EUR: Draghi’s managed float

- 29 June 2017

- FX

Expectation management exercise lifts the euro

Draghi uses benign conditions to nudge market expectations

ECB President, Mario Draghi’s speech in Portugal June 27th looks very much an exercise in expectation management, taking advantage of benign financial conditions to remind the market that Eurozone monetary conditions stand to move to a less accommodative setting over coming quarters.

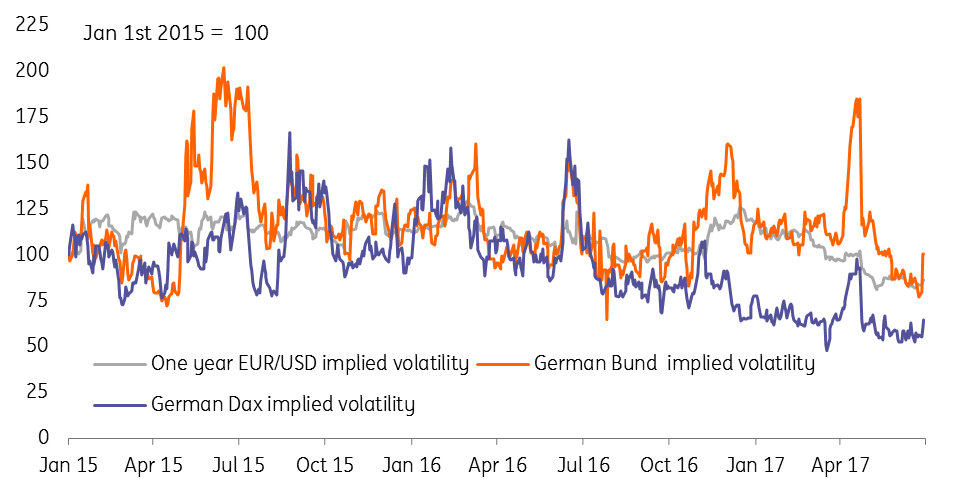

The speech was delivered when Eurozone cross market implied volatility – a gauge for expected volatility – was at multi-quarter lows and could be well-absorbed by financial markets.

Implied volatilities of EUR/USD, Bunds and Germany’s DAX index at multi-quarter lows

Bund bubble deflates

Draghi’s comments shifted the focus from deflationary to reflationary forces and had the desired effect on the euro and bond markets. In our opinion, the ECB is well-tuned to market sentiment through a variety of market contact groups and had a good idea of the impact of those comments on EUR and Eurozone bond markets. The move in German Bund yields (around +15bp at the time of writing) has lifted the EUR (and European currencies) across the board and validated our baseline EUR/USD call, that an ECB tapering-driven upside break-out in German Bund yields in 3Q17 would drive EUR/USD to 1.15.

Draghi's comments shifted the focus from deflationary to reflationary forces

Options market seems ill-positioned for a summer rally in the EUR

It looks to be an exciting summer ahead for the EUR. The very short term focus will be on the June 30th release of flash Eurozone CPI data for June. Our Eurozone team and the market expect an energy-driven drop in the headline rate to 1.2% YoY from 1.4% in May. Core inflation is expected to edge up to 1.0% YoY from 0.9% YoY.

Over the remainder of the year, our team look for some weak upside in headline CPI to the 1.4/1.5% YoY area and core nudging up to the 1.3% YoY area. The direction of travel in prices may gently support the ECB’s position of a gradual removal in monetary accommodation – but does not look an intense catalyst.

We think it is fair to characterise the market as ill-prepared – or ill-positioned – for a summer rally in the EUR

Despite this we think it is fair to characterise the market as ill-prepared – or ill-positioned – for a summer rally in the EUR. We judge this by the state of the FX options market, which can tell us how market participants (e.g. multi-national corporates and asset managers) are hedging their EUR/USD risk.

Notably the Draghi-driven spike in EUR/USD above 1.13 drove short-dated (1m) volatility to 7% from 6.4% and saw the Risk Reversal Skew – the difference the market is prepared to pay for a 25 delta EUR call versus an equivalent EUR put – move sharply in favour of EUR calls. This is evidenced in both the term structure of the EUR Risk Reversals and also the fact that EUR risk reversals in the 3m tenor are moving to favour EUR calls for the first time this decade. In short the market feels the need to buy upside protection in EUR/USD.

It looks to be an exciting summer ahead for the euro

Risk Reversal Term Structure makes a decisive move

Baseline forecasts

As per our May 9th update, our baseline EUR/USD forecasts are outlined below. While EUR/USD may stall around the 1.14/15 area near term without fresh catalysts, we would probably say that upside risks exist to our forecasts - particularly in the 3Q17 window when the ECB tapering debate will come to a head.

For reference, those forecasts see EUR/USD move to 1.15 in 3Q17 and then staying there - limited by Italian elections and perhaps a fiscal-induced dollar rally in late Summer - until 2Q18, when we look for EUR/USD to break up to 1.20.

The ECB believes its monetary policy measures have contributed to reducing Eurozone long run risk-free rates by 80bps

ING’s house call is for Bund yields to rise to 0.60% by the end of 3Q17. It is also worth noting that the ECB believes its monetary policy measures have contributed to reducing Eurozone long run risk-free rates by 80bps – serving as a reminder that the timing of the normalisation of Euro benchmark rate curves will be one of, if not the most, definitive market calls over the next 12-24 months. Following Draghi’s speech, markets will now be on full alert for tapering signals at the July 20th ECB meeting, while a formal decision may well be taken on September 7th.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more