Power price normalisation and grids expansion in European utilities

- 29 January 2024

- Energy

The energy crisis is behind us, and the European Commission has taken action to prevent further disruption over the coming years. European utilities will continue to grow in terms of both cash flow generation and investment, but at a less hectic pace. The extremely elevated power prices seen in 2022 and 2023 are also entering into a normalisation phase

The elevated gas and power prices of 2021 and 2022 are behind us. In France, where half of the nuclear fleet was out of service for maintenance, the baseload 1y forward contract averaged €548/MWh in 2022 on the wholesale market. The lack of nuclear availability in the country added to the disruptions caused by the European economic recovery and the almost terminated natural gas procurement from Russia. With European utilities finding other gas providers, a phase of power prices normalisation started in 2023. Thanks to higher procurement from Norway and liquified natural gas resources from North America and Qatar, gas prices came back to lower and more stable levels. The natural gas TTF contract trades around €32/MWhc, far below the €300/MWh mark attained in mid-2022. For power prices, this means more acceptable tarrifs for residentials and corporates – although in 2023, they were still three times more expensive than in the 2016-2019 period.

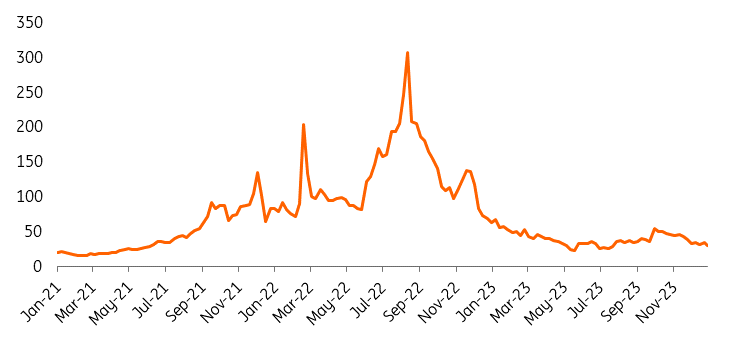

The TTF 1 Month forward contract price (EUR/MWh) has eased

Actions have been taken to avoid another energy crisis

The Dutch TTF natural gas contract (one month forward) traded around €32/MWh at the end of 2023. The price is far below what the markets experienced in 2021-2022, but still twice as much what consumers were paying in the 2016-2019 period.

The EU has opted to extend measures to tackle excessive prices

At the height of the energy crisis, members of the European Union agreed on several measures to tackle excessive prices. The Market Correction Mechanism is one of the measures adopted. It is activated if the TTF price exceeds €180/MWh for three working days, and if the TTF price is €35/MWh higher than a reference price reflecting prices on international markets for the same three working days. Despite the fact that the mechanism has never been triggered since its implementation, the EU decided to extend the measure's expiration date to 31 January 2025 (from 1 February 2024 initially). The emergency measure to enhance European solidarity through better coordination of gas purchases is extended to 31 December 2024.

The reform of the energy market design for the long term

In November 2023, The European Council and Parliament reached a provisional agreement to reform the union’s electricity market design (EMD). Overall, the reform aims at boosting fossil-free energy to cut CO2 emissions as well as maintaining energy prices at affordable levels, especially in the event of a crisis. Several elements are tackled:

- Protection of vulnerable customers: measures to protect vulnerable customers from energy disconnections have to be reinforced across EU member states. Criteria for declaring a crisis were agreed upon and measures to support disadvantaged customers with reduced energy prices to support energy affordability.

- Power Purchase Agreements (PPAs): EU members are asked to encourage long-term contracts between power generators and clients.

- Contracts for Difference: two-way contracts for difference will apply to investments in wind energy, solar energy, geothermal energy, hydropower without reservoir and nuclear energy new facilities. EU member states will have the flexibility to redistribute the revenues made through the two-way contracts.

- Capacity remuneration mechanisms: when justified, exceptions can be introduced to the CO2 emission limit for authorised capacity mechanisms. These mechanisms have to be become a more structural element within the electricity market.

Power prices will retrench further in 2024 but remain elevated

Power price expectations for 2024 shared by Standard & Poor's and some utilities point to wholesale power prices between 1.5-2 times higher than the period 2016-2019. Going back to power prices seen in the period 2016-2019 will probably not be possible in the short term unless a severe economic recession breaks out. Despite the Dutch TTF 1-month forward contract coming down to €32/MWh equivalent at the end of 2023, this price is still double compared to the pre-Covid pandemic period. In some parts of Europe, LNG shipments from the United States and Qatar have taken over the gas flows originally coming from Russia – but at a higher cost.

