EU carbon hits year-to-date lows

- 17 November 2023

- Commodities, Food & Agri Energy

EUAs have been trending lower for much of this year. Weaker demand, increased renewables and the front loading of allowances has seen the market trade down to its lowest levels this year

EUA Dec-23 price (EUR/t)

EUAs fall on demand pressures

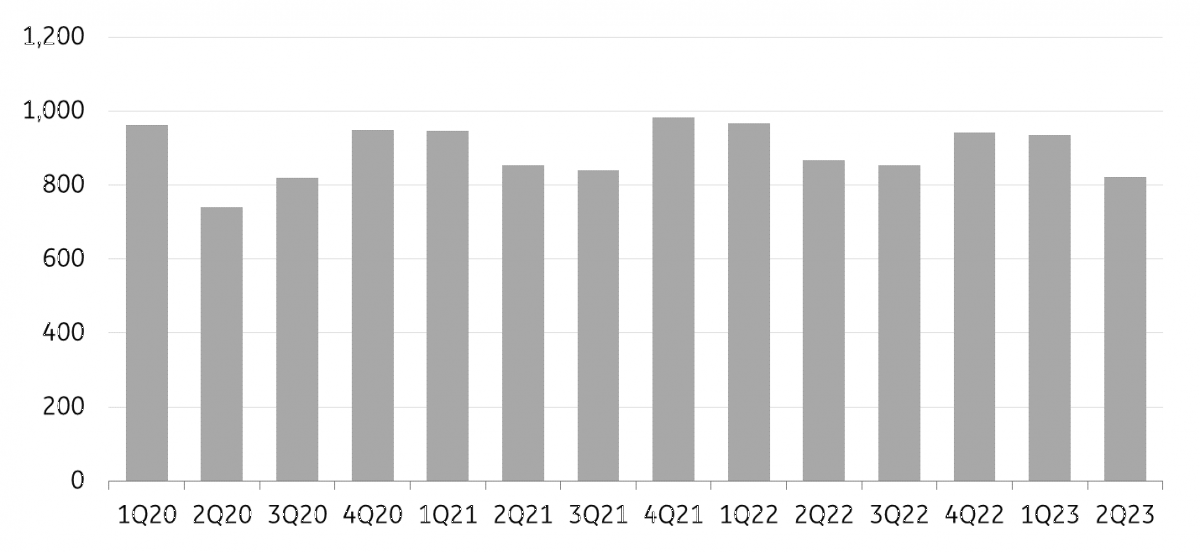

In November, EU Allowances (EUAs) traded down towards EUR75/t, the lowest levels seen this year. And this is after the market briefly broke above EUR100/t at the start of the year. By function, the longer-term outlook for EUAs remains constructive as allowances in the market are reduced. However, shorter-term dynamics are also important. In the current environment, it is probably no surprise that demand for allowances has been lower. The EU has seen reduced industrial activity, which means lower emissions and the need for installations to surrender fewer allowances. Eurostat data shows that emissions in the second quarter of this year fell 5.3% year-on-year to 821mt CO2 equivalent – the lowest levels since the third quarter of 2020. Emissions over the first half of this year totalled 1.76b tonnes CO2eq, down 4.2% YoY.

EU greenhouse gas emissions fall (mtCO2eq)

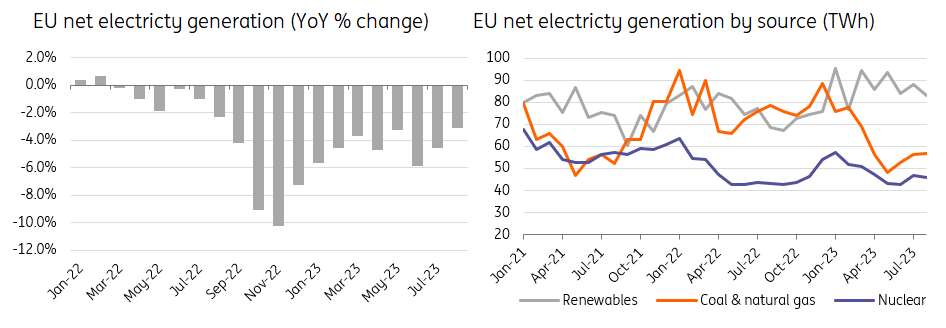

If we look at the power sector, in addition to overall power generation having fallen this year we have also seen changes in the power mix. Renewables output has been strong, and in France nuclear power output has also recovered, therefore reducing the number of allowances needed. EU electricity generation has been in a YoY decline since March 2022. Net generation over the first eight months of the year is down 4.5% YoY. Generation from coal and natural gas over this period is down a significant 20% YoY, whilst renewables (including hydro) are up 11% YoY.

