Fiscal policy of next Dutch government probably expansionary

- 4 March 2021

- The Netherlands

Policy proposals by parties in the Dutch coalition government ahead of the 17 March election imply higher spending and lower taxation in the next 4 years, leading to a GDP impulse of 1.3%. Known for its after-crisis austerity, Dutch politics made a turnaround. Despite an increase, Dutch public debt will remain low compared to peer countries

Insights to the fiscal and economic effects of policy proposals of most Dutch political parties

It is common practice in the Netherlands for traditional political parties to submit their detailed policy proposals for the next term (up to 2025) of the House of Representatives to the independent agency called the Netherlands Bureau of Economic Policy Analysis (CPB). CPB will then subject the proposals to a viability check, estimate the fiscal implications and macro-economic effects. The results presented in the first week of March provide insights to the likely possible policy direction of the next Dutch government.

Most eligible parties decided to participate in this tradition in 2021. Only Geert Wilders’ PVV, Thierry Baudet’s FvD and Esther Ouwehand’s Party for the Animals decided not. We will discuss the size and effect of policies submitted by the parties that are in the current coalition government, which poll at 80 out of 150 seats (according to Peilingwijzer estimates based on polls of I&O Research, Ipsos/EenVandaag and Kantar as of 25 February 2021, with 73 to 87 seats at a 95% confidence level). This includes the liberal conservative VVD of Mark Rutte, Christian democrats CDA of Wopke Hoekstra, centrist liberal democrats D66 of Sigrid Kaag and Christian-social party ChristenUnie (CU) of Gert-Jan Segers. Although other coalitions and therefore another policy mix are also possible, this is difficult to predict, and we refrain from doing that.

We will weigh the results of these four parties by their estimated support. For example, VVD gets a share of 50%, since it represents 40 out of the 80 polled House of Representative seats within the coalition.

Also of interest might be our publication of what to expect from the Dutch elections, based on polls and election manifestos

Substantially more public spending in the medium term

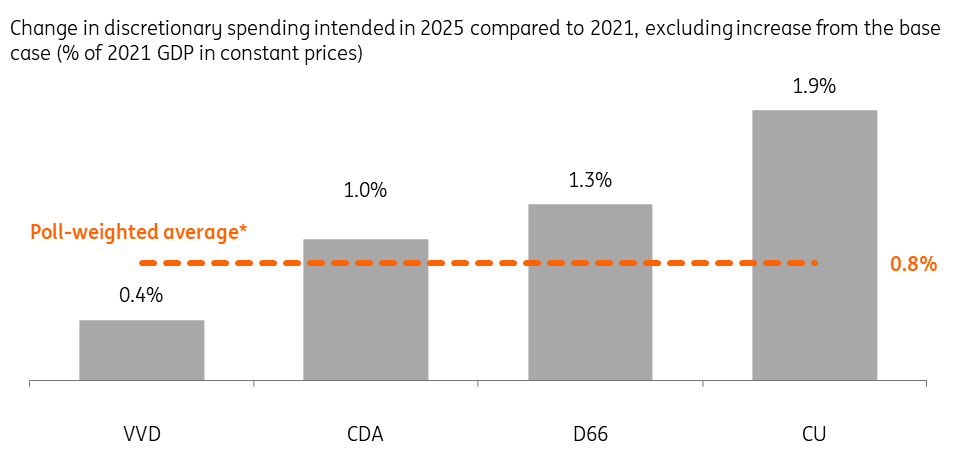

A continuation of the current coalition would probably mean expansionary fiscal policy. Government expenditures will probably fall compared to the Covid-19 inspired high level of spending of 2021, because temporary support measures will end. All parties will increase (real) structural spending during the next term (as measured in 2025). The net increase in spending varies from 0.4% of 2021 GDP (VVD) to 1.9% (CU). The poll-weighted average increase of the four governing parties is 0.8% GDP, a significant increase.

