Global car market in the slow lane: China soars ahead of the West in electrification

We anticipate another year of sluggish growth for the global car market, marked by some positive factors but also numerous uncertainties. While the regional divergence in electric vehicles (EVs) grows, we expect a resurgence in the European EV market in 2025

The global car market should have expanded in 2024, but at a slow pace

The global car market likely expanded last year, although on a relatively limited scale. We assume the global car market grew by 1-2% last year, with our current estimate of +1.7% being pretty close to the +1.8% we projected for FY24 in August.

We also note that last year’s global car sales volumes remained well below the 2019 mark and several millions short of the 2017-18 levels. In Europe, the lack of a post-Covid market rebound is even more pronounced with car sales still down approximately 18% relative to 2019. This means renewal rates are low amid an ageing fleet. One factor in the persistent weak demand is the reduced replacement of company cars during the pandemic.

Slow growth in car sales in 2025, with the volume still below pre-Covid figures

Europe showed the slowest growth among the top three markets last year

While China and the US experienced low-to-mid single-digit year-on-year growth in FY24, the European auto market, monitored by the European Automobile Manufacturers’ Association and including the European Union, EFTA members, and the UK, lagged with modest growth of 0.9% compared to 2023, with the EU market itself growing by just 0.8%.

Based on data by the China Association of Automobile Manufacturers (CAAM), China produced 31.3m and sold 31.4m light-duty vehicles in 2024, up 3.7% and 4.5% year-on-year, respectively. In the US, light vehicle sales reached approximately 15.9m, up 2.2% year-on-year, according to Wards Intelligence.

Largest European car markets had mixed performance in 2024

In Europe, car sales dynamics varied among the big European markets, partly impacted by the phasing out of the electric vehicle incentive programmes. While France, Germany and Italy recorded declines of 3.2%, 1.0% and 0.5%, respectively, in FY24, Spain – where the incentives for EVs and plug-in vehicles were extended through the first half of 2025 – showed a healthy growth rate of 7.1%. The UK's car market also expanded in 2024, by 2.6% year-on-year, also pushed by the EV mandate.

We expect limited growth for global auto sales in 2025, with many uncertainties

Looking to 2025, we expect Western Europe to deliver another subdued performance, with growth of just 1.0%, in the absence of some additional incentive programmes. We think the European car market will be supported by the continued reduction in policy interest rates and by an anticipated rebound in EV sales, helped by multiple new model launches, among other things. However, policies are under pressure to adopt a flexible approach regarding ambitious CO2 targets.

In China, we expect the market expansion to continue, underpinned by the remaining incentive programmes and helped by more affordable price levels of locally manufactured EVs. We note that our base case growth rate for the Chinese market of 2.0% is lower than the wholesale growth of 4.7% expected by CAAM, including +24.4% for new energy vehicles (battery electric vehicles [BEVs], plug-in hybrid electric vehicles [PHEVs] and fuel-cell vehicles). In the US, the environment is less predictable given the new US administration but we do assume a modest growth of the market of 1.5%.

Overall, we expect the global car market to expand by 1.6% in FY25.

European car manufacturers will remain under pressure

European car manufacturers encountered significant challenges in 2024, especially during the latter half of the year. We anticipate that the situation will remain difficult this year unless there are policy concessions and supportive measures.

In addition to our expected limited growth, European original equipment manufacturers (OEMs) face ongoing headwinds in China due to the elevated competition from quickly developing EV-focused players such as BYD and Xpeng, combined with more restrained purchasing attitudes among the country’s consumers. We expect that the market share of the European and Western brands will continue to decline during 2025. Intensified competition in the changing global marketplace has also encouraged Japanese carmakers Honda, Nissan and Mitsubishi to consider joining forces.

In the United States, major players such as Toyota and Hyundai/Kia as well as European car manufacturers like VW, Mercedes, and BMW are at risk of facing import tariffs and uncertainties regarding their North American production and supply chains, including facilities in Mexico and Canada. This could lead to higher car prices and affects their local competitive position. Meanwhile, in the European Union, stricter emission standards and the gradual removal of EV incentives add to the challenges.

Therefore, we expect European car manufacturers to deal with multiple obstacles this year as they strive to adjust to the evolving market and geopolitical environment and navigate between short and long-term interests.

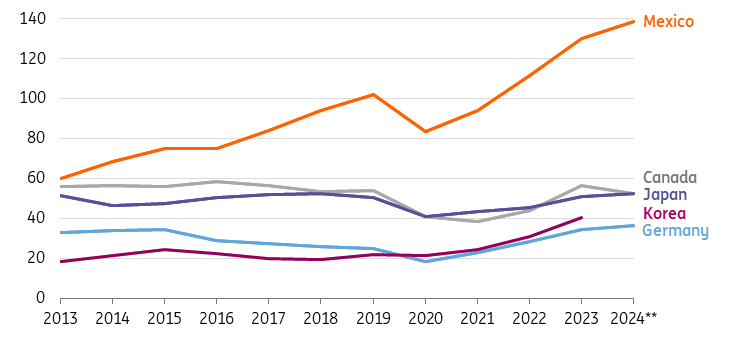

Manufacturing sites in Mexico are most exposed to potential US tariffs on cars and parts

Production volumes to lag sales

Given the modest demand outlook, we anticipate that production will lag behind sales volumes this year. Consequently, we expect the global car manufacturing sector to remain roughly flat year-on-year. This stagnation in production growth is likely to exert additional pressure on auto parts manufacturers, who rely on volume and may face increased cost-cutting and pricing pressures from OEMs.

