Fed prefers to pause, but we doubt they will

- 30 October 2019

- United States

The Federal Reserve has cut interest rates by 25bp at the third consecutive FOMC meeting. The market anticipates a pause in December, but a slowing economy means we think there are more rate cuts are to come

Fed delivers another 25bp

As widely expected the Federal Reserve has cut the target rate 25bp to 1.5-1.75% and once again the decision was not unanimous. Esther George and Eric Rosengren, who believe the economy is performing well and are worried about “overheating” in some sectors, opposed today’s move. In September James Bullard had voted for a 50bp move, but this time he went with the consensus.

The key change in the accompanying statement is that the Fed has dropped the sentence saying that the FOMC “will continue to monitor the implications of incoming information for the economic outlook and will act as appropriate to sustain the expansion” (our emphasis). Instead we have a sentence saying the FOMC “will continue to monitor the implications of incoming information for the economic outlook as it assesses the appropriate path of the target range for the federal funds rate” (our emphasis). This suggests that the Fed wants to take stock after three consecutive rate cuts in July, September and October. The key question is will the data allow them to? We have strong doubts.

Markets expecting a December pause

In terms of where we go from here, financial markets are anticipating a pause from the Federal Reserve. The fact that equities are at all-time highs and there have been positive trade discussions between the US and China seem to have allayed recession fears. Implied probabilities based on futures contracts are only fully pricing one further rate cut in total with roughly a one in four chance that it comes at the December FOMC meeting.

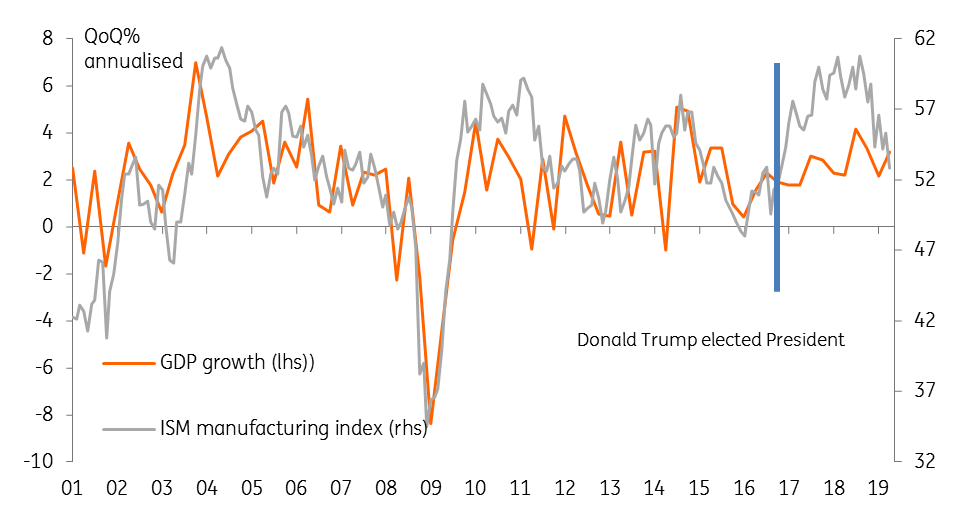

ISM surveys point to a more rapid deceleration

But we think the Fed has more work to do

However, the economic data is not as positive with business surveys, such as the ISM series in the chart above, suggesting the US economic slowdown is intensifying. Friday’s jobs report is also likely to underline the deceleration story even with the acknowledgment of a temporary distortion due to the GM-related strike. Inflation expectations are also very low and wage growth has moderated recently. With the European and Asia story showing little sign of a rebound and the dollar remaining firm we are, for now, sticking with our view that the Fed will take out additional “insurance” against recession at the December meeting with a further rate cut possible in 1Q20.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more