See this publication for economist views on fiscal policy in the Netherlands in times of Covid.

Increase in discretionary spending intended by all coalition members

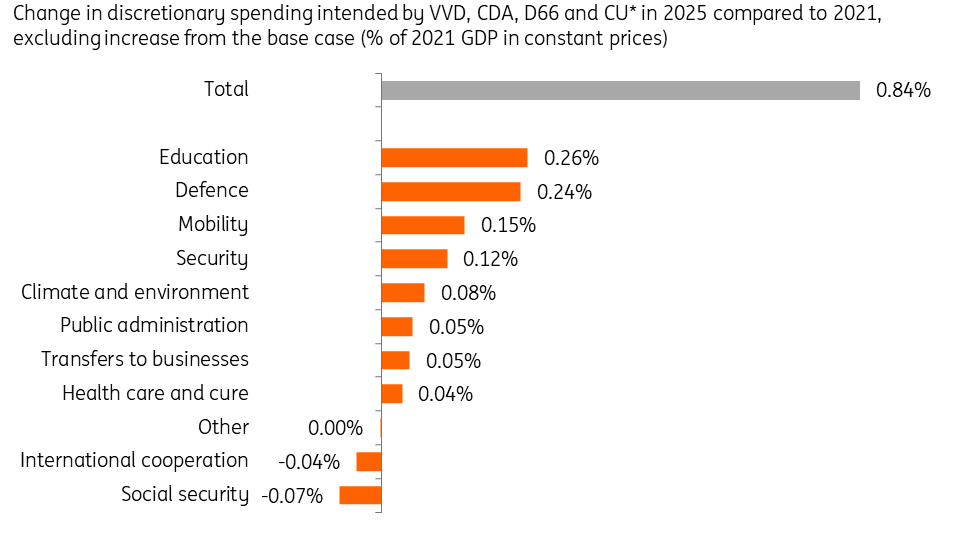

Higher spending especially on education and defence

No coalition party cuts spending on health care and all of them increase spending on education, climate & environmental policies, defence, security and mobility. Abstracting from temporary and trend (ageing) driven changes in spending (-1.2% GDP), the coalition parties intend to increase spending most on education, followed by defence and mobility.

The largest spending cut is applied to social security, but this very much depends on a complete overhaul of the allowance system, abolishing allowances for children, childcare, health care and rent. This would however be offset by lower taxation.

Largest increase in spending in education intended

No total agreement on direction of taxation, but a cut most likely for the current coalition

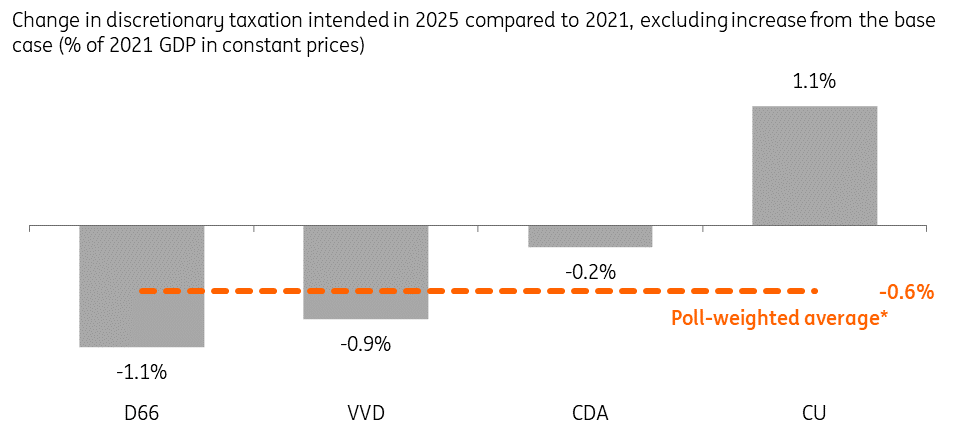

Coalition parties don’t fully agree on the direction of taxation. Without policy changes, taxation will increase by 0.7% of GDP, mostly due to ageing-related increases in health care insurance premiums. Abstracting from such base case effects, the intended change in discretionary taxation varies from a cut of 1.1% of GDP (D66) to an increase of 1.1% (CU, in part to compensate for lower allowances). The weighted averages of the change are a decline of 0.6% GDP, in line with the direction that three of the four parties intend.

