Fitch’s China outlook downgrade highlights a key fiscal dilemma

- 10 April 2024

- China

Fitch’s China outlook cut highlights the dilemma between fiscal spending or consolidation

Fitch's credit rating outlook downgrade highlights increasing concern over debt sustainability

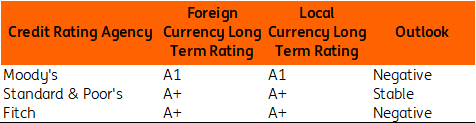

After the Moody's downgrade of China's credit rating outlook last December, Fitch followed suit with a downgrade of China's long-term foreign currency credit rating outlook. This move is unlikely to be a surprise to markets given the developments of the past several years.

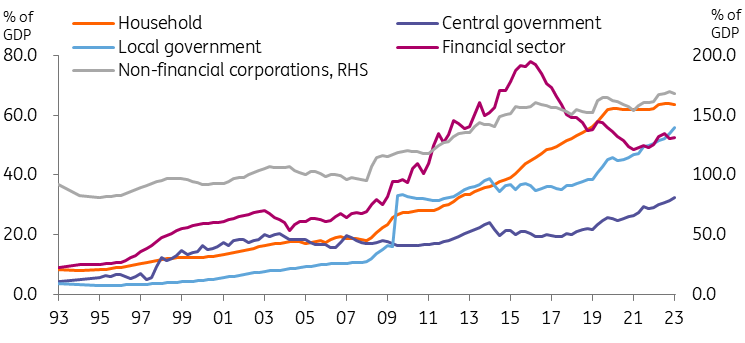

Government debt to GDP data often has significant variations depending on methodology, but in general we can observe that the debt situation has worsened rapidly since the pandemic. This has occurred on both sides of the equation – with rising government spending on anti-pandemic measures and with slowing economic growth. According to data from China's National Institution for Financial Development and Center for National Balance Sheets, the combined categories of general, central, and local government debt to GDP rose from 77.2% at the end of 2019 to 111.8% at the end of 2023. Other estimates, such as those from the Bank of International Settlements, put China's government debt to GDP at a more benign 81.2% of GDP.

The key factors behind the outlook downgrade include a wider fiscal deficit, risks from LGFVs, a slowdown of growth and a transition from the previous public financing model, which was driven by local governments which were heavily dependent on land sales. These factors have been discussed extensively by market participants over the last several years. Fitch noted that the central government would be shouldering a greater share of the fiscal burden, which will have the effect of raising its debt to GDP measure, which has been comparatively very low. In our view, one of the most important factors Fitch mentioned is an "uncertain consolidation path."

With fiscal spending likely to accelerate this year amid growth stabilisation efforts and a low probability of seeing meaningful fiscal consolidation measures before the outlook stabilises, it is possible that rating agencies take the next step from a negative outlook adjustment to an actual credit rating downgrade in the coming year or two – despite this year's official fiscal deficit targets being kept unchanged at a relatively cautious 3%. The last major wave of credit rating cuts were in 2017 for Moody's and Standard and Poor's, and 2013 for Fitch.

Typically after the adjustment of sovereign ratings, company level ratings will also be reviewed, and we could see similar moves in the coming weeks for outlooks on Chinese credit issuers.

China's long term credit ratings and outlook

China's fiscal dilemma: stimulate or consolidate?

The downgrade from Fitch highlights the dilemma that policymakers are facing. On one hand, there is certainly a need to support economic growth in the near term, and fiscal support in our view is important in order to avoid falling into a so-called "Japanisation" trap, where the economy enters into a negative feedback loop of weak confidence, falling asset prices, and slower economic growth. This will cause government debt levels to rise in the near term.

On the other hand, long-term fiscal consolidation efforts remain important. In China's case, finding a viable alternative for land sales is an important step to take in the medium term, but the obvious solutions to this – like increasing other taxes – are unpalatable at the moment given the current state of the economy. Nonetheless, the land sale driven model of government financing will also need to change as China's economy transitions.

In our view, long-term consolidation efforts might need to take a back seat to short-term stabilisation concerns, and the debt outlook could look worse before it looks better. Failing to restore growth and confidence would weaken the GDP side of the debt to GDP equation, and could have an equally harmful impact on long-term debt sustainability. However, it is important that fiscal spending from this point onward is directed toward productive areas of growth for the future. We expect that a portion of this investment will target strategic industries focused on the development of the green economy and the digital economy.

Some market participants have been discussing whether or not we will see Chinese-style quantitative easing, which could be a way to reduce the fiscal burden via lower borrowing rates and also support the markets. While it is possible that these policy tools will be added to the People's Bank of China's repertoire, Chinese sovereign yields are already comparatively low amid weak risk appetite, benchmark interest rates are still well above the zero bound, and the policy focus to stabilise the RMB at a reasonable and balanced level indicates that the odds of this coming into use in the near term are low.

China's government debt has risen rapidly since 2020

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more