European rescue alphabet soup and market impact

- 2 April 2020

- Rates

The past few weeks have seen a flurry of proposals for EU members to jointly finance the coronavirus-related fiscal costs. We look at the latest proposals, how they compare, and how they would be received by EUR rates markets

An attempt at taxonomy

Given the number of unknowns and lack of political agreement, it is pointless to go into too much detail about each of them. It is worth having a general taxonomy in mind, however. The proposals can be categorised along two axes. Firstly, how much of a fiscal transfer do they amount to (in €), and secondly for how long. The holy grail in terms of supporting the more vulnerable member states is of course a large package of help with permanent transfers.

SURE but not very significant

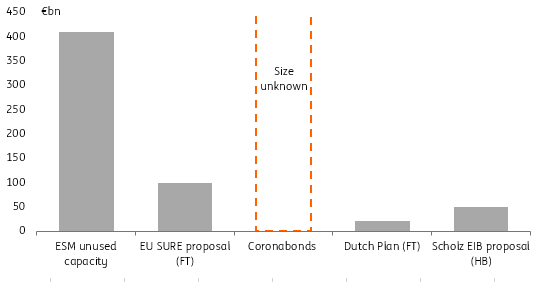

The EU's SURE proposal floated in the FT yesterday, from what we can tell, doesn't rank very highly on either axis. To be sure, €100bn of loans (with the largest three recipients unable to borrow more than €60bn together) is a step in the right direction, but it compares with the European Stability Mechanism's firepower of over €400bn. Similarly, the length of the loans is unknown but each member state's exposure would presumably be limited to the amount of guarantees provided. According to the same source, they should total €25bn and would be weighted by the size of each country's economy.

Rescue measures: the patchwork approach

This is perhaps the greatest advantage to this proposal. Its limited size and (apparently) lack of conditionality make it a more likely tool to be implemented. We see no reason to think this could not be used in addition to other measures, such as the ESM's Enhanced Conditions Credit Lines (ECCL) or European Investment Bank loans in principle. Indeed, according to Handelsblatt, German Finance Minister Olaf Scholz is open to combining SURE bond issues with additional EIB and ESM loans. It is likely that contributing member states would look at their total additional liabilities under all the proposals on the table however.

The options on the table

Alphabet soup and market impact

Market reaction to the proposal has been positive but we warn against overstating its significance. Granted, even an additional €20bn loan each to Italy and Spain would be a step in the right direction but this compares to what our economics team estimates will be €70bn of additional financing needs for 2020 alone in Italy. Note also that this option is inferior to the ESM ECCL in one additional respect: it is not a pre-condition for the European Central Bank to start the Outright Monetary Transactions.

We argue that €20bn less BTP issuance alone would be of no great relevance for Italian yields, and that additional Germany guarantees to the EU and EIB would fail to move Bund yields. Add some ESM loans to these figures and one starts to have a decent budget relief for affected countries in the near term, but their liabilities would remain their own.

Fiscal transfer would reverse the divergence in borrowing costs

Interestingly, semi-core sovereign primary markets stand to be most affected from the plan. If the ESM borrowing is any guide, and we think it is, the markets most likely to be ‘crowded out’ are existing ‘E-names’ (EU, EIB, EFSF, ESM), and France. With respect to ECB purchases, what would be spent on SURE bonds would not be spent on other supranational, agencies or sovereign bonds.

This seems like an ever more distant prospect now but any progress on an instrument with more explicit fiscal transfers, even if capped and limited in time, would be a lot more significant for European yield. In addition to the direct substitution of liabilities between member states, it would encourage hope, or fear depending of where you stand, of greater fiscal and economic coordination in the future, thus chipping away at the very reason why borrowing costs differ from one member state to the next.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

In case you missed it: Undone by a pandemic

- This bundle contains 11 Articles