European Utilities: A bittersweet year for earnings

In 2025, the European utility sector’s cash flow generation will remain strong but will mark another contraction due to still-elevated power prices though these are now in a normalisation phase. Pure grid operators, meanwhile, will see cash flow generation expanding again

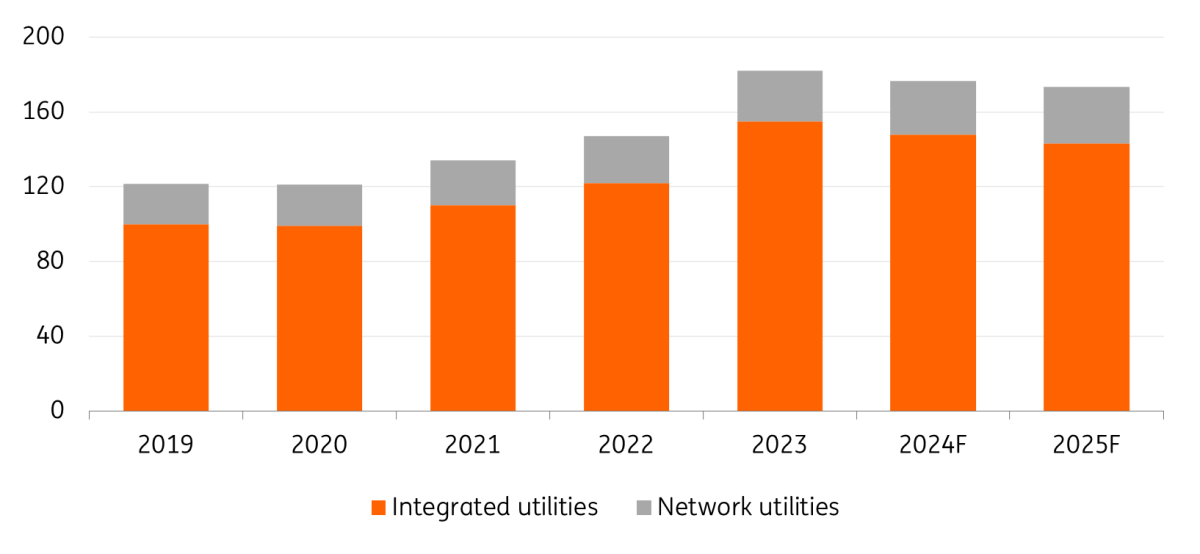

Except for some outliers, European utilities’ cash flow generation grew considerably between 2021-2023 on the back of surging power prices and demand catching up after the Covid-19 pandemic. Altogether, the top 40 European utilities1 expanded their earnings before interest, taxes, depreciation and amortisation (EBITDA) from €134bn in 2021 to €183bn in 2023 with integrated utilities driving the strong growth. Within the sector, the sub-segment represented by pure grid operators saw its cash flow generation progressing at a slower pace with a growing remuneration linked to higher interest rates and a larger regulated asset base.

1 Top 40 European utilities

Call 1: Small earnings contraction for the sector in 2025

2024 was a pivotal year with the beginning of a normalisation in power prices. For the full year 2024, the European Utility sector should see an EBITDA decrease of 3% vs. 2023. According to their guidance for 2025, the top 40 European utilities will generate an aggregated €173bn in EBITDA, representing a 2% reduction in cash flow generation compared with 2024.

| -2% |

Sector's EBITDA in 2025 |

European integrated utilities, whose activities stretch from grid operations, power generation, supply and customer services, are mostly responsible for the sector’s EBITDA contraction. On aggregate, the top 20 European integrated utilities2 guide to cash flow generation declining by 4% in 2025. Nevertheless, the picture is rather polarised. The business profile of the players matters. The least diversified utilities will tend to feel the full impact of the normalisation in European power prices. This is the case for most German and Nordic integrated utilities. On the other hand, others will continue to benefit from growth thanks to a well-diversified business profile including activities in North and South Americas, for instance, where energy needs are rising at a faster pace.