In the UK and Italy, power prices being 1.5 times higher than in the period 2016-2019 would result in an average price just above €90/MWh. In France, the electricity price in the period 2016-2019 averaged €48/MWh. Prices being 1.5 times higher in 2024 would result in an average power price of €77/MWh.

The average power wholesale 1Y forward contract (EUR/MWh) should decrease again in 2024

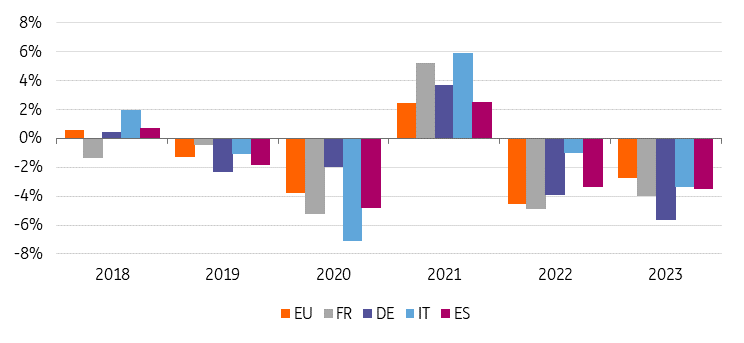

Elevated prices and a sluggish economy could continue to destroy electricity demand

Electricity consumption experienced another decline in 2023. Globally, the European Union saw power demand falling by 2.8% in 2023 after a 4.5% fall in 2022. Germany saw the biggest power demand destruction last year with a 5.6% collapse.

Elevated power prices keep retail and corporate consumers aware of the cost of their energy bills. The economic recovery in 2021 after the pandemic shutdowns resulted in a strong power demand in countries such as Italy and France where restrictions were drastic. The increase in electricity prices in 2021/2022 led to retail consumers restricting their energy use. Across Europe, energy intensive industries limited their activities (and sometimes shut down factories) to avoid loss-making.

In their top three calls for the eurozone, our economists remain cautious on the outlook for spending, penciling in just 0.8% growth for 2024 (compared to a forecast of 1.6% by the European Central Bank and 1.2% by the European Commission). Consumption growth is likely to be limited by the turn in the labour market, with a gradual increase in unemployment limiting aggregate income growth. Even with a much more benign inflation backdrop, we expect eurozone consumption growth to remain subdued in 2024, keeping GDP growth below 0.5%.

A sluggish economy in the eurozone and power prices that retrench but remain elevated on a historical basis could see another year of power demand destruction. We would not be surprised to see another year of negative growth for power demand in 2024 – although we could expect the decrease to be less severe than in 2022 and 2023.

Power demand has been negative in the last five years (%YoY change)

European utilities’ cash flow generation to progress again

In 2024, we expect that European utilities’ cash flow generation will continue to progress. We estimate the sector’s EBITDA to be on average around 7% stronger in 2024 compared to 2023. This increase comes from past investments bringing new projects online, higher remuneration on regulated grid activities and for some margins normalisation for their trading segment.

| +7% |

average sector EBITDA growth in 2024 |

For the top 20 integrated utilities, we estimate their EBITDA to grow by around 5% on average. The growth corresponds to new renewable capacity coming online. Most integrated utilities also operate grids and will benefit from increased remuneration. Apart from a few utilities too dependent on Russian gas procurement, the sector has seen two years of extraordinary financial results derived from very high power prices. Utilities with a substantial portion of electricity produced by renewables benefitted from low cost generation which they could sell at elevated prices on the retail and wholesale markets.

In their 9M23 result publications, several European utilities informed analysts and investors of decreasing electricity prices. Consumers are locking in lower contract prices already. Power prices that are 1.5 times higher on average than during the stable period seen in 2016-2020 still mean comfortable cash flow generation in 2024 for the power generation business of integrated utilities – but also the start of a decline that will spread itself across several years due to the hedging strategies.

Regulated network activities to drive the growth for the sector

For the top 20 grid utilities, we forecast an average 9% EBITDA growth in 2024 vs. 2023. The elements that contribute to this strong increase are:

- Large investments that inflate utilities’ regulated asset base and thus remuneration;

- Continued recouping of past costs;

- Inflation passthrough for utilities evolving in regulatory framework allowing inflation corrections;

- Revised WACC and/or remuneration formulas to account for higher cost of debt and/or higher costs in general.

| +9% |

average EBITDA growth in 2024 for European gas and power network operators |

Several regulators revised the remuneration of grid utilities in recent months. The low cost of debt during the period 2018-2021 – especially in Central and Northern Europe – negatively impacted regulated network utilities’ cash flow generation. Remuneration either stagnated or even decreased, while an important financial effort was requested for the sector to develop and adapt its network assets to accommodate the transmission and distribution of renewable power and gas.