Three coalition partners opt for lower taxation

Shift of tax burden towards wealth and businesses

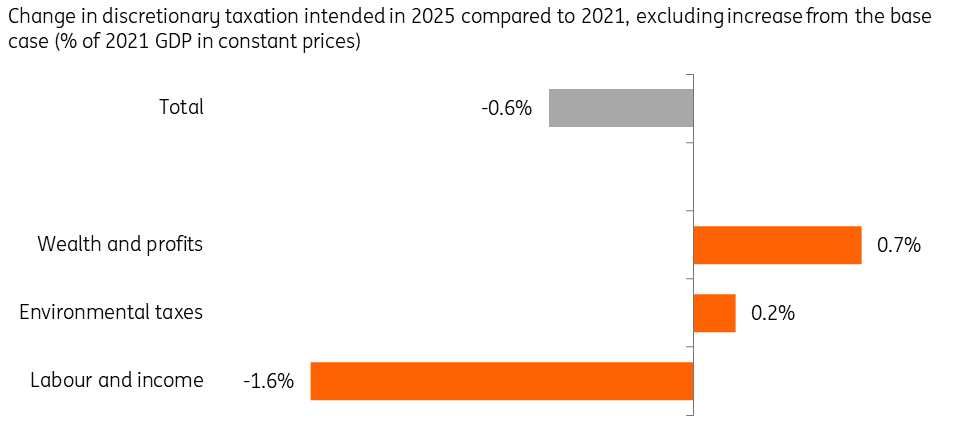

All parties intend to reduce the tax burden for households significantly: taxation on labour and income is in 2025 on (weighted) average 1.6% GDP lower than would be the case without policy changes. In part it is a shift of the burden to profits, wealth and pollution.

Lower tax partly financed by wealth, profit and environmental taxes

Agreement on looser fiscal policy in the medium term

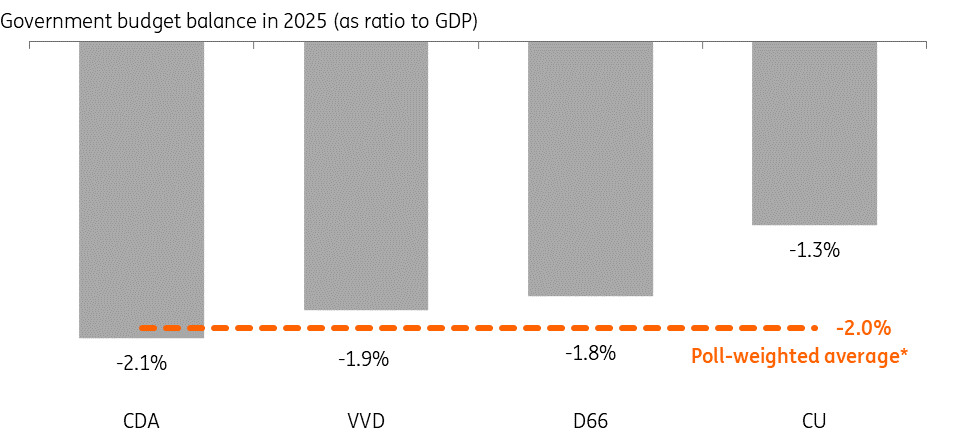

As a result of generally looser fiscal policy in the medium term, the government budget balance would decrease to between -1.3% GDP (CU) to -2.1% GDP (CDA) in 2025. The resulting estimated government debt levels in 2025 vary between 59.6% GDP (D66) and 61.7% GDP (VVD), which keeps the weighted average of 61.0% GDP very much within safe margins.

