The euro sell-off after the ECB: All a bit much?

- 14 June 2018

- FX

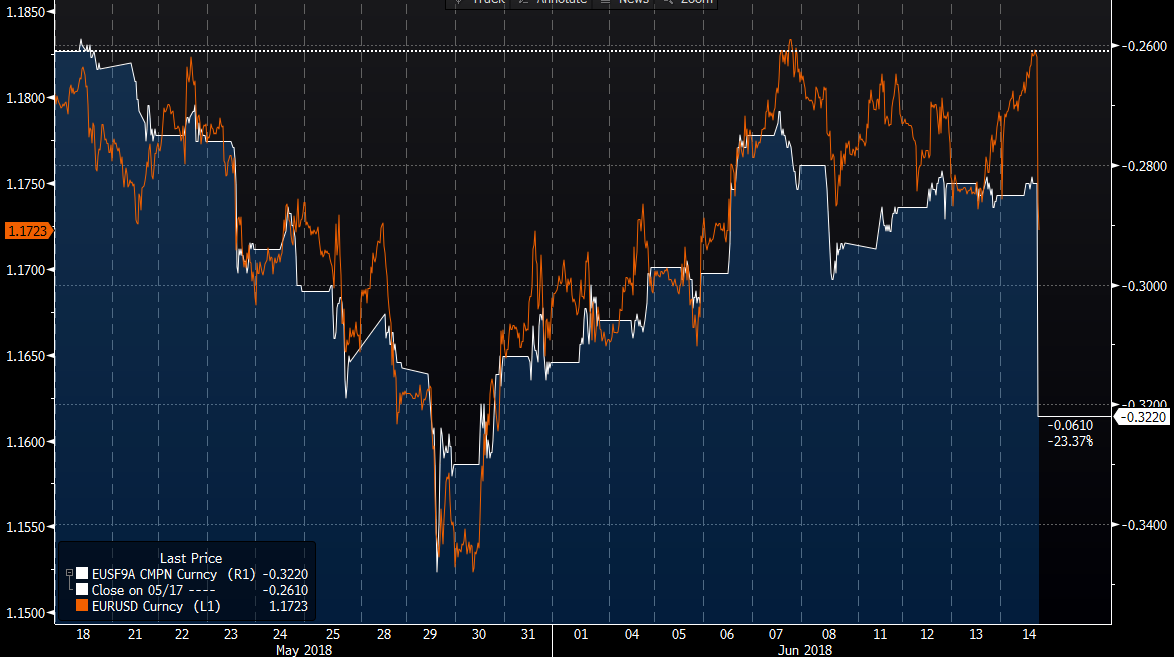

EUR/USD has sold off hard on the announcement that the ECB ‘anticipates’ ending QE in December this year and keep rates unchanged at least through the summer of 2019. This has come as a disappointment to the rates market, which had priced close to 10bp of ECB rate hikes by June 2019. The EUR sell-off feels a bit much, though

Will the end of QE be the bigger priority?

While the forward rate guidance should see US:EU policy divergence continue for another twelve months, this story looks largely priced in and it feels like the euro sell-off is a bit of an over-reaction. Of course, the ECB has to manage the exit from QE very carefully – which they’re doing through aggressive forward guidance. But we tend to think that, over time, the announcement of the end of QE will emerge as a bigger story – and that in the last quarter of this year and 1Q19 the short end of the EUR curve can start to narrow the spread with its US counterpart. EUR/USD should be pushing back above 1.20, possibly to the 1.25 area by that time. Helping this story should be the return of portfolio flows - particularly long-term debt portfolio flows - to the Eurozone. These were sent off-shore by the ECB's QE programme starting in 2015 and the anticipation of their return should support the EUR over the coming 1-2 years. In general, we see the lower end of EUR/USD trading range in the 1.15/16 area this summer.

EUR/USD v June 2019 pricing for EONIA

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

In Case You Missed It: Confidence and cracks

- This bundle contains 7 Articles