The eurozone’s recovery is hitting a soft patch

- 4 February 2022

The eurozone recovery is hitting a soft patch on the back of Omicron and high energy prices, but it should gain speed again from the second quarter onwards. The more lasting inflation story is pushing the European Central Bank towards a gradual change of tone. Net asset purchases are likely to end in September, leaving the door open for a rate hike by year-end

Another weak quarter likely

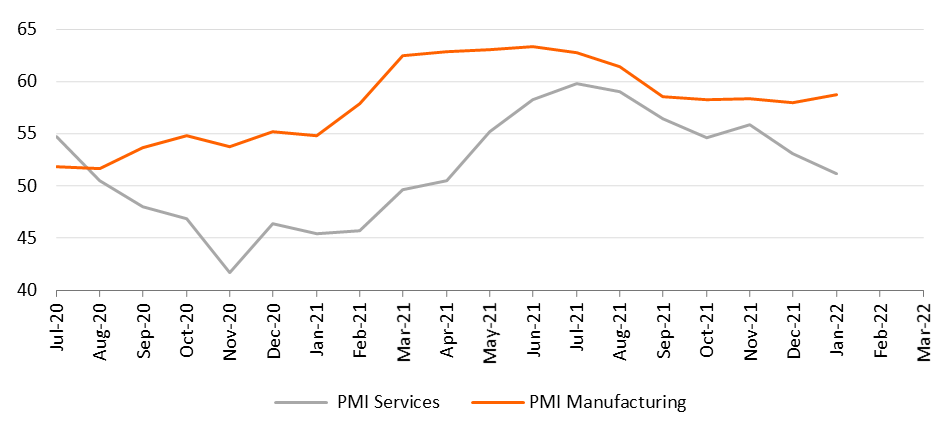

After a weak fourth quarter, with only 0.3% quarter-on-quarter growth, the eurozone is likely to also see subdued growth in the first quarter of 2022. January was hit by a record number of Omicron infections, leading to higher absenteeism due to illness, which in turn hurt production. At the same time, containment restrictions were a brake on consumption, especially in the services sector. The good news is that with the peak in infections probably reached, restrictions in many countries are now being relaxed.

Supply chain problems, which were probably the biggest cause of the gross domestic product (GDP) contraction in Germany in the fourth quarter of last year, have also subsided a little, causing the Ifo-indicator to improve in January. It is probably too early to say that the frictions in the supply chain are completely behind us, as Omicron lockdowns in China might spell trouble again. High energy prices remain another headwind that is likely to weigh for some time on consumption expenditures.

Weakening in services sector on the back of Omicron

Tight labour market

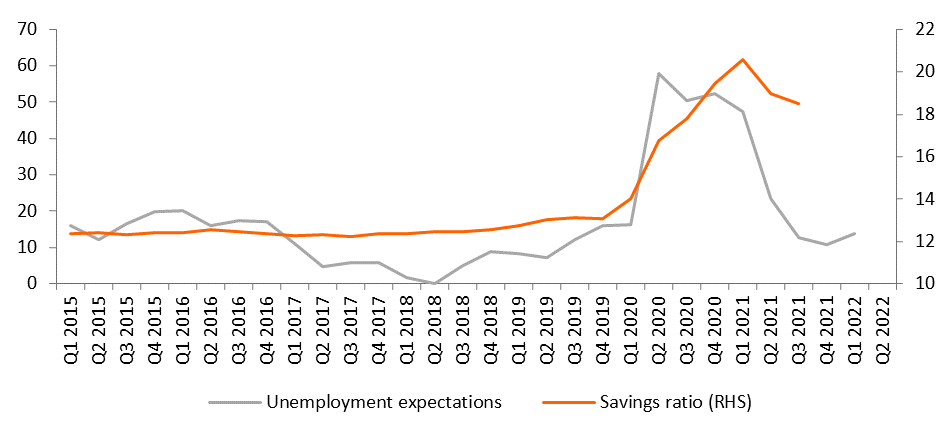

While the current circumstances are mixed, there is still genuine hope that the eurozone economy will put in a more than decent growth performance this year. The consumer has certainly been hurt by high energy prices, but government support is softening the blow in many countries. The savings ratio is still several percentage points above its pre-pandemic average, which could provide some extra spending power, especially since brighter labour market prospects could reduce precautionary saving. The unemployment rate fell to 7.0% in December, vacancies are at a very high level, and a growing number of companies are signalling labour scarcity.

So consumption will probably remain a driving force of the recovery. On top of that, the impact of the European recovery fund will start to kick in this year, adding to growth, especially in the southern member states. Over the coming years fiscal policy is going to become a bit less expansionary as the Stability and Growth Pact is likely to return in some form, perhaps not yet fully in 2023, but certainly in 2024. All in all, we expect 3.7% growth this year and 2023 might still see 2.7% before slowing down to a more long-term potential growth rate of 1.5% in 2024.

Improving labour market perspectives will push down savings ratio

Another inconvenient inflation surprise

Another month, another inflation forecast increase. Indeed, the preliminary estimate showed the harmonised index of consumer prices (HICP) inflation at 5.1% in January, even higher than December’s 5%. However, with the January 2021 German value-added tax (VAT) hike disappearing from the equation already shaving off 0.5 percentage points from the inflation rate, the current figure was really bad. Of course, energy prices remain the biggest culprit, with little visibility for the next few quarters, although it seems unlikely that they will increase as much as they did in 2021.

For the European Central Bank (ECB), the underlying inflation story is more important. At 2.3%, core inflation remains above the ECB's medium-term target and second-round effects could prevent a decline. We now see headline inflation of 3.3% this year, with risks skewed to the upside. 2023 might see inflation below 2% temporarily, but at the end of the year, this threshold should be surpassed again.

ECB has become less dovish

The least one can say is that higher-than-expected inflation has increased the pressure on the ECB. In a recent interview the ECB’s chief economist, Philip Lane, stated that wage increases of 3% were compatible with the 2% medium-term inflation target. As we expect wages to pick up by 3-3.5% this year, the ECB’s target seems within reach. Lane also mentioned that the policies needed to fight very low inflation would no longer be needed if inflation remained stable at around 2%.

The February ECB press conference already sounded more hawkish, with the risk to the inflation outlook now tilted to the upside. We now believe that net asset purchases will end in September. This creates room for a deposit rate hike before the year is out, though this isn't a done deal yet. But it seems very likely that by the summer of 2023 the deposit rate will have left negative territory for good.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: The masks, and the gloves, are coming off

- This bundle contains 15 Articles