Government budget deficit in 2025 around 2% of GDP implies fiscal stimulus

Stark differences in long run debt projections

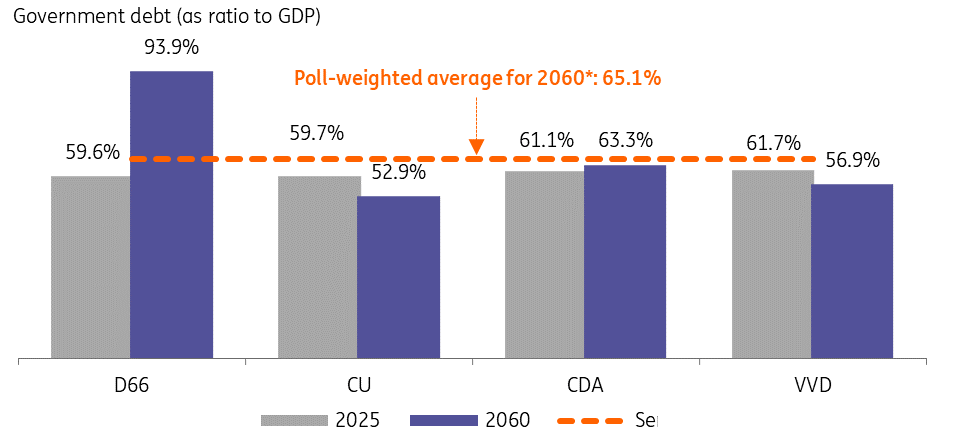

CPB also estimated the long run impact, projecting 2060 debt ratios. Such long-term projections are surrounded by uncertainties; one obvious risk would be a changing interest rate. That said, the long run debt ratio projections vary more widely among parties than the 2025 projections, between 52.9% GDP (CU) and 93.9% GDP (D66). D66 is really the exception here, as VVD, CDA and CU all stay below 64% GDP and the weighted average is only 65.1% GDP. This is not to say that D66 is against fiscal prudence: its manifesto makes clear that it wants a “mid-term review”, in which financial priorities will be rearranged once the effects of the Covid-19 crisis are clearer. All in all, one can expect that if the current coalition were to continue to govern, government debt would stay quite low in international comparison, probably also in the long run.

Public debt ratio projected to remain low on average

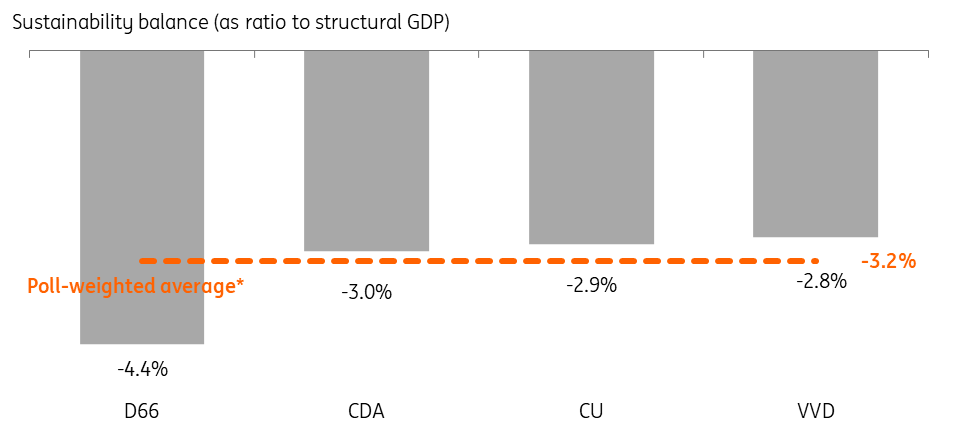

Fiscal sustainability balance implies the shift of a fiscal burden to future generations

