Fed policy pivot helps boost gold prices

- 25 January 2023

- Commodities, Food & Agri

Gold prices have surged over the past two months with expectations that the US Federal Reserve will slow its interest rate rises. We have increased our 2023 price outlook slightly based on the faster-than-expected pivot in US interest rate policy and the return of Chinese demand after Beijing’s U-turn on its zero-Covid strategy

Gold gains on softer dollar

Gold prices fell sharply last year after hitting a record high of above $2,000/oz in March as US dollar strength and central bank tightening weighed heavily on the precious metal. Higher interest rates make gold, which provides no returns, less attractive.

Investor appetite for gold also decreased in 2022. Last year was the second consecutive year of decreasing demand for gold exchange-traded funds (ETFs). Investors sold $3bn worth of physically-backed gold ETFs in 2022, a 3.4% decrease to $202.7bn of global holdings at the end of December, according to data from the World Gold Council.

But the precious metal has risen almost 20% since early November to above $1,900/oz at the beginning of 2023, helped by a weaker dollar and bets on smaller rate hikes by the Fed amid signs of cooling US inflation.

US business conditions contracted again in January as demand for goods and services fell for the fourth month in a row, the latest S&P survey showed.

The annual rate of US inflation fell for the sixth consecutive month in December to 6.5% from 7.1%, according to the latest consumer price index released earlier this month, increasing bets that the Fed may slow down the pace of its monetary tightening.

Our US economist now sees growing risks that the Fed may stop hiking after a 25bp move in February. With recessionary forces intensifying and inflation looking less threatening, the prospects of Fed rate cuts later in the year are growing. Currently, my colleague in the US expects a final 25bp rate hike in March.

Real yields have also been weakening, giving support to non-interest-bearing gold. Ten-year real US yields reached their highest levels in more than a decade last year, pushing gold from a peak of above $2,000/oz in March 2022 to a low of just above $1,600/oz in November. Given the strong negative correlation between gold prices and real yields, gold struggled in the rising yield environment. Higher yields increase the opportunity cost of holding gold, which turned investors off the precious metal. The fall in real yields since November has encouraged a more bullish view on gold and has seen the price rally above $1,900/oz.

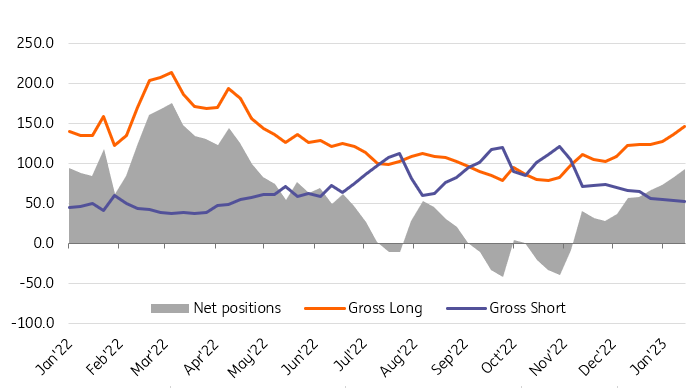

Meanwhile, the latest CFTC data show that speculators increased their bullish bets in COMEX gold by 10,783 for a seventh consecutive week, to leave them with a net long of 93,357 lots as of the last reporting week. The net-long position was the most bullish in almost nine months.

However, ETF holders haven’t shown a shift in sentiment just yet. The gold rally still lacks support with total gold held by ETFs falling 0.2% so far this year despite rising prices.

Speculative positioning in COMEX gold

Central banks' gold buying hits record highs

Central bank buying in the first nine months of 2022 was the highest since 1967, according to the World Gold Council. During times of economic and geopolitical uncertainty and high inflation, banks appear to be turning to gold as a store of value.

Last month, the world’s official financial institutions bought 673 tonnes. In the third quarter alone, central banks bought almost 400 tonnes of gold – the largest quarterly purchase since records began in 2000.

The buying in the third quarter was led by Turkey with 31 tonnes, taking gold to about 29% of its total reserves. Uzbekistan followed with 26 tonnes, while in July Qatar made its largest monthly acquisition on record since 1967.

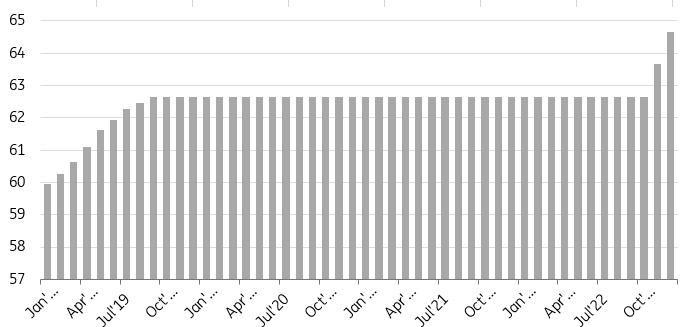

Meanwhile, earlier this month the People’s Bank of China revealed a further 30-tonne purchase of gold in December, following on from its first reported monthly purchase of 32 tonnes in more than three years in November. By the end of 2022, China’s gold reserves reached 2,011 tonnes.

Given the current geopolitical environment is likely to persist, we believe central banks will continue to add to their gold holdings in the coming months.

The gold purchases made by central banks around the world constitute only a portion of the total demand for bullion, which also includes the consumption of jewellery, investments in gold bars, coins, ETFs, and technology.

China gold reserves

Chinese gold demand disappoints in 2022

China’s 2022 gold consumption fell 10.6% from 2021 to 1,001.7 tonnes, according to the China Gold Association (CGA). The decline in bullion demand was led by weak bar and coin demand, which fell 17.23% last year. Jewellery demand fell 8% to 654.32 tonnes, the CGA said.

Gold jewellery consumption saw a strong recovery at the beginning of last year but fell again after subsequent Covid outbreaks, while high gold prices slowed down investment and industrial demand.

We believe China’s reopening and the end of its strict zero-Covid policy should support Chinese gold demand’s rebound in 2023. China’s gold demand may also benefit from the government’s efforts to stimulate consumption, as was stipulated at the Central Economic Work Conference at the end of last year.

Near-term demand may also receive a seasonal festive boost from the Lunar New Year holiday at the end of January. The Chinese holiday is observed from 21 January to 27 January.

Fed’s rate path crucial to gold in 2023

Looking ahead, we believe gold will remain sensitive to the Fed’s monetary policy. A less hawkish Fed is likely to lead to a weaker US dollar, which would support higher gold prices. Any hint of rising hawkishness from the US central bank would likely push gold lower.

Meanwhile, fears of recession should provide support for gold, while continued weakening in the US dollar should further boost gold prices.

We expect gold prices to move higher over the course of 2023 with prices averaging $1,900/oz in the fourth quarter of 2023.

ING forecasts

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more