The hike in the post-Covid cost of materials and the energy crisis in 2021 and 2022 dramatically changed the operational cost conditions of European corporates, including network utilities. Added to this were rate increases impacting financial markets and the yield paid on new debt issuance. Some corrections were brought to the remuneration formulas (quite often based on a WACC methodology) and while 2023 already saw some recouping of costs occurred in the past, 2024 will see remunerations going up again in several European countries.

- Belgium: Still with a cost-plus model, the national electricity transport company Elia Belgium will benefit from strong tariff increases in the coming years. Over the period 2024-2027, the tariffs the utility can charge to its users will grow by 77% with an average return on equity set at 7.2% instead of the average 6% in the period 2020-2023.

- Germany: In June 2023, the German regulator Bundesnetzagentur (BNetzA) announced a regulatory return on equity (ROE) increase to 7.09% pre-tax (or 5.78% post-tax) for new onshore investments. The remuneration for grid assets built before 2024 will remain at 5.03%.

- Italy: in November 2023, the Italian regulator ARERA published the final determination for the new allowed WACC for electricity and gas networks for 2024. The revision of the risk-free rate, the country risk premium and the sovereign bond yields led to higher weighted average cost of capitals (WACCs) for most activities. On average, WACCs will increase by 80 basis points. For instance, regulated assets for power transmission activities will be remunerated at 5.8% instead of the 5% set for the period 2022/2023. Gas distribution activities will be remunerated at a 6.5% WACC, which replaces the 5.6% in the former regulatory period.

- The Netherlands: in its tariff methodology 2022-2026, the Dutch regulator (ACM) determined an average nominal WACC of 3% for the network utilities operating on the territory. The cost base is the year 2020. The initial methodology includes an average inflation of 1.7% per year and an average cost of debt around 0.5%. After court actions, the Dutch transmission and distribution utilities obtained a revision of their remuneration. In 2023, the WACC was brought up to 4% and will reach 4.5% in 2024. The cost base is now the year 2021, which offers a better picture of the operators’ cost structure. The recouping of past costs will again boost the regulated utilities’ cash flows in 2024, something much needed given the large investment plans that need to be executed. For consumers, the bill for network services averaged €380 in 2022. In 2023, the amount climbed to €513 (+35% vs. 2022) and is expected to be slightly above €600 in 2024 according to our calculations.

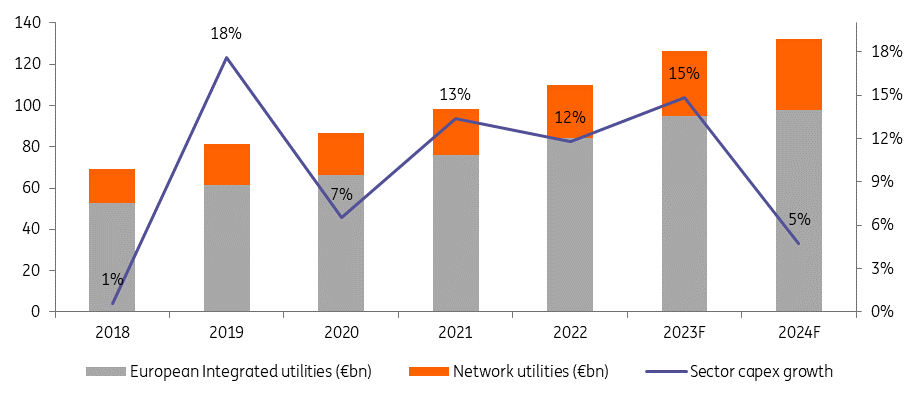

A milder investment increase in 2024

In 2024, the top 40 European utilities* will invest a total of €132bn in the maintenance and development of their grids, renewable base and conventional energy generation assets. According to the utilities’ strategic plans and our estimates, this global amount compares to €126bn for the full year 2023, representing a 5% growth year-on-year.

*The top 40 European utilities: A2A, Acea, Alliander, Amprion, Centrica, EDF, EDP, Elia Belgium, Enagas, EnBW, Enel, Enexis, Engie, E.ON, Eurogrid, Fingrid, Fortum, Fluvius, Fluxys, Hera, Iberdrola, National Grid, Naturgy, Nederlandse Gasunie, Redeia, Redexis, REN, RTE, RWE, Snam, Statkraft, Stedin, Suez, TenneT, Terna, Orsted, Vattenfall, Veolia, Verbund, Viergas

Sector average capex growth (%)

| +5% |

average investment growth for the sector in 2024 |

Looking back to the period 2018-2022, the sector’s investment plans have grown by a staggering average of 11% per year going from c.€70bn in 2018 to €110bn in 2022.