We would not be surprised when halfway through its term fiscal policy for the long run will be revisited, once the consequences of the Covid crisis are more apparent. Indeed, one can argue that there is the option value of waiting for new information. As such, long-term plans and projections may be of less importance now than they generally are, as long as the parties involved have a credible reputation for long-term fiscal prudence. If the structural deficit – as signalled by the sustainability gap that remains in the plans of all parties – was addressed later, some of the fiscal burden that is now put on future generations will be shifted back again onto current generations. For the current policy proposals, the projected sustainability balance – the net present value of future revenues and future expenditures – on average stands at -3.2% of GDP.

Technical note: While both are informative, the results for the sustainability balance and long run debt are not fully consistent because of methodological differences. In contrast to the calculations of debt ratios in 2060, these “sustainability calculations” implicitly take into risks to government revenues and spending and therefore use a risk-weighted discount rate rather than a yield curve with ultimate forward rates.

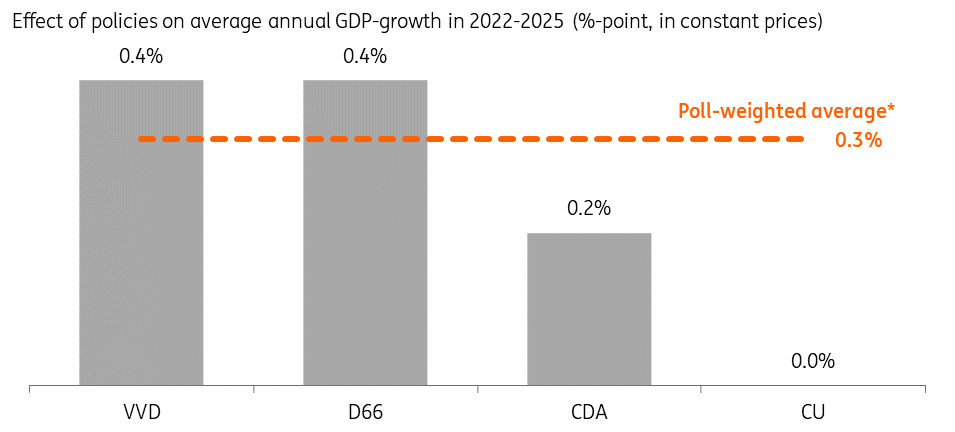

Effects on economic development: temporary GDP boost

Former austerity lovers, many Dutch politicians have drastically changed their stance on crisis management. No party intends to cut back in a way like the past. Current support schemes however will end, and no political party seems to plan a boost like the Biden proposal in the United States right after the corona crisis. However, somewhat looser fiscal policies that current coalition members want, mean temporarily higher expenditures overall on a macro-economic level. In the medium term, these intended policies (in particular higher consumptive public spending) have a temporary net effect of between zero (CU) to a substantial 0.4%-point (VVD and D66) on the average annual GDP-growth in 2022-2025. On average this could add up to a 1.3% boost to the level of GDP and would potentially raise employment and lower unemployment temporarily. This will likely increase wages and inflation a little.