On the pure grid operators’ side, the top 20 network utilities3 will continue to see their cash flow generation expanding (+6% in 2025) on the back of growing asset bases and supportive regulatory frameworks (although not in every country).

2 Top 20 European integrated utilities: A2A, Acea, EnBW, Enel, Centrica, CEZ, EDF, Enel, Engie, E.ON, Fortum, Hera, Iberdrola, Orsted, RWE, Statkraft, Suez, Vattenfall, Veolia, Verbund

3 Top 20 European network utilities: Alliander, Amprion Elia, Enagas, Enexis, Eurogrid, Fluvius, Fluxys, Italgas, Fingrid, National Grid, Nederlandse Gasunie, Redeia, Redexis, REN, RTE, Stedin, Snam, TenneT, Terna

After a strong expansion, the top 40 European utilities' EBITDA will decline again in 2025

Call 2: Power prices have retrenched but should stay elevated in 2025

The vast majority of power generators sell at least 90% of their future power generation a year ahead of production. The current wholesale forward contracts generally impact utilities’ cash flow generation 12 to 18 months later as payments are received when the contracts are executed.

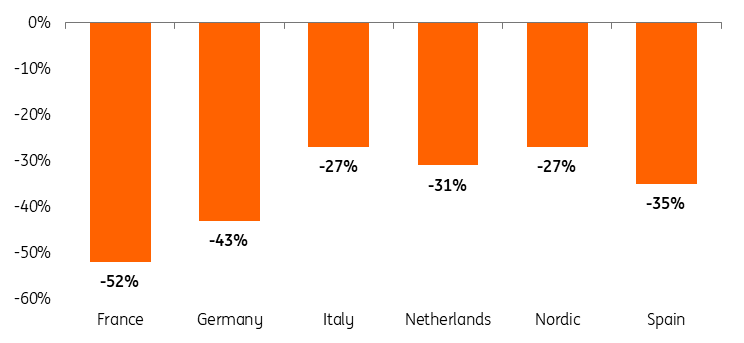

In 2024, on a 12-month average, the wholesale 1Y forward contract was sold at €77/MWh in France, a 52% decline compared with 2023 when the average stood at €162/MWh. In Germany, the contract dropped by 43% from €140/MWh to €80/MWh on average. Electricity prices declined substantially but are still above the averages seen before the Covid-19 pandemic when contracts were signed between €40 and €50/MWh. All European countries registered lower wholesale electricity prices. European players found ways to diversify their natural gas procurement and a large part of the French nuclear fleet came back into operation.

Average wholesale prices significantly declined between 2023 and 2024

Wholesale power prices should evolve in the same range in 2025

The price level at which European utilities hedge their power production in 2025 will impact their cash flow generation in 2026. Business and retail consumers will also feel the impact in 2026-2027 as their contracts are being readjusted on a rolling basis.

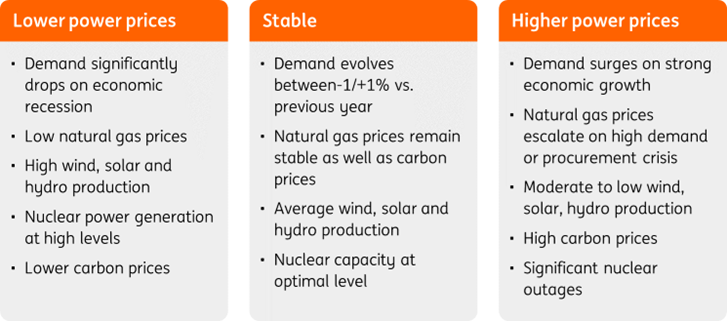

The energy crisis in 2022 was the result of a perfect storm. As in our scenario ‘Higher power prices’, demand surged as economic activity came back to normal levels after the peak of the pandemic. The conflict between Russia and Ukraine and the procurement issues that it created sparked the acute crisis. At the same time, France’s nuclear power fleet is running at very low capacity (more than 50% of its nuclear park was out of operation due to repair work).

