Peter Vanden Houte: Eurozone growth is already dwindling

- 1 June 2023

On the back of a weak first-quarter performance for the eurozone economy, we have downgraded our growth outlook. That said, we now pencil in two more rate hikes, as core inflation is unlikely to come down much before autumn. We might be too pessimistic about growth, though an even worse scenario cannot be dismissed either

Eurozone view: weak growth with falling inflation

Eurozone growth disappointed in the first quarter. While falling energy prices and rising wages should support consumption, the soft Chinese reopening, tighter monetary conditions and looming US recession will weigh on growth and bring the economy close to a standstill by year-end. It is mainly services that are currently thriving. The manufacturing sector is struggling with excess inventories while construction is hampered by higher interest rates. It is therefore not surprising to see that services inflation remains quite sticky, while there are budding deflationary pressures in the goods industry. But the further weakening of growth over the course of the year should bring inflation down towards 3% by year-end. As the ECB wants to see a clear decline in core inflation before ending the tightening cycle, 25bp rate hikes seem likely in both June and July, with an additional one in September a genuine risk.

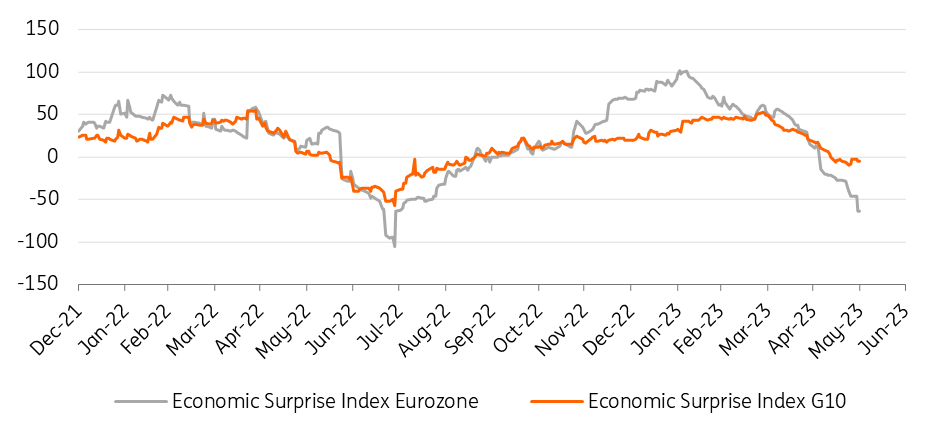

Eurozone data has been disappointing lately

Where we differ

With our 0.5% GDP growth forecast for both 2023 and 2024, we are definitely below consensus (0.6% and 1.0% respectively) and far below official forecasts (for instance, the European Commission foresees 1.1% for 2023 and 1.6% for 2024, quite similar to what the ECB is pencilling in). With our 5.4% inflation forecast for 2023 and 2.5% for 2024, we are close to consensus, but below official estimates, especially for 2024. Market forwards indicate rates plateauing at a level around 50bp above today’s level in the second half of the year, with a first rate cut in the second quarter of next year, exactly in line with our predictions.

Goldilocks after all?

We might be overly pessimistic about the growth outlook. With wages picking up and inflation coming down on the back of further falling energy prices, consumption growth could accelerate in 2024, certainly if you also pencil in a decline in the savings ratio. The weakness in manufacturing might also be short-lived: once the inventory overhang has been corrected and consumer demand for goods picks up again, manufacturing should become a driver of growth. If at the same time the US manages a soft landing and Chinese growth gathers momentum, net exports could also support the expansion.

Finally, with the European recovery plan gaining traction, public investment should add to growth. This would be a kind of goldilocks scenario, with growth accelerating and inflation falling in 2024.

Credit growth is stalling

A deeper downturn is still a genuine risk

On the other hand, it is certainly possible to come up with a stronger downturn scenario (bear in mind that we haven’t pencilled in any negative growth quarters for the next two years). What we find a bit strange, is that in the official forecasts, it seems as if tighter monetary policy does have very little effect after all – even though the ECB’s (admittedly somewhat discredited) models are forecasting a significative negative growth impact of monetary policy, both in 2023 and 2024. Also, in the past, it has been very hard for the eurozone to decouple from the US. Therefore, a US recession might hit the eurozone more than we currently anticipate.

On top of this, throw in the possibility of a credit crunch: falling house prices and an inverted yield curve will make banks a lot more cautious. So, even though we are already more bearish than the consensus, we cannot dismiss the possibility that growth turns out to be even weaker. Of course, that might allow the ECB to cut back rates a bit more strongly over the course of next year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: We’re only human

- This bundle contains 9 Articles