Fed set to hold, but signal the potential for a final hike

- 15 September 2023

- FX Rates United States

Mixed US data and Federal Reserve comments solidly back the market pricing of another pause at the 20 September FOMC policy meeting. However, inflation concerns linger and economic resilience suggest the Fed will continue to signal the potential for a final hike even if we don’t think it carry through with it

Fed set to pause again on 20 September

At the last Federal Reserve monetary policy meeting in July, the Federal Open Market Committee raised the Fed funds policy rate range 25bp to 5.25-5.5%. The minutes to the decision also showed officials continue to have a bias to hike further since “most participants continued to see significant upside risks to inflation, which could require further tightening of monetary policy". At the Fed’s Jackson Hole Conference in late August Chair Powell said that policymakers “are attentive to signs that the economy may not be cooling as expected”, indicating a sense that it may indeed need to do more to ensure inflation sustainably returns to target.

Nonetheless, the FOMC minutes also suggested differences of opinion are forming. While all voting FOMC members backed the hike, there were two non-voting members who “indicated that they favoured leaving the target range for the federal funds rate unchanged”. Moreover, “a number of participants judged that… it was important that the Committee's decisions balance the risk of an inadvertent overtightening of policy against the cost of an insufficient tightening”.

In recent months we have had some encouraging news on core inflation with two consecutive 0.2% month-on-month prints with a third coming in at 0.278%, much better than the 0.4-0.5% MoM consecutive prints we got over the prior six months. There has also been evidence of moderating labour costs (the Employment Cost index and cooling average hourly earning growth) together with more modest job creation. Yet we have to acknowledge that the activity data has remained strong with the US economy on track to grow at an annualised 3% rate in the current quarter.

The commentary from officials, including the hawks, such as Neel Kashkari, suggest a willingness to pause again in September (just as it did in June), but to leave the door ajar for a further hike at either the November or December FOMC meetings.

Given this situation economists are universally expecting the Fed funds target rate range to be left at 5.25-5.5% with markets not pricing even 1bp of potential tightening. While the European Central Bank hiked rates but indicated it may be done, the Fed is set to pause, but keep its options open.

The potential for further hikes remains

As with the June hold decision, the Fed is set to suggest that the decision should be interpreted as part of its process of a slowing in the pace of rate hikes rather than an actual pause. While inflation is moderating, it is still too high and with the jobs market remaining very tight and activity holding firm, the Fed can’t take any chances.

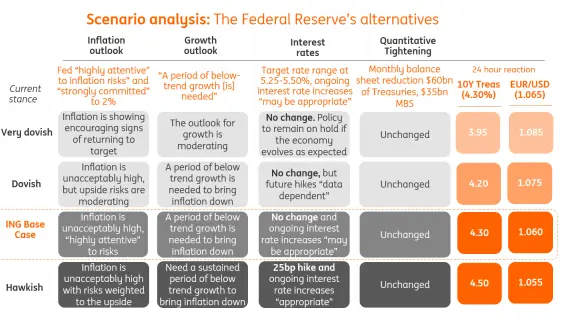

The scenario graphic above outlines the range of possibilities outside of our core view of no change, but the door left open for future hikes. However, the other options have very low probabilities attached to them. We simply cannot see the point of the Fed softening its stance on the outlook for policy and give the markets the green light to sell the dollar and drive Treasury yields lower given this will undermine their fight against inflation. At the same time, a 25bp hike would be such a shock it could be seen as inconsistent with the Fed’s attempt to engineer a soft landing and would hurt risk appetite.

Dot plot to retain a final hike – but we don’t see it being implemented

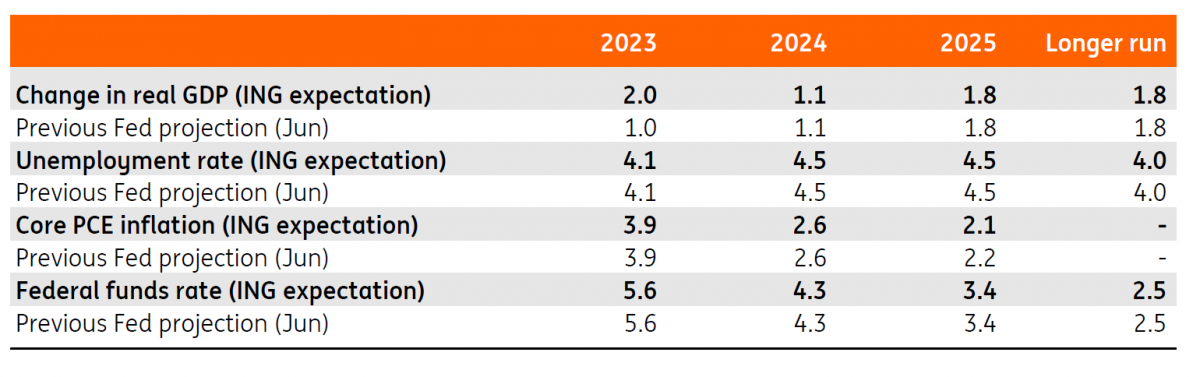

This brings us onto the updated Fed’s forecasts. The key change in June was the inclusion of an extra rate hike in their forecast for this year, which would leave the Fed funds range at 5.5-5.75% by year-end. It seems highly doubtful this will be changed given the data flow, while the unemployment and inflation numbers seem broadly on track. GDP for 2023 is likely to be revised up substantially though given the remarkable resilience of activity and the consumer spending splurge over the summer, much of which appears to have gone on leisure activities.