We believe that our central scenario “stable” is the most plausible for 2025. Prices should evolve around the same base as seen in 2024. Power demand in the European Union should remain sluggish with modest GDP growth for most EU members. The French incumbent, EDF, the biggest power generator in Europe, has revised its nuclear power production upward from 315-345 TWh in 2024 to 335-365 TWh in 2025. While production will meet domestic demand, it will also allow production to be sold to neighbouring countries. Natural gas prices, characterised by volatility, could be the trickiest element. Even though the Dutch TTF contracts regained strength in 2024, our commodities strategists expect prices to somewhat retrench by the end of 2025 on higher liquefied natural gas (LNG) supply from the US. Despite higher volumes being a positive, a higher share of LNG supply within the European natural gas mix also means prices remaining at a certain level given more expansive procurement costs in comparison to Russian gas.

Scenarios for electricity prices

Electricity demand remains sluggish

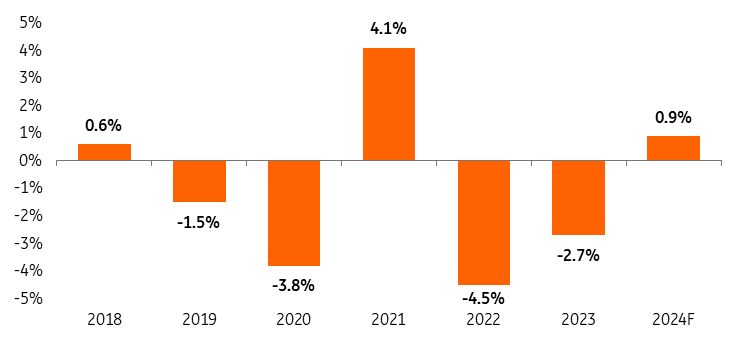

Demand plays a role in determining power prices. The large recovery of electricity consumption across the European Union (+4.1%) in 2021 after the first wave of Covid infections influenced power prices. Following the recovery, 2022 and 2023 registered a significant decline in demand due to extremely elevated prices leading to consumers applying energy-saving strategies.

Data provided by ENTSO-E, the association representing 80 European power transmission operators and publishing statistics, suggests power consumption was up by 0.9% in 2024. Before the energy crisis, power demand fluctuated between +1% and -1% at the European level. With more than 70% of the power demand coming from industry, transport and commercial services, 2025 consumption will again largely rely on the bloc’s economic health. Signs of weaknesses seen already in Germany and France may not bode well for growth above the average seen before the Covid-19 pandemic. In the longer term, electricity consumption growth should be supported by electrification. To mitigate the costs of the energy transition, some governments have adopted less supportive policies including the cancellation of subsidies for electric cars. Such actions may delay the energy transition and the expected growth in electricity demand in the EU.

In 2024, power consumption increased by a mere 0.9%

Natural gas prices will remain volatile

Natural gas prices have played a large part in elevated power prices in the last few years. Even though about 50% of Western Europe’s electricity generation now comes from renewables, natural gas used by power plants has been the marginal cost for power generation, especially since coal has become a smaller resource for the utility sector. Pre-Covid-19, the Dutch TTF 1-year forward contract was traded in the range of €10-20/MWh. The conflict between Russia and Ukraine has had a significant impact on the natural gas market. August 2022 marks the highest spike in the Dutch TTF month forward contract with a price reaching €307/MWh. Since then, the price of the contract has tightened, and in March 2024, it was sold at €27.3/MWh. This was due to procurement issues being resolved, thanks to increased flows from Norway and LNG shipments from the US. Nevertheless, the price of the TFF contracts has remained volatile in the last three years and after the price retrenchment in 2023/2024, natural gas prices started to expand again to reach €49/MWh in the first week of January 2025.