Substantial boost to economic growth in the medium term

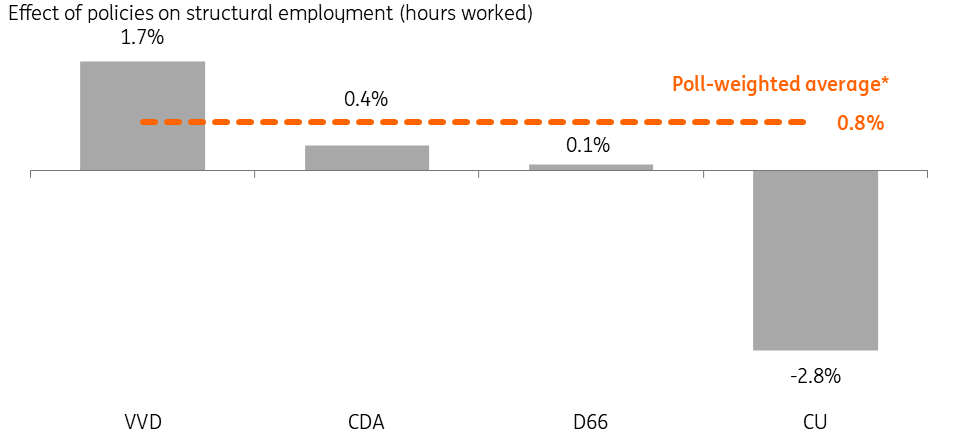

Policies may boost structural employment in the long run

In the long run, higher public expenditures will generally cause a change in composition of output (towards more public and less private via crowding out) rather than expand it. But structural policies that constitute a reform, such as tax cuts that may increase the incentive to work, can boost potential growth structurally. This effect is apparent in estimates for effects on structural unemployment. Where policies of CU have a large negative effect on structural employment (-2.8%), policies of CDA, D66 and especially VVD (1.7%) boost employment. On average, the plans of the coalition partners may structurally increase employment by a significant 0.8%, but only if many of the policy proposals (such as the increase in income-related combination tax credit and general labour tax credit and a reduction in the rent allowance) of VVD would be implemented.

Structural employment boosted substantially only if many of VVD policies are adopted

Often there is a trade-off: some policies that increase employment will increase inequality. VVD policies increase inequality (based on Gini-coefficient estimates), while those of CDA, D66 and CU cause a decrease. In this light, it is also interesting to mention that all parties would like to increase the minimum wage.

Public investment further on the rise despite no new additions to National Growth Fund

Public investment is the type of expenditure that may boost potential growth structurally rather than cause crowding out of private expenditures. The current government already announced a temporary National Growth Fund for a cumulative €20 billion (about 0.5% GDP per year) of investment in knowledge development (including education), scientific research and R&D and infrastructure for the period of five years. The first proposals worth €25.5 billion are currently being judged by an independent committee.

VVD and CDA intend to keep the National Growth Fund as it is. D66 maintains the fund, but transfers some of the funds to the existing Mobility Fund, with no net effect. CU abolishes the National Growth Fund, but also still uses the full amount of €20 billion for alternative investment, in public transport and education.

So, overall there seems to be an increase in public investment that was already envisioned in the base scenario and coalition parties don’t add additional funds to the National Growth Fund. From the spending figures above, however, it seems that the net change in public investment intended by coalition parties is still positive, given that spending on for example education will increase. Note that national accounts consider spending on education as consumption rather than investment; we as economists consider this an investment in human capital since it may raise productivity growth. This is positive for the medium- to long-term economic outlook.

Conclusion: more spending, no matter what

All in all, current coalition parties opt for more spending and lower taxation in the next government term, boosting the economy both in the next years and somewhat in the longer term as well. Even if the current coalition would not continue to govern, the direction of fiscal policy however would generally be the same: almost all traditional Dutch political parties want to increase spending. This goes at the expense of the fiscal position of the government. For the medium term, Dutch public debt levels would ex ante nevertheless remain well within margins that many economists consider as safe. Yet, a fiscal burden is shifted towards future generations. Such a political choice could be reasonable from a well-being perspective, for example when investments translate into non-financial benefits such as a cleaner and safer environment for future generations, but it could also prompt parties to reconsider structural expenditures and taxation at some point in time. Even if priorities and preferences don’t change one could revisit policies given the large uncertainty about the effects of the Covid-19 crisis and the development of the interest rate. And that is exactly what most coalition parties seem to intend: make sure that the economy is well supported in the short run – a real change in comparison to the Global Financial Crisis – but consider going back to previous fiscal norms or improve fiscal sustainability at a much later point in time.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more