ING expectations for the Federal Reserve's new forecasts

We don't think the Fed will carry through with that final forecast hike. The combination of higher borrowing costs and less credit availability plus pandemic-era savings being exhausted and student loan repayments restarting should mean that households feel more of a financial squeeze in the fourth quarter and beyond. Rising credit card and auto loan delinquencies also hint at more pain with the Federal Reserve’s Beige Book warning that we may be in "the last stage of pent-up demand for leisure travel from the pandemic era".

The concern is that economic softness could go too far (as highlighted by some officials in the July FOMC minutes) and heighten the chances of recession. Given this risk and the positive developments on inflation and labour costs, we think the Fed will be on hold for a number of months with the data flow gradually weakening the case for a November or December rate hike – which the market itself only gives around a 50:50 chance. Our base case continues to be more aggressive interest rate cuts through 2024 than suggested by the Fed and priced by financial markets.

A word on r*

There has been some chatter about the Fed adjusting its expectation for the long run forecast for what the Fed funds target rate should be, which would be a big story given the anchor this provides for longer dated Treasury yields. This has been put at 2.5% for quite some time, but as the graphic below shows we have started to see individuals nudge their own assessments higher. The momentum suggests it is only a matter of time before it does indeed change.

FOMC individual member expectations for longer run Fed funds rate

Our own assessment is that it is likely to be closer to 3%. Fiscal policy has been loosened significantly under the Trump and Biden administrations and we don’t see that changing anytime soon – the Bloomberg consensus is for the US to run a fiscal deficit of 6% out to 2025. This will mean that monetary policy will need to be more restrictive in order to keep inflation under control. On top of this we have the so called “Triple D” of demographics, decarbonisation and deglobalisation, which will all keep upward pressure on inflation and interest rates.

Regarding demographics, Baby boomers have been saving for retirement which has contributed to a glut of savings, driving down real interest rates. This process is ending as they liquidate the accumulated savings while shrinking birth rates means more competition for workers that could put upward pressure on wages.

As for decarbonisation, switching from cheap and abundant fossil fuels to renewables is expensive and then there is the issue of storage and expanding the electrical grid. Energy bills are likely to be higher, which will increase costs throughout the economy. Then on deglobalisation – Covid, Russia-Ukraine, China-Taiwan have highlighted concerns about stability of global supply chains. Re-shoring and “friend-shoring” is now in vogue, but this will be disruptive and expensive, putting up costs.

As such, we believe it is only a matter of time before the Fed formally declares that interest rates, over the longer term, will need to be higher than we experienced over the past 20 years.

Market rates more focused on where the Fed funds rate is in 2025. And liquidity excesses to tighten more in 2024

The journey for market rates in recent weeks has been impacted by the reduction in the size of the rate cut discount as priced by the markets out to 2025. In that sense there has been some separation between delivery of Fed policy up front and direction for market rates, with market rates rising while the immediate Fed policy rate call has been broadly non-committal (the market discount). That said, the probability for a future rate hike has been on the rise of late, relative to a clearer discount for no change only a couple of week ago. Still, the bigger impact for longer tenor rates is dominated by how low the funds rate can get to when the Fed turns to cutting. Currently that is not much below 4%. We think that will be forced lower as the economy weakens. But it is where it is for now, and that’s helping to keep the 10yr Treasury yield well above 4%, with a tendency to test towards 4.5% (Fed funds low plus a 30-50bp term premium).

In terms of liquidity circumstances, the Fed will acknowledge that the volume of cash going back to the Fed on the reverse repo facility has fallen to US$1.5tr; that’s down some US$1tr from its peak. It’s an important milestone, one that is an echo of the ongoing balance sheet roll-off of Treasuries and MBS from the Fed’s balance sheet (US$95bn per month). Interestingly bank (excess) reserves have not fallen, and in fact if anything they have risen some, now in the US$3.3tr area. This is comfortable, and indicative of ongoing ample liquidity conditions despite the ongoing (soft) quantitative tightening. The Fed might like to comment on this too, largely asserting that this is a good thing, where the falls in balances going into the Fed’s reverse repo facility is the more natural means to excesses exiting the system. The reverse facility has been doing its job, and as balances ease it implies less need for a job to be done. It will feel tighter when bank reserves fall, likely through 2024 and into 2025.

Few reasons for dollar to hand back gains, yet

The dollar is going into the September Fed meeting at the strongest levels since March. The concept of US ‘exceptionalism’ (both in growth and interest rates) looms large over the market and as yet there have been few reasons to bet against the dollar.

The event risk of the September FOMC meeting does not seem a particularly bearish one for the dollar. As above, we are not expecting the Fed to call time on its tightening cycle. And by leaving one more hike in the dot plot, the Fed can avoid yields at the long end of the bond market slipping too far and providing premature stimulus. Indeed, the greater risk might be the Fed scaling down its dot plot median forecast of a 100bp easing cycle in 2024.

A hawkish September FOMC does not mean the dollar has to rally a lot. But assuming there are no surprises, it probably means ideas of a prolonged pause in the policy cycle will see interest rate volatility fall even further and demand for the carry trade stay strong. In practice, this could see USD/JPY work its way much closer to 150 and provoke Japanese authorities into intervention – as they did this time last year.

Expect EUR/USD to trade on the soft side now that the ECB has told us that rates have peaked. However, we suspect good demand will emerge near the 1.05 level. Our house call is that US ‘exceptionalism’ does not last and that US growth converges on the weak eurozone story into 2024.

Typically, November and December are seasonally weak months for the dollar. Our call is that weaker US activity data will become evident over time and that the current period will come to be viewed as ‘as good as it gets’ both for US growth and the dollar. We are sticking with our call that EUR/USD will be trading above 1.10 by year-end.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more