Eurozone recovery hampered by supply bottlenecks and soaring energy prices

- 7 October 2021

Although Covid-19 is now more or less under control, other headwinds are slowing the pace of the eurozone recovery: supply chain distortions have not disappeared, while surging energy prices will also weigh on growth. Inflation continues to surprise to the upside, strengthening the tapering debate within the European Central Bank

Robust growth, but slowing

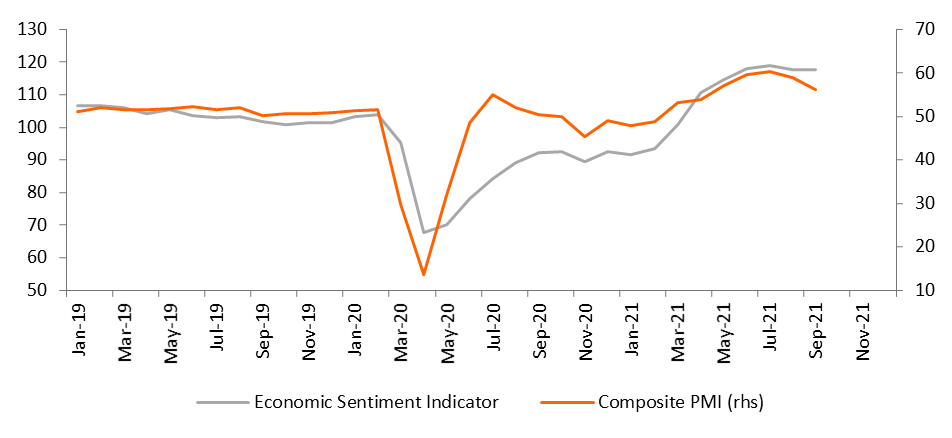

The eurozone economy faced a mixed return from the holiday season. While the Economic Sentiment Indicator staged a surprise increase in September, the composite PMI fell to the lowest level in five months. The Eurocoin indicator, a gauge for the underlying growth trend, softened to 0.75 from 0.98 in August. So it seems as if we are still looking at a rather robust recovery, though the pace of growth is decelerating. The high vaccination rate, keeping Covid-19 infections under control, certainly helps. But at the same time, we see some slowdown in the rest of the world, especially in China, which is likely to impact eurozone exports. On top of that, manufacturing continues to be hurt by low supplies of raw materials and key components, poor freight availability and port congestion.

Growth has peaked

Energy prices become a headwind

Survey data indicates that employment growth slowed a bit in September yet remained among the highest seen over the past two decades, as companies try to increase capacity. No wonder consumer confidence remains upbeat, with unemployment expectations falling rapidly. That would normally bode well for consumption in the coming months, though soaring energy prices are a growing headwind. That said, several governments have already announced energy cost support for lower income households, which should limit the damage. All in all, we see the growth pace weakening somewhat from the fourth quarter onwards. On the back of an upward growth revision for the second quarter, we have raised our GDP forecast for 2021 to 5.1%, while the 2022 outlook is slightly lowered to 3.9%.

Inflation worries

Inflation continues to surprise to the upside. The flash HICP inflation rate came out at 3.4% in September, the highest level in 13 years. High energy prices are the main culprit (natural gas prices are at a historic high), but core inflation also picked up to 1.9%. As a matter of fact, non-energy industrial goods climbed 2.6% year-on-year, probably the consequence of continuing supply chain problems and higher input costs. Looking at the European Commission’s ESI survey, companies in the manufacturing sector are planning to raise prices further while in services and construction, selling price expectations are also close to all-time highs. This makes the inflation outlook an increasingly difficult story. While in 1Q 2022 the impact of the German VAT hike will fall out of the equation, elevated energy prices and second-round effects are likely to keep inflation high. We only expect it to fall back below 2% in the second half of next year. Consequently, we have revised our inflation forecast up to 2.1% for 2021 and to 1.9% for 2022.

Net percentage of companies expecting higher selling prices very high

Tapering discussion intensifies

All of this is bound to strengthen the hawks within the ECB’s Governing Council. Board member Isabel Schnabel already prepared the ground for a tapering of bond purchases by stating that "as the inflation outlook brightens, it becomes less important how much a central bank buys or when a reduction in the pace of net asset purchases starts, but rather when such purchases end. It is the end date which signals that the conditions for an increase in policy rates are getting closer”. We expect that after the end of the Pandemic Emergency Purchase Programme in March 2022, the Asset Purchase Programme will be temporarily increased to €50b - €60b to smooth out the reduction in quantitative easing, but then be reduced again to €20b - €40b in the second half of the year. As for interest rates, we now forecast a first rate hike around the turn of the year 2023/24.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: Starting the great rotation

- This bundle contains 11 Articles