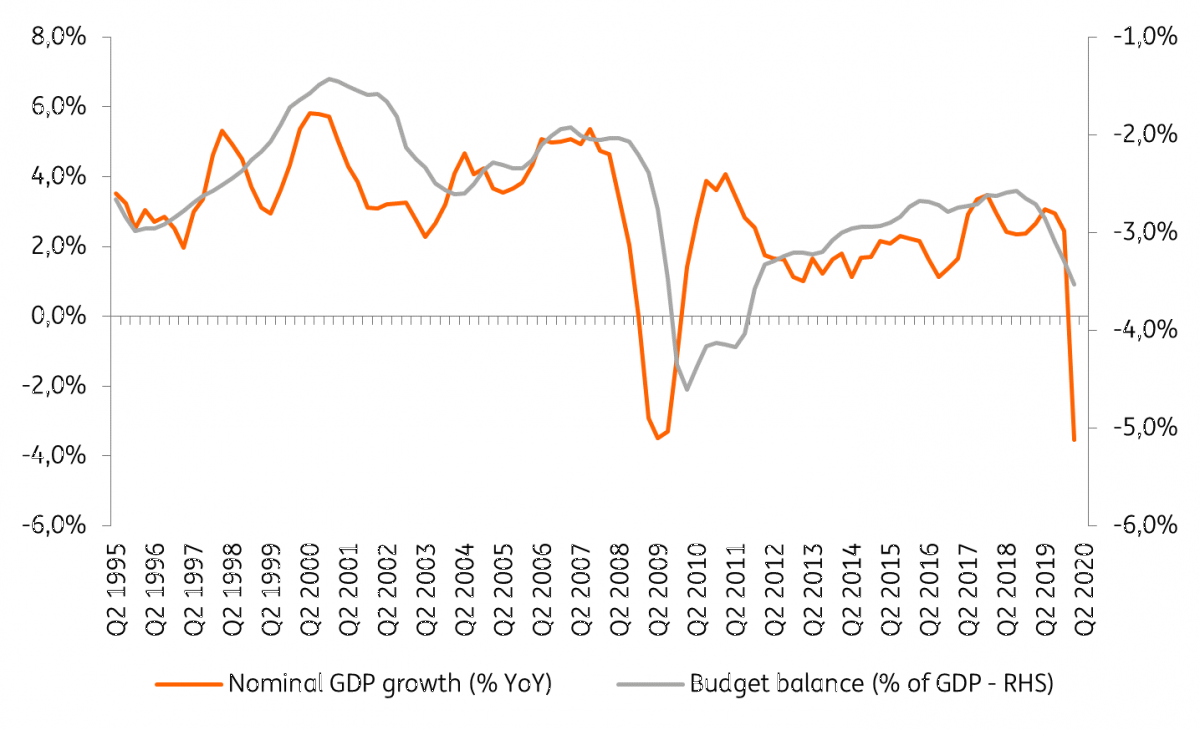

More spending, together with less tax receipts, low growth and low inflation are a toxic mix for public finances. While spending will increase to the tune of 8% this year, tax revenues are expected to decrease by more than 6% (with low energy prices, energy taxes alone should see a loss of €2bn to €4bn, and that is without counting the drop in VAT). With GDP contracting by almost 5% and an inflation close to 0% in 2020, the deficit-to-GDP ratio is likely to reach 5.3% while debt will end up close to 110%.

How Covid-19 will dent public finances in 2020

A virus-driven ice age

These figures confirm that like most developed economies, France has entered what we called “a virus-driven ice age” in our last Monthly Economic Update (available here). In these times, it's more difficult than ever to come up with adequate economic forecasts. The best we can do is to describe several possible outcomes, based on different scenarios regarding the length of the lockdown and the spread of the virus (to know more about ING scenarios, please refer to our last Monthly Economic Update (available here). What was presented here for France is in line with ING’s base case scenario which assumes a U-shaped recovery with a wide bottom, as social distancing and travel restrictions are likely to stick, even beyond the lockdowns. After a severe contraction of most economies in the first half of 2020, a decent recovery would follow, though most economies will likely only return to their pre-crisis levels in 2022. In more adverse scenarios, the return to pre-crisis levels could take until 2023 or even later.

Link to monthly eco update

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more