ESG Omnibus: Throwing the baby out with the bathwater

- 23 January

- Financial Institutions Sustainability

Now that the EU has finalised the sustainability Omnibus, we analyse the changes and impact these will have on European banks. This will be a positive for banks which are no longer required to report on ESG but significantly complicate disclosures for those still in scope

The background

At the start of 2025, the European Commission proposed an overhaul of the EU’s sustainability reporting directives. What followed was a year of debates, diverging proposals and unprecedented political alliances. The sustainability Omnibus (or Omnibus I) was eventually approved by the European Parliament in December 2025. While some have welcomed the simplification and anticipate productivity gains for corporates, we believe the impact will be less positive for European banks.

An Omnibus to streamline EU sustainable reporting directives

So, what does the first Omnibus actually change? It targets three sustainable reporting policies: the Corporate Sustainability Reporting Directive (CSRD), the Corporate Sustainability Due Diligence Directive (CSDDD) and the European Taxonomy.

Using an Omnibus package (the Union’s legal mechanism for merging and streamlining multiple regulations), the EU simplified the three policies. However, by doing so, the essence of these has also been altered. In the next section, we review the changes before diving into the impact these will have on European banks.

What changes with the sustainability Omnibus?

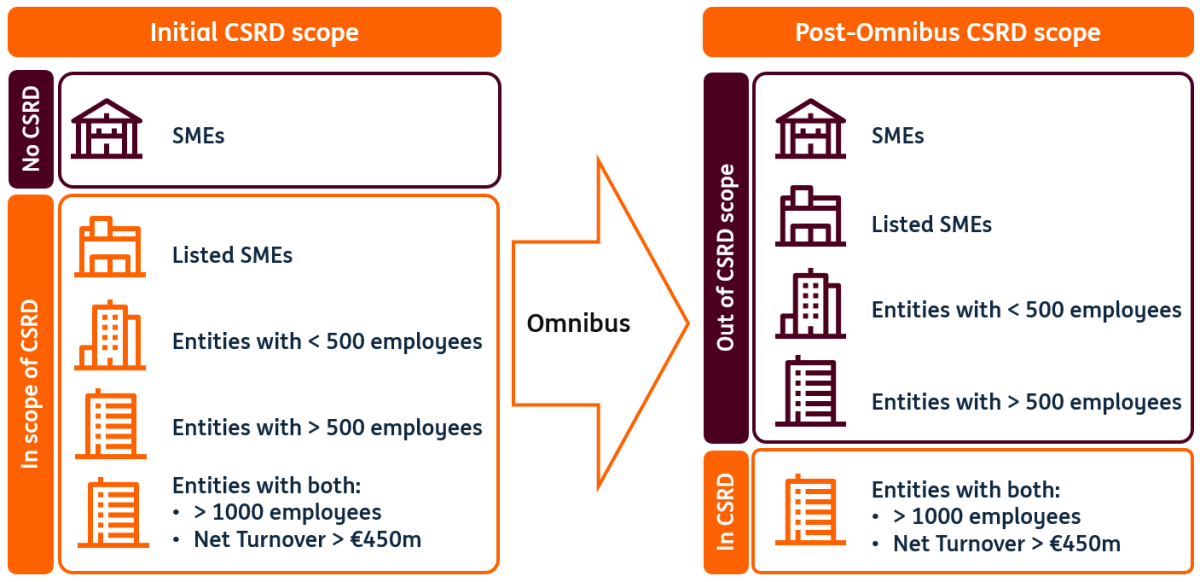

CSRD: A massive scope reduction

The initial proposal by the European Commission introduced an 80% reduction to the CSRD scope. The final text goes further than that, with an estimated staggering scope reduction of 90%. Indeed, the CSRD will now only include entities with over 1,000 employees and with a net annual turnover of over €450m.

The revised Directive also introduces new thresholds for non-European entities operating within the Union. Only those generating more than €450million in annual net turnover in the EU will fall within the scope of the CSRD. Subsidiaries and branches of non-European entities will be required to report under the CSRD once they exceed €200million in net turnover generated in the EU.

The graph below summarises the changes compared to the scope that the CSRD was initially supposed to cover.

Reduction of the CSRD scope for EU entities

In addition to the scope reduction, the Omnibus I also introduces changes to (but not exclusively):

- Data requirements: a simplification of the framework by reducing the number of data points to collect as well as focusing on quantitative information and deleting sector-specific disclosures (made voluntary). The European Financial Reporting Advisory Group (EFRAG), in charge of drafting the new European Sustainability Reporting Standards (ESRS), submitted its proposal to the Commission at the end of last year. The Commission now has until June 2026 to finalise the simplified set of reporting standards.

- The value chain cap threshold has been raised to protect companies with less than 1,000 employees from having to provide information to larger business partners (that are required to report their sustainability information). The protection of smaller companies is a negative for banks as they inherently rely on their clients’ data to build their own sustainability reporting, but we will come back to this in the section focusing on the impact on banks.

