Eurozone: Hitting top speed

- 2 March 2018

We remain comfortable with our Eurozone GDP growth forecast of 2.4% this year but the pace of growth will slow a bit in the second half while political uncertainty will force the ECB to tread carefully

In his statement to the Economic Committee of the European Parliament, ECB President Mario Draghi summed it up nicely: all of the monetary policy measures taken between mid-2014 and October 2017 will have an estimated overall impact on euro area growth and inflation, in both cases, of around 1.9 percentage points cumulatively for the period between 2016 and 2020. However, the evolution of inflation remains conditional on an ample degree of monetary stimulus provided by the full set of the ECB’s monetary policy measures. In other words: growth is there, but inflation remains a work in progress.

Growth no longer accelerating but still strong

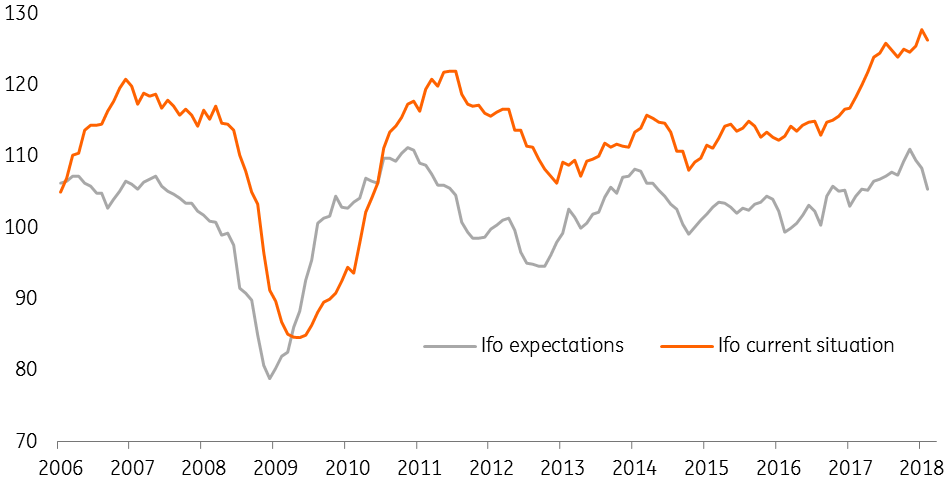

While we certainly don’t want to become bearish on the growth outlook, recent data seems to suggest that the acceleration in growth might soon start to level off. As we pointed out before, sooner or later, the strong euro had to have some impact. And that is precisely what the February German Ifo-indicator is telling us. While the “current conditions” component remained close to an all-time high, suggesting a strong first quarter, business expectations came in a lot weaker, probably pencilling in the future adverse impact of the strong euro on exports. It was the same story in the Purchasing Managers’ Index (PMI). The slower growth of business activity reflected an easing in the rate of increase of new orders which fell to a five-month low.

That said, underlying growth still seems strong enough, as companies boosted their staffing levels by one of the greatest extents seen over the past 17 years. February’s €-coin indicator even suggests an annualised GDP growth pace of close to 4.0% in the first quarter! Admittedly, consumer confidence weakened in February, but that was probably due to the financial market turmoil in the period the survey was taken. With the annual growth rate of adjusted loans to non-financial corporations increasing to 3.4% in January, from 3.1% in December, the capital expenditure outlook also looks good. So, all in all, we remain comfortable with our GDP growth forecast of 2.4% this year, though we believe that the growth pace will slow a bit, while staying above potential, in the second half of the year.

While the political uncertainty in a number of European countries might still last a bit longer (eg, it is likely going to take some time to form an Italian government), we don’t think that this will derail the recovery, though it could force the ECB to tread carefully in its exit strategy.

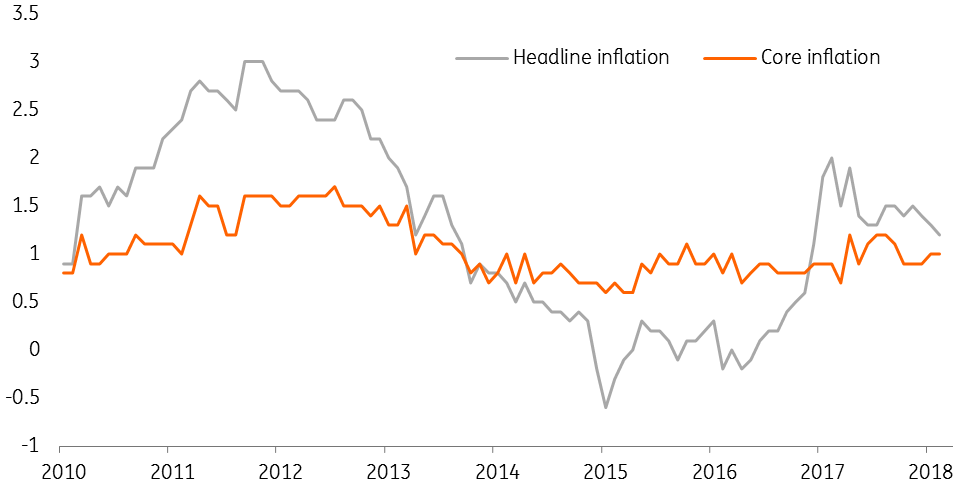

Wages are picking up but inflation is likely to rise gradually

The first German wage agreements came out on the high side of expectations, but they are unlikely to boost inflation significantly since more flexibility and productivity gains should temper the impact on prices. That said, at the current stage of the recovery, downward pressure on real wages is ebbing away in most European countries. At the same time, there is still some slack in the labour market, as average hours worked are still lower than before the crisis. So the view of a slow pick-up in inflation is still valid, though we don’t think that underlying inflation will top 1.5% this year.

Inflation is still going nowhere

Majority within ECB's Governing Council wants to delay QE decisions to avoid premature tightening

From the minutes of the last meeting of the ECB Governing Council we know that a number of members asked for the removal of the easing bias in the statement. However, the majority rejected this suggestion as it still seems premature. Indeed, already announcing an end to quantitative easing (QE) now, would most probably lead to a further strengthening of the euro and an increase in bond yields. This would then delay the return of inflation towards its target. Therefore, we believe the ECB will keep its cards close to its chest and wait as long as possible before making any announcement on the continuation or the end of the asset purchase programme.

We stand by our expectations of an extension of the ECB’s net purchases until the end of the year and a first 10bp deposit rate hike in June 2019. Bond yields, which saw a rapid rise earlier in the year, are now consolidating. While we believe that the underlying trend is still upwards, we see bond yields moving sideways over the coming months.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more