The TTF 1M Forward contract has retrenched significantly but some volatility remains (€/MWh)

Weather conditions have led to lower reserves at the European level. In the first week of January 2025, reservoirs were filled at c.69% and for countries such as the Netherlands and France, this level fell as low as 55%. The confirmation of the ending of the contract between Ukraine and Russia for transporting gas to Europe via Ukrainian pipelines added to the stress on natural gas prices. Our ING commodities strategist, Warren Patterson, predicts the TTF 1-month forward contract will trade at an average of €40/MWh in the first quarter of 2025 and €35/MWh by year-end. The LNG market is expected to add supply, with the US seeing new LNG projects coming online and adding c.15% in volume to current production. These price predictions hinge on the timely execution of these projects, as well as weather conditions that may either increase or decrease the urgency to refill reservoirs at a faster rate.

The elements influencing the power prices hedged by European utilities make the forecasts a difficult task. European utilities will publish their year-end 2024 results in February and March 2025 and their guidance should confirm (or potentially not) our stable scenario with wholesale power prices remaining at similar levels to those seen in 2024.

Call 3: Pure grid operators still benefiting from supportive regulatory frameworks

Within the sector, network utilities will see their EBITDA in 2025 growing by c.6% on average, a growth rate in line with 2024. The elevated capital expenditure programmes add new assets to the regulated asset base of grid operators. This base is the operators’ assets that are used to provide regulated services such as power lines and gas pipelines. The regulated asset base usually serves as the base for regulated remunerations under allowed rates of return. Network utilities can also operate assets and provide services that do not fall under the determined regulated asset base.

| +6% |

of EBITDA increase for pure grid operators in 2025 |

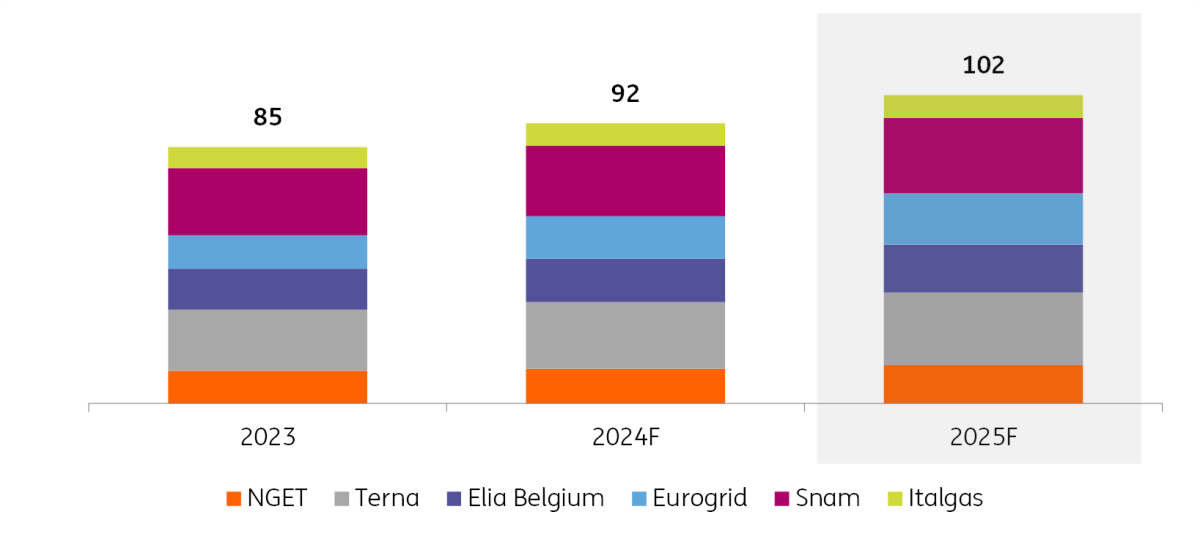

In our article “European Utilities in 2025: big investments and bigger debt,” we describe the European utilities’ investment plans for 2025. The sector will see investments growing by an average of 9% in 2025. The sub-segment top 20 network utilities will grow by an average of 12%, meaning that grid operators will see the biggest capex expansion again next year. Based on National Grid Electricity Transmission (NGET), Terna, Elia Belgium, Eurogrid, Snam and Italgas, the aggregated asset base of the six network operators will increase by c.11% in 2025 in comparison with c.8.5% in 2024.

