Expect robust semiconductor demand in 2025, but not in all segments

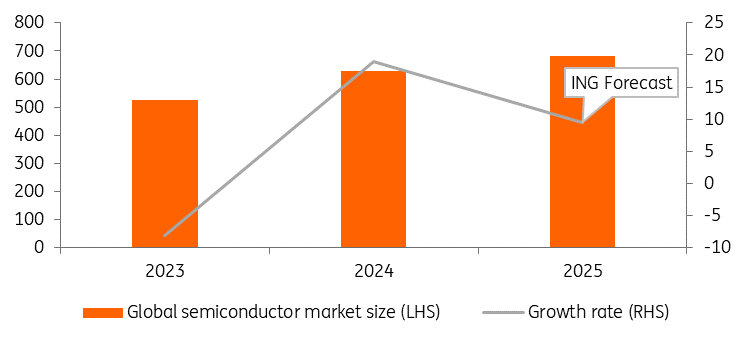

In 2025, we expect 9.5% growth in the global semiconductor market, driven by robust demand for data centre services, including AI. However, growth in other, more mature segments is expected to be stagnant. Our forecast is lower than the projections of WSTS and others, but slightly exceeds ASML's long-term growth expectations for the sector

We expect 9.5% growth for the global semiconductor market

The Covid-19 crisis marked an interesting period in the recent history of the semiconductor industry. There was a high demand for electronics products and therefore semiconductors. This demand was initially difficult to meet, leading to a build-up in semiconductor inventory. These challenges were especially prevalent in the automotive sector, where a shortage of semiconductors led to production delays. What followed was a ramp-up in inventory and a subsequent run-off. Indicators, such as the South Korean semiconductor and parts inventory, suggest that inventory levels have normalised. However, leading industry executives have expressed early concerns about a potential slowdown in the mature market semiconductor segment.

The market is becoming increasingly bifurcated, with strong growth in AI and data centre-related segments and stalling growth in more traditional segments, like PCs, smartphones and the automotive sector, driven by semiconductor price pressures. Recent Nvidia results were poorly received, and Samsung has also lowered its outlook for AI-driven demand for its products. Despite this, advancements in AI are progressing rapidly, and growth appears strong.

The WSTS (World Semiconductor Trade Statistics), a leading institute, expects global semiconductor market growth of 11.2%. This is below previous forecasts of IDC (15%) and Gartner (12.7%). The WSTS forecasts are driven by 16.8% growth in logic microchips, 13.4% growth in memory microchips and low single-digit growth in mature technology semiconductors.

Considering the weaker-than-expected earnings season and disappointing 1Q25 guidance, along with signs of inventory build-up and price pressure from China, we hold a more negative outlook on mature technology compared to the WSTS. Additionally, Deepseek demonstrated that advanced AI models can operate with fewer advanced memory chips. Coupled with capacity expansions in the memory segment, this could result in some price pressure. Therefore, we are slightly less optimistic about the growth of the memory market than the WSTS.

Our overall expectation for FY25 semiconductor market growth is therefore 9.5%. This remains slightly above the 9% longer-term industry trend growth rate assumed by ASML. Despite the observation that the sentiment in the sector is turning somewhat negative at the moment, the outlook is still rather good for the global semiconductor sector. Nevertheless, since European manufacturers do not focus on leading-edge technology, the continent may not benefit from sector growth.

ING expects solid semiconductor market growth (US$bn, %)

Smartphone sales will not drive the semiconductor industry in 2025

Smartphones no longer seem to be the driver of revenue growth in the semiconductor sector. Recent iPhone upgrades were relatively minor compared to previous generations, with the iPhone 16 showing small improvements on the iPhone 15 and disappointing AI capabilities. Also, as global technology market analyst Canalys recently stated, “vendors are facing a tricky 2025 with mounting complexities”. Therefore, the global smartphone market will not be a driver of semiconductor market growth in 2025. Nevertheless, as the market is increasingly driven by high-end products, Samsung and Apple will likely grow their revenues.

Semiconductor sales for the automotive industry will likely disappoint

There is a strong secular trend towards a higher share of semiconductors in cars, which is accelerating with the increasing adoption of electric vehicles (BEV/PHEV). However, the overall global automotive market outlook for 2025 is modest, with our automotive analyst projecting a 1.6% growth.

The share of electric vehicles in Europe and North America is only slowly rising. Nevertheless, in 2025, the share of electric vehicles will likely approach 50% in China. Therefore, we expect 19% sales growth for electric vehicle sales.

Since the second half of 2024, we have observed an inventory correction across automotive supply chains, which typically takes about a year to stabilise. However, the increasing significance of the Chinese market complicates predictions. While Chinese demand exceeded expectations in the latter half of 2024, there are growing indications of oversupply in China, resulting in lower prices.

Given the low growth in the Western world and indications from recent earnings releases, we hope for stable automotive semiconductor markets in 2025. Nevertheless, the automotive semiconductor market is notoriously difficult to predict.

Semiconductor sales for AI and server applications continues to rise

The trend of hyperscale data centres spending more on semiconductors is continuing. According to Gartner, hyperscale data centres spent US$112bn on semiconductors in 2024, almost double the amount the year before. Strong growth is expected to continue.

AMD reported FY24 AI chip revenue of more than US$5.0bn and expects AI-driven sales to be in the “strong double digits” in 2025. AMD expects “tens of billions” of dollars in sales from AI chips in the next couple of years. Nvidia is also confident it can grow sales, especially because of the ramp of its next-generation AI chip (Blackwell).

TSMC expects “the revenue growth from AI accelerators to approach a mid-40% CAGR for the five-year period”. This is above its overall long-term revenue growth expectation which should approach a 20% CAGR in US dollar terms for the five years starting from 2024.

We also expect a drive by data centre operators to develop their own microchips and therefore expect the rise of Application Specific Integrated Circuits (ASICs). Large hyperscale operators look for the most cost-efficient computing power because of the need for cheap AI model inference and some training applications. This can be achieved through tailored ASICs. Companies such as Broadcom and Marvel will help to design the semiconductors, while TSMC will produce them. Over time, these products are expected to take market share from AMD and Intel.

In 2025, we continue to see the technological advancement of leading-edge memory chips and solid demand for high-bandwidth memory. As Deepseek showed, there is some downside risk to this expectation as data centres may invest a bit less in high-bandwidth memory chips and a bit more on advanced compute chips. However, as data centre investments grow, the future demand for advanced node logic semiconductors looks promising.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

SemiconductorsDownload

Download article

12 March 2025

Trends shaping the semiconductor industry in 2025 This bundle contains 3 Articles