We find some reassurance in our expectation of relatively stable volumes in 2025, compared to the more significant declines in the latter half of last year. Although our outlook for European car and auto parts manufacturers remains subdued for the current year, we believe the situation may pick up in the second half of this year, given the weaker performance in the second half of 2024.

Growing divergence in electrification of new cars across the world

Diverging picture between East and West

China continues to outpace the rest of the world when it comes to the car market's biggest trend: electrification. China’s share of EVs (BEV and PHEV) in total new car sales exceeded 40% in 2024. China continues to push ahead with EV subsidies to boost consumer demand. Chinese EV supply chains are already well-developed, and its pushing strategy helps industry players to scale and fill up production slots of factories, while the numerous EV-only players also deal with excess capacity.

The world’s largest car market is on track to get close to the 50% line for EV sales in 2025, much earlier than previously anticipated and way ahead of the pack. With a share of more than 60% in global EV sales, this pushes the market EVs to almost 25% in 2025 (with BEVs covering some 17%) despite backtracking in the US.

The diverging picture between East and West is evident in the rapidly growing market share of new Chinese brands. Both BYD and Geely have entered the top 10 car groups, whereas just five years ago, BYD was relatively small. In 2024, BYD delivered nearly as many EVs as Tesla (1.76 million) and could potentially become the largest BEV manufacturer by the end of 2025.

This rapid electrification hurts Western incumbent car makers with significant stakes in China including Mercedes, VW and BMW, as they lose ground to Chinese brands in the transition. This remains a concern for 2025.

China's share in global sales of Western carmakers declined in 2024

European CO2 policy forces step up in EVs

Europe faced stagnation and even a slight setback in electrification in 2024 compared to 2023. Several countries entered the second more difficult phase of electrification and started to scale back fiscal support. The slipped EV share in 2024 was due to Europe’s largest car market, Germany, which has seen a decline in the market share of battery EVs (BEV) of almost 5% points from 18.4% in 2023 to 13.5% in 2024 following the sudden scrappage of purchase subsidies for the general public at the end of 2023.

The policy-driven uptick in the UK wasn’t enough to keep figures up. 2025 is going to look different, at least if ambitious CO2 targets for 2025 aren’t softened following calls to allow flexibility for already tested car makers. The EU figure of 13.6% for BEV should exceed the 20% level to meet an average unit emission of 93.6 gram/km, despite an option for pooling and buying CO2 credits. Provided the current policy remains, we expect the total EV share (PHEV + BEV) to rise to 27%. A strategic dialogue on the future of the car industry in the EU is expected to provide clarity to this key topic at the start of 2025. Part of the solution could also be to support demand by temporarily and conditioned reintroduction of purchase subsidies.

With the slowdown in the EV transition, plug-in hybrids are gaining attention again, and their battery ranges are increasing to 140km or more. However, they are becoming less appealing to manufacturers as the assumed electric utility factor will be reduced in 2025, making them less effective in meeting targets. Overall, we do not anticipate significant growth for PHEVs in Europe in 2025.

Uptake of EVs expected to stall in the US in the short run following exit of subsidies

The federal government in the US is shifting away from supporting electric vehicles under Trump. The target of 50% EV sales by 2030 and the associated tailpipe regulations requiring 20-56% EVs by 2032 has been revoked and purchase subsidies up to $7,500 will likely be halted as well.

The number of EVs eligible for subsidies has already been limited and Chinese EVs have effectively been banned, but further removal of support (also for charging infrastructure) will lead to significantly lower growth expectations for 2025 compared to previous expectations.

However, individual more urbanised states could still encourage more sustainable choices on a regional level, which is already being reflected in excise duties. And in individual cases, with intensive point-to-point use in particular circles, EVs can already be economical. The total EV-share (PHEV + BEV) in total sales of 10% are unlikely to grow much in the short run, but it won’t sink either.

Ford and GM have proactively addressed the market slowdown by reducing their EV production growth plans ahead of the new administration. Meanwhile, market leader Tesla, with its own charging network, benefits from reduced competition in its home market.

Lower battery prices are driving self-sustaining EV sales

Global prices of (lithium-ion) battery packs resumed their downward trend in 2024 and dropped by some 20% to $115 per kWh, according to BNEF. After a phase of higher battery metal prices, this is good news for the uptake of EVs. And prices could slip further in 2025. This is important as the battery usually makes up more than 30% of the total production costs.

A complicating factor though is the rest of the world has turned even more dependent on China for (cheaper) batteries and battery supplies. Large manufacturers including CATL and BYD supplied 85% of the global battery cell production at the end of 2023, and even more than two years earlier (80%).

While the EU imposes higher tariffs on Chinese car imports, it remains heavily dependent on China for essential EV components and has yet to achieve greater self-sufficiency. In the current geopolitical climate, this dependency is a concern until a viable recycling industry emerges.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article