Fed meeting: Three things to watch this week

- 12 June 2017

- FX United States

Expect a rate hike, but what the Fed says on growth, inflation and its balance sheet plans are just as important for markets

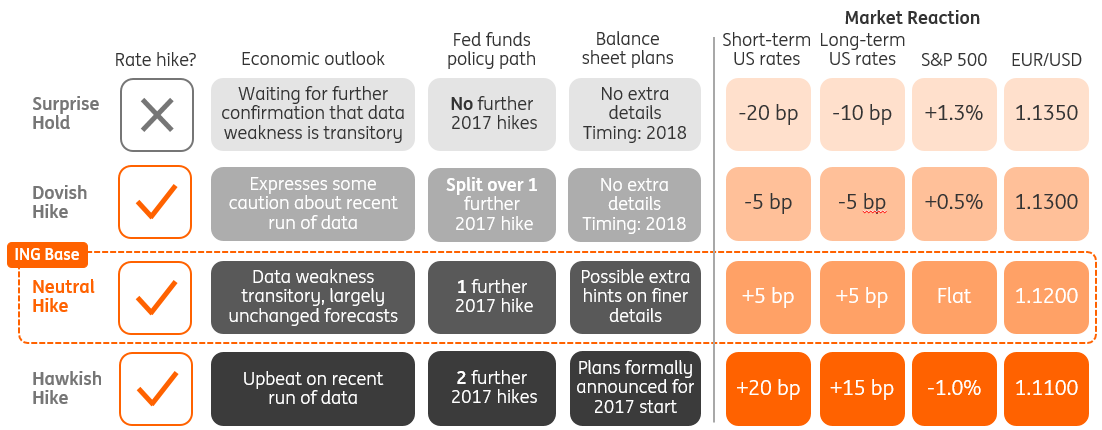

How markets could react to the Fed this week

Economic outlook: It's all 'transitory'!

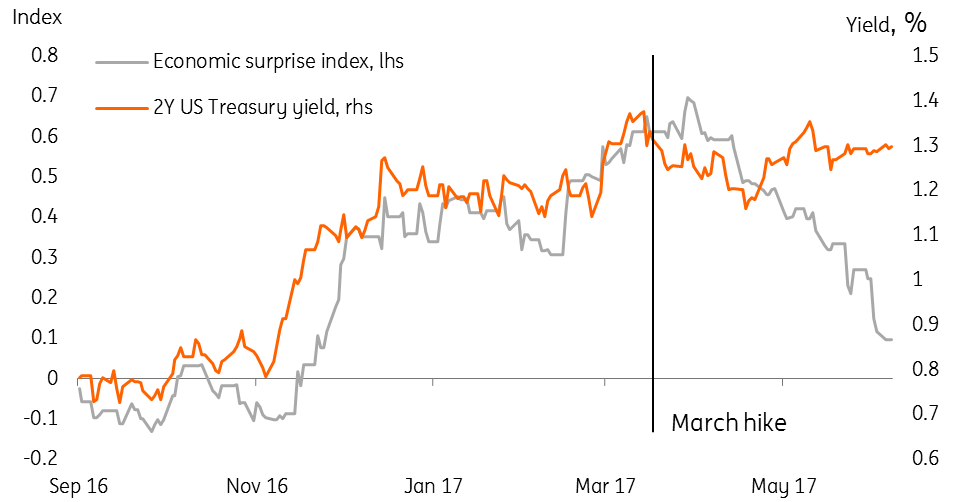

There’s little doubt that much of the data since the March Fed meeting has been disappointing. No doubt this is partly attributable to poor seasonal adjustment, but this has left markets sceptical about the rates outlook for the rest of the year.

The Fed is at pains to point out that it is all ‘transitory’ – a buzz word that was used nine times in the latest minutes.

Expect see the ‘T’ word get plenty of airtime this week, and the Fed will point to some recent better news – most notably the dramatic fall in the unemployment rate since January.

We also anticipate a modest recovery in growth over the rest of the year, with or without Trump’s stimulus package. That should be enough to see the Fed hike again in September.

Economic data has disappointed since March

Core inflation - where is it?

Where the Fed’s ‘transitory’ argument breaks down, at least at face value, is on inflation. Specifically, the Fed’s favoured core PCE measure has failed to break out of the 1.5-1.8% range for some time. Wage growth has also been less aggressive in recent months.

This could easily change as the economy picks up speed again in the second quarter but, in the short term, this could be a communication headache for the Fed as their hiking ambitions diverge from their data-dependency guidance.

The Fed’s balance sheet plans

The Fed, keen to avoid taper tantrum 2.0, appears to be drip-feeding markets with its balance sheet plans to test the reaction.

There’s potential for further balance sheet clarity at this week’s meeting

We now know that the Fed will unwind it’s balance sheet using a cap on the value of bonds that would be allowed to run-off each month. This cap will gradually increase every three months. But we are still awaiting details on the initial size of the cap, the likely size of cap adjustments and, crucially, the target equilibrium size of the balance sheet.

The other key element is timing. We are expecting the Fed formally to announce the start of this process at its December meeting, with reduction beginning in early 2018. The meeting minutes seem to be the favoured way of communicating these details, but there’s potential for further clarity at this week’s meeting.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more