Regulated asset bases grow significantly (€bn)

Regulated networks' remuneration will continue to be supportive in 2025 but could start to fall thereafter

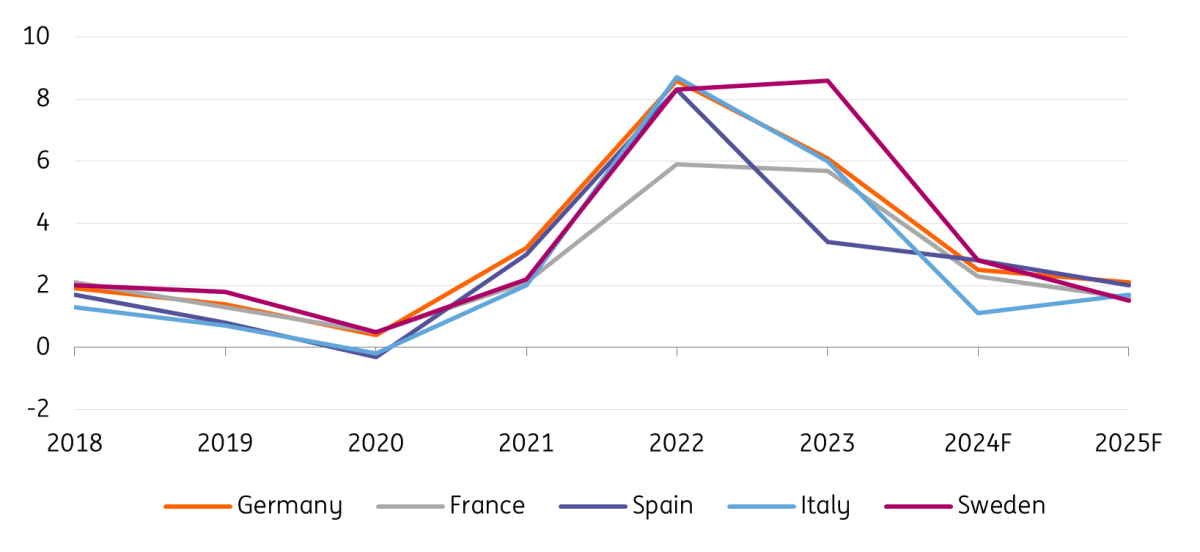

Regulated remuneration on assets generally takes into consideration the operators’ determined operating costs, cost of debt and cost of capital. In the period 2018-2022, European regulators tightened their frameworks with the aim of reducing baseline allowed returns as the companies’ cost of debt significantly declined. The measures were also designed to counteract the higher returns seen in previous cycles and implement stricter cost controls on the utilities’ operating expenses. From 2023 onward, the lower remunerations became inadequate in a number of countries. To operate their grids, utilities are themselves high energy users and with skyrocketing power prices in 2021-2023 and global hyperinflation, operating costs surged.

Consumer price indices (%)

Alongside higher costs to operate their networks, corporates also saw their cost of debt increasing again in 2022 and 2023. Except for Spanish and Portuguese utilities, regulated frameworks allow for inflation passthrough. In 2024 and 2025, corrections for past inflation, capital and cost of debt will permit the sub-sector to continue growing its remuneration. The picture could start changing in 2026 as inflation and corporates’ cost of debt have declined significantly. However, regulators should keep in mind that the energy transition requires very large investment needs and good remuneration is essential to maintain a debt burden at acceptable levels.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

22 January 2025

Energy Outlook 2025: Growth amid challenges This bundle contains 7 Articles