The 5% increase that we forecast for 2024 is therefore less important than what we have seen in the last five years. We see a couple of reasons for that:

- Investments reached exponential expansion in the period 2021-2023 and the growth is now slowly returning to a more average level (especially for integrated utilities).

- With (renewable) projects more expensive, as seen with Orsted and Vattenfall, European utilities become more selective as they want to secure appropriate levels of return on investment.

Higher costs result in a more selective approach toward renewables

Just like many industries, soaring commodities and material costs have impacted the Utilities sector. Purchasing costs for renewable equipment, especially offshore wind farms, have made some utilities renouncing some of their projects.

Recently, the Danish utility Orsted announced depreciation of €2.1bn on its US offshore wind farm projects. Soaring costs, higher interest rates and uncertainty on related subsidies have had a dramatic impact on expected return on investment. Vattenfall, the Swedish incumbent, inaugurated its offshore windfarm on the Dutch coast but announced it was suspending the development of its 1.4GW Norfolk Boreas offshore wind farm programmed to power 1.5mn UK homes.

Offshore wind farm development is now 40% more expensive than seen previously

According to the Swedish utility, costs on the project have increased by 40%, negatively impacting the company’s future earnings.

The Italian incumbent Enel presented its new strategic plan in December 2023, in which investments in renewables for the period 2024-2026 are revised downward, especially for onshore wind. With higher returns, Enel decided to allocate more capital expenditure in its regulated network activities.

In September 2023, the UK failed attracting bids for its offshore wind power auctions. Offshore wind developers argued that the government’s offer did not match the surging costs and higher funding expenses. The same reasons explain the poor auction results that Spain registered in December 2022. Only 50MW of wind projects were subscribed when the authorities planned to allocate 3.3GW of new onshore wind power and solar panels.

Several European utilities have a foothold in North America where they operate power plants (renewables and/or conventional energies) and sometimes transmission/distribution networks. The US has been amongst the favourite places for developing renewable activities thanks to attractive fiscal policies.

In the last few months, major European players such as Orsted, EDP and Enel have announced US disposals, mostly concerning wind projects and sometimes solar and geothermal. In its 2024 renewable energy industry outlook, Deloitte underlined the good performance of the solar industry which saw installed capacity growing by 36% in 2023. At the same time, additional capacity from wind projects came at 2.8GW, 57% down compared with 2022. The consultancy firm cites an average cost increase of 50% for wind projects between 2021 and 2023, which led to a diminishing pipeline. The difficulties in obtaining permissions and connections to the grids are other reasons for the disaffection for wind projects.

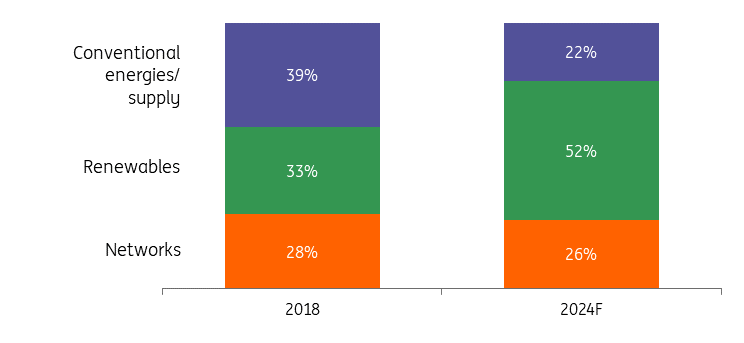

Despite higher costs, the development of renewable capacity remains a key focus

The shift of European integrated utilities' business model from conventional energy generation producers and suppliers (coal, natural gas and nuclear) towards renewables is reflected in past and future investments. In 2018, 33% of total investments were dedicated to renewables. We forecast renewables to represent 52% of total investment in 2024. With conventional power generation plants being shut down or disposed of, capital expenditure for this segment is on a significant decline from 39% in 2018 to 22% in 2024. Despite higher costs, European utilities remain committed to delvering on their carbon emission reduction targets.

European integrated utilities' investments per segment

Developing renewables portfolios through acquisitions will progress again if funding costs abate

While the priority has shifted to selecting projects that will guarantee a decent return on investment, European utilities continue to be largely involved in the development and operating of renewable power plants. The reshuffling of portfolios through asset disposals or asset rotation to achieve higher returns on investments comes alongside new project developments as well as acquisitions. The difficulties in developing renewable projects are acknowledged by most utilities. Timeframes for obtaining the necessary permissions, the extensive administration tasks, higher material and staff costs and the delays in connecting the new power plants to the grids have been hurdles for the sector.

