Fed raises rates 25bp, retains a bias to do more

The Fed unanimously hiked its policy interest rate range 25bp as widely expected with the statement retaining the phrasing that further policy firming “may be appropriate”. With two months’ worth of data to come before the next FOMC meeting we suspect evidence of slowing inflation and softer activity won’t make that necessary

25bp hike, further action "may be appropriate"

After categorizing the June pause as a slowing in the pace of rate hikes the Federal Reserve has unanimously voted to raise the Fed funds target range 25bp to 5.25-5.5%, the highest level for 22 years. Markets and economists saw little chance of any other outcome with the main debate being whether the Fed might soften its language and move to a more neutral data dependent stance. We felt that was a long shot and the Fed has indeed kept its tightening bias, indicating further policy firming “may be appropriate”. Chair Powell again referred to the June forecast update signaling the likelihood of one further rate rise later in the year. Meanwhile, the statement described activity as expanding at "moderate pace", job gains being "robust", inflation remaining "elevated".

No room for relaxation when inflation is so high

With two months until the next meeting there was no need for the Fed to change its position. A dovish tilt would have led the market to latch onto the possibility of the Fed not hiking further. Treasury yields and the dollar would have fallen significantly, which would loosen financial conditions in the economy. Given low unemployment, robust wage growth and the fact that core inflation is still running at more than double the 2% target, such a market reaction would run counter to the Fed’s aims.

Instead the Fed stuck with its hawkish bias with the press conference suggesting that the Fed’s mindset remains focused on ensuring that inflation returns to target sustainability even if that runs the risk of a recession. Chair Powell again referred to the extra rate they included in their June forecast update, which would take the policy rate range to 5.5-5.75% and stated that intermeeting data was broadly consistent with their expectations. Markets though have their doubts with just five basis points of tightening priced for that September FOMC meeting with it being a 50-50 call whether there will be a 25bp hike by the November FOMC meeting.

Data flow likely to mean September FOMC meeting is another "pause"

By the time of the 20 September FOMC meeting we will have had two further job and inflation reports, a detailed update on the state of bank lending plus more time for the lagged effects of the already enacted Fed tightening to be felt. Headline inflation may be a little higher then than it is today, reflecting energy cost changes, but there is little Fed policy can do about that. However, core inflation looks set to slow further and could be down at around 4% versus the current 4.8% rate given decelerating housing rent inflation, falling used car prices and weakening corporate price intention survey evidence.

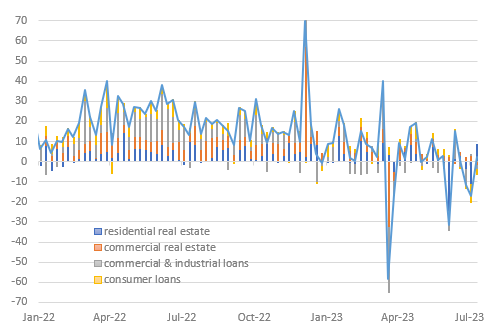

As for activity, manufacturing is clearly struggling, but the jobs market remains tight and the service sector continues to expand. Over the next two months, we think the headwinds for activity will intensify though with outstanding stock of commercial bank lending set to fall further thanks to the combination of higher borrowing costs, which Powell described as "restrictive" and tightening lending standards. Student loan repayments will not have restarted by that point but the potential consumer spending implications are likely to become more apparent.

Week on week change in outstanding bank lending ($bn)

Another pause could mean the peak

So, by the time of the 20 September FOMC meeting, we think the Fed will have evidence suggesting inflation remains on the path to 2% and that activity is slowing to below trend rates and the jobs market is cooling as desired. If correct we suspect this will mean another pause, like at the June FOMC meeting, but with the Fed tentatively keeping one additional rate hike in its forecast profile before year-end. However, our base case is that disinflationary and decelerating activity trends will continue and the Fed will not carry through with it. We think that 5.25-5.5% marks the peak for the Fed funds target range.

The Fed cements a mild rate cutting discount ahead, keep upward pressure on Treasury yields

From a market rates perspective one of the key things to watch today was how the Fed decision and subsequent commentary might affect the Fed funds strip. In particular, beyond the hiking and into the discounting completion of the rate cutting phase. This is important, as where the fed funds strip sits in 2025 has a material effect on longer dated Treasury yields, as, say the 10yr yield, really should not trade much through the longer dates on the strip. In fact they should trade at a 30bp premium to it (above it).

We went into the FOMC with the Jan 2025 implied rate at just under 4%. It’s still there post the meeting, in the 3.9% to 4.0% range (as it jumps around, typically on low volumes). Remember this was down in the 3% area when Silicon Valley Bank went down. The fact that its 100bp higher now limits the extent to which the 10yr Treasury yield can fall. In fact it should rise, and we continue to target it to get to the 4% area in the coming weeks, versus a current level of between 3.9%. That broadly flat to the implied funds rate in Jan 2025. That’s too low for the 10yr yield, as it implies no curve just as the Fed has completed it rate cutting cycle.

We are not agreeing with the market discount per se, but where it sits is important in terms of framing the here and now for the 10yr Treasury yield, and in that way helps to add context to the immediate few weeks ahead. Meanwhile the Fed continues to gradually tighten through its bond roll-off programme. Most of the impact of this has been in lower volumes going back to the Fed on the reverse repo facility. Bank reserves have in fact held steady. This allows the Fed to keep the tightening pressure on. It also keeps bills rates under elevation pressure, and prevent the bills curve from moving to a state of material inversion. At least not just yet. And, all other key rates are up by 25bp too, including the reverse repo rate now at 5.3%.

No surprises from the Fed leaves FX cross currents in play

A widely expected 25bp hike from the Fed and no substantive changes in the FOMC statement initially caused barely a ripple for the dollar. However, the dollar did soften marginally through Chair Powell’s press conference – and it was not clear why. In fact, Chair Powell left the door open to a September rate hike should data determine the Fed had more work to do.

As elsewhere in the world it looks increasingly like the dollar trend will be driven more by the data than central bank communication. Indeed, we may not hear much from the Fed before the Jackson Hole Fed symposium on 24-26 August.

In terms of the data, our house call for further signs of US disinflation and slowing activity may deliver a gentle dollar bear trend into the next FOMC meeting in late September. The problem for dollar bears like ourselves is that growth prospects overseas do not look particularly compelling – especially in the eurozone where stagnation is at risk of turning into a contraction. On balance we think the US disinflation story will dominate, however, and that EUR/USD should drift up to 1.12 and 1.15 by the end of September and December respectively.

In terms of those cross currents, European Central Bank policy is certainly one of them. Does ECB hawkishness fall away too quickly and undermine the EUR/USD rally? And has anything really changed in China despite high level indications of more stimulus?

Given quite a few unanswered questions it is no surprise that cross market volatility remains quite low and that investors remain enamored with the carry trade. This will keep the Japanese yen on the back foot – unless the Bank of Japan surprises on Friday – and maintain the demand for the market’s favourite EM high yielders such as the Mexican peso and the Hungarian forint.

Download

Download article

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more