Looking ahead, this is not expected to change anytime soon. Both forward spark and dark spreads are firmly in negative territory in the coming months, suggesting that power generation from natural gas and coal will remain under pressure through the 2023/24 winter. This all suggests that EUA prices are likely to remain subdued in the short term.

EU electricity generation falls, while renewables output grows

Front loading of allowances doesn’t help

Supply dynamics have also played a role in pressuring EUAs, dimming the short to medium outlook. This is partly due to REPowerEU, which aims to end the EU’s reliance on Russian fossil fuels by diversifying energy sources, energy savings and accelerating the roll-out of renewables. Part of the REPowerEU plan is set to be funded by the Recovery and Resilience Facility (RRF) through the sale of ETS allowances. The Commission’s aim is to raise EUR20 billion from allowance sales. 40% of these funds are set to be met by bringing forward the auction of allowances scheduled to be auctioned between 2027-2030. These will now be brought forward to before 31 August 2026. Meanwhile, the remaining 60% will be met by sales of allowances from the Innovation Fund.

The EEX auction calendar shows an additional 35.3m allowances are to be auctioned in 2023 for the RRF, whilst auction regulation from the Commission shows 86.7m allowances to be auctioned in both 2024 and 2025 and 58m allowances in 2026 for the RRF. This adds up to a total of 266.7m allowances, which equates to EUR20.5b at the current allowance price of around EUR77. At current prices, we would only need to see a little less than 260m allowances to be auctioned to hit the EUR20b revenue target.

While the short-term outlook remains subdued and the medium-term outlook less bullish than originally envisaged, the longer-term picture remains bullish. Ambitious targets under Fit for 55 mean a more aggressive reduction factor will be used for allowances moving forward. A reduction factor of 4.3% per year will be used between 2024 and 2027 and 4.4% between 2028 and 2030. This compares to a previous linear reduction factor of 2.2%. In doing so, the Commission hopes to see emissions under the ETS fall 62% from 2005 levels by 2030 compared to a 43% reduction target previously. This is also slightly more aggressive than the proposed 61% reduction.

Furthermore, to help hit the target there will be two one-off reductions in the cap, effectively reducing it by 90m allowances in 2024 and a further 27m allowances in 2026.

Shipping falls under ETS from 2024

1 January 2024 will also see the shipping sector fall under the EU Emissions Trading System (ETS). Initially, carbon emissions from all large ships (above 5,000 gross tonnage) entering EU ports and transporting passengers or cargo for commercial purposes will fall under the ETS. Large offshore ships will be included from 2027. There will be a phase-in period where shippers will only have to surrender allowances for 40% of their emissions for 2024, 70% for 2025 and 100% for 2026 emissions. Furthermore, only carbon emissions will be included from 2024, but from 2026, methane and nitrous oxide emissions will also be included.

As for geographical scope, 100% of emissions will be covered for intra-EU trips and those that fall within an EU port, whilst 50% of emissions will be covered for extra-EU voyages that either start or end in an EU port.

The inclusion of the shipping sector in the EU ETS will see 78.4m allowances added to the ETS, which will be subject to the same reduction rate as the wider ETS. This compares to total ETS-applicable emissions from the maritime industry in 2022 of 83.4mtCO2e.

CBAM reporting gets underway

1 October 2023 saw the start of the trial period for the Carbon Border Adjustment Mechanism (CBAM), where importers of goods in the scope of CBAM have to report the embedded emissions within those imports. CBAM will initially apply to cement, iron and steel, aluminium, fertilisers, electricity and hydrogen.

Then, from 1 January 2026, not only will importers need to declare the quantity of goods imported into the EU in the preceding year and their embedded emissions, but they will also need to surrender the corresponding number of CBAM certificates which is linked to the EU ETS price. The phasing-out of free allocations of EU ETS allowances for these sectors in the EU will take place in parallel with the phasing-in of CBAM in 2026-2034.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more