European utilities such as RWE, Engie and Elia have been active on the M&A market in 2023, with the acquisition of local players that offer a pipeline of projects already in place. The advantages of M&A activities allow utilities to avoid parts of the hurdles inherent to the several phases between the conception of a project and its operation.

The period between 2018-2022 saw a strong increase in merger and acquisition activities concerning “alternative energies”. The figures for 2023 point to a weaker year and, although the number of deals were in line with those seen in 2022, the amount in EUR terms fell significantly to €11.4bn. As the next section explains, funding costs significantly increased for corporates, making it more difficult for M&A opportunities to materialise. We would expect M&A activities for the sector to grow again if funding costs lessen.

M&A volumes for alternative energies in North America and EMEA declined in 2023 on higher funding costs

Financing costs sharply increased

Due to its capital intensive nature, the European utility sector is a heavy user of bank loans and bonds. While parts of investment need to be financed by new financial instruments, utilities also face loans and bonds redemptions. On top of higher operating costs, the sector has to finance parts of its capital expenditure and refinance its debt at much higher interest rates than in the last five years.

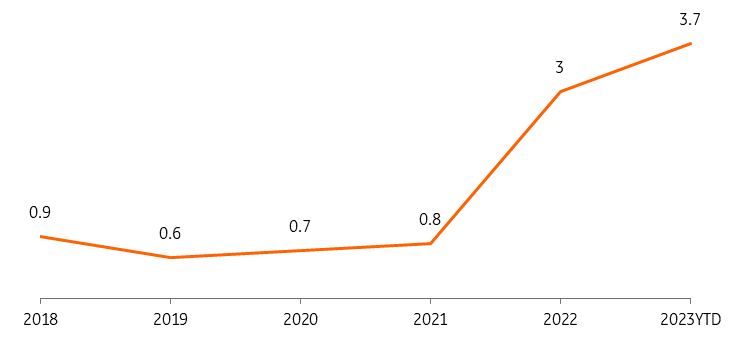

Today, the sector pays an average of 3.7% in yield for a five-year senior bond. In 2022, this yield was 3% on average. In the period 2018-2021, utilities could issue five-year senior bonds with an average coupon of 0.8%. Our ING rates strategists believe that the European Central Bank will start cutting rates over the course of 2024 and that a “neutral” 2-2.5% rate by the end of 2025 could be achieved.

Average yield paid by utilities on new debt issued on the EUR bond market (%)

Financial leverage remains a concern

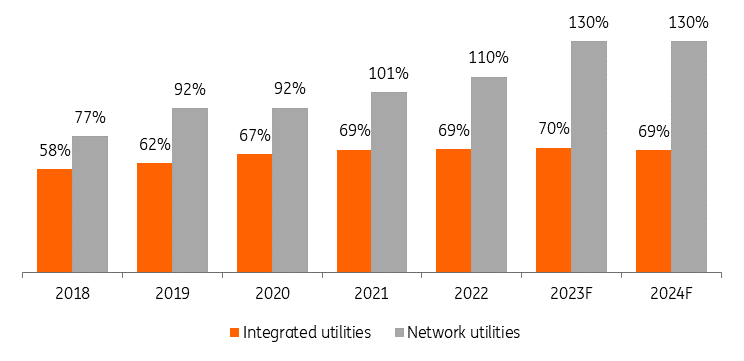

Parts of capital expenditure plans are financed by debt, especially for network utilities whose regulated cash flow generation does not provide them with the sufficient funds to finance investment plans. In 2023 and 2024, we deem network utilities’ investment plans to surpass earnings before interest and depreciation (EBITDA) by 30%. For integrated utilities, earnings are sufficient to finance capital expenditure needs. However, EBITDA represents the revenues generated by the activities taking into consideration operating costs and operating taxes. The financial indicator does not take into consideration interest expenses on financial debt, and the remuneration of shareholders.

Capital expenditure to EBITDA ratio (%)

Due to the funding needs of European utilities (especially network utilities) we do not expect the sector to improve its financial leverage ratios. 2024 should see the beginning of a phase of normalisation for power and gas prices. Nevertheless, the geopolitical situation in the Middle East could bring volatality to the markets in case of escalation. The sector seems to be better prepared today in the case of an energy crisis.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Energy Outlook 2024: High ambitions, steadier speeds

- This bundle contains 6 Articles