European telecoms set to see modest growth in 2026

- 26 January

- TMT

We view 2026 positively for the European telecom sector. Sales should grow by 2% due to new services and price increases. EBITDA growth is likely to be a bit higher because of cost rationalisation efforts. We do not see investment coming down a lot because of the need to upgrade mobile networks to 5G Standalone and to extend fibre to more customers

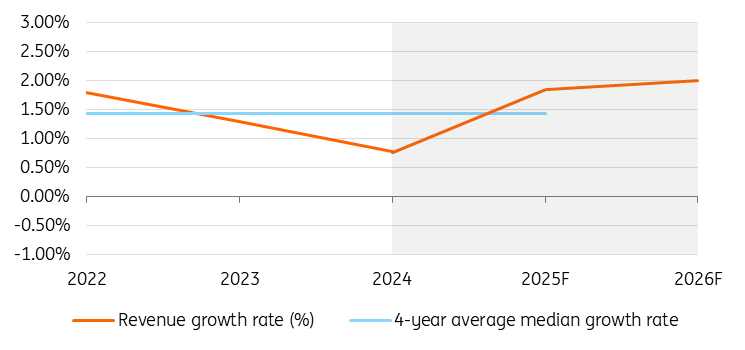

2% revenue growth does not suggest plain sailing for telcos

The waters look calm in the telecom space. However, companies need to work hard to maintain their top-line growth, especially in markets with many operators. We see competition coming from new satellite services and new fibre operators, often competing on price. Also, in the business segment, we continue to see the impact of over-the-top services, like Teams and WhatsApp. Telecom companies have to step up their game to bring competitive packages to small and medium-sized businesses. KPN offers a good example of a company that has renewed its SME offers.

Our expectation for 2% top-line growth, therefore, comes from the sale of new services, like bigger bundles, higher speeds, or low-latency gaming packages, but also from some price increase. However, revenues will be held back by discounts to new customers and price pressures in the value segment. Furthermore, we expect Average Revenue Per User (ARPU) to remain relatively low in markets such as Italy and Spain. There is also a risk of lower ARPU in Belgium coming from the new entrant, Digi.

A few companies, such as Altice France, will find it hard to maintain profitability, lowering the overall outlook. This profitability challenge for some operators is partly driven by a regulatory framework that fosters intense competition in certain countries, in our view.

Expect 2% revenue growth

EBITDA to grow faster than revenues as costs can be cut

Manual switchboards are long gone, and automation has steadily reduced operating costs for telecom operators ever since. We expect this trend to continue in 2026. Be it through the copper switch-off, network automation, or a more efficient customer service, with the use of AI. Companies such as Telefonica and BT have announced reorganisation programmes, while Telia is working on one.

But we also see higher costs, stemming from investment in AI tools, reorganisation costs, the development of new 5G services, and sometimes elevated subscriber acquisition costs. All in all, we expect EBITDA growth to outpace revenue growth by 0.5% and see median EBITDA growth among European telecom operators of about 2.5%.

EBITDA growth to outpace revenue growth

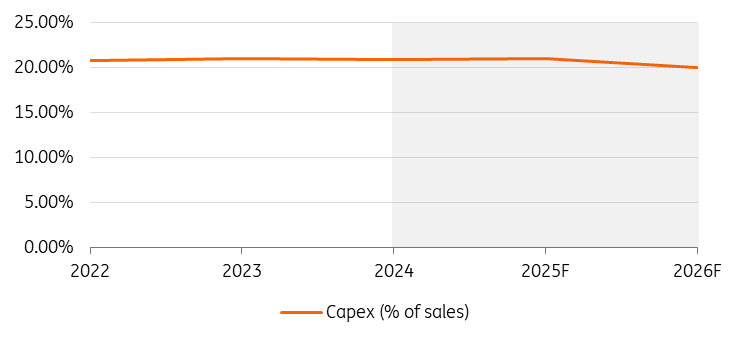

Capex remains high, but could surprise on the low end

We have read some upbeat messages that cash flows could increase this year on lower capex. According to this view, free cash flow may expand because of lower investment needs now that the fibre rollout is coming to an end in some countries. This argument has merit. However, it ignores the fact that operators may want to roll out networks in remote areas, while they still need to connect the homes passed. And this comes at a cost.

In our view, until now, investments in fibre have been prioritised over investments in 5G standalone networks. We expect investments in 5G SA to become a priority now. Also, further costs will come from investments in new mobile sites or upgraded antennas and the development of new AI services. We expect median capex-to-sales numbers to be in the 20% area.

Capex will likely trail off a bit, but not much

A solid 2026 outlook but higher growth in non-regulated industries

Although the above points to solid cash flow generation, these are far from the growth rates of the large technology platforms. This may be a disappointment for some, but can be explained by the infrastructure-like returns, and also by the regulatory framework, limiting product and pricing differentiation, and limiting the ability to sell advertisements.

Nevertheless, we think our forecast shows that the telecom sector matches the business fundamentals sought by corporate fixed income investors.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Telecoms Outlook 2026: Communicate, work and play

- This bundle contains 6 Articles