CSDDD: A delayed implementation

The final sustainability Omnibus also introduces significant changes to the CSDDD scope by drastically reducing it to only include entities with over 5,000 employees and a net annual turnover of over €1.5bn. The financial threshold also applies to non-European entities operating in the EU. Importantly, the revision delays the implementation of the Directive until 26 July 2029.

In addition to these two changes, the CSDDD review also alters the essence of the initial Directive which aimed to increase supply chain transparency. Indeed, European entities remaining in scope of the CSDDD will not have to disclose information on their entire supply chain but instead only identify and disclose violation risks detected. Also, the changes specify that companies should request information from entities not in scope only when the data cannot be obtained in another way.

Aside from the scope reduction and the inclusion of a risk-based analysis of the value chain, the Omnibus I also (among other things):

- Removes the requirement to establish transition plans

- Removes the European-level civil liability clause

- Implements a maximum fine of 3% of the entity’s net worldwide turnover in case of infringements.

European Taxonomy: simplified reporting and materiality threshold

The European Taxonomy is also impacted and simplified by the sustainability Omnibus.

However, as it is enforced at the Union level through the Taxonomy Disclosures, Climate and Environmental Delegated Acts, the legislative process differed from the CSRD and CSDDD.

The Commission published an initial proposal in July 2025 after which the Parliament and Council had six months to review it. This period ended at the beginning of January, and the Commission officially published and applied the new rules as of 1 January 2026. That being said, entities have the option to introduce these changes in 2027 (for the financial year 2026), giving them a year to introduce the changes in their reporting.

The text includes five main changes to the original Delegated Act:

- Introduction of a materiality threshold: Activities representing less than 10% of the entity’s net turnover, CapEx and OpEx are considered “non-material” and are exempted from Taxonomy eligibility and alignment assessment. However, those should be reported separately as “non-material”. The Commission justifies the materiality threshold as a tool to allow undertakings to focus on the most significant part of their activity.

- Operational expenditure exemption: When the operational expenditure (OpEx) KPI is immaterial for the entity’s business model, the undertaking is exempted from assessing Taxonomy eligibility and alignment for the KPI. Instead, it is only required to report the total value of operational expenditure without any further assessment.

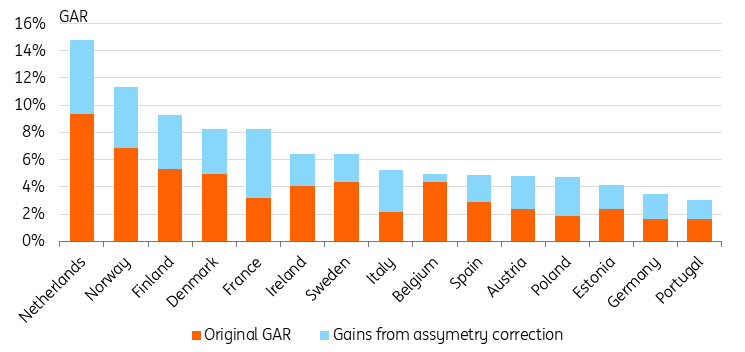

- Simplification for financial institutions: KPIs for financial undertakings (such as the Green Asset Ratio (GAR)) will exclude, from the denominator, exposure to entities falling out of scope of the sustainability reporting requirements. The GAR asymmetry has been a central criticism since the start of its enforcement as it mathematically brought down the results. The significant reduction of the CSRD scope and consequent adjustment of the denominator should resolve that issue. However, we don’t expect the change to significantly improve the average GAR result. Indeed, using banks' Pillar 3 disclosures from end-2024, our calculation shows less than a three percentage point increase in banks’ GAR on average. Dutch banks would see the largest increase in average GAR with a 5.5 percentage point gain. The delegated act also contains the exclusion from the denominator: derivatives, cash and cash equivalents, on-demand bank loans, goodwill and commodities. The inclusion of trading book KPIs and Fees and Commission KPI is postponed until 2028. The reviewed Delegated Act also allows financial undertakings not to disclose the detailed Taxonomy templates until 31 December 2027. Instead, banks can, during the period, publish a statement indicating that they do not claim that their activities are associated with environmentally sustainable activities under the EU Taxonomy.

The GAR asymmetry correction is expected to have only a limited impact on results

- Reporting template simplification: The Delegated Act lays out a simplified reporting template reducing the number of data points from 78 to 28 or a 64% reduction for non-financial entities and 89% for financial undertakings. It also introduces the removal of the separate annex on the performance and exposures to the fossil gas and nuclear activities.

- Do No Significant Harm simplification: The text also introduces the simplification of the DNSH criteria for pollution prevention and control related to chemicals. However, it only targets those technical screening criteria but does not change the ones related to the objectives of climate change mitigation and adaptation. The Commission plans to further review the European Taxonomy in the second quarter of 2026. Additional changes to the DNSH criteria are therefore expected this year.

While these changes simplify Taxonomy disclosures, the largest impact stems from the reduction of the enforcement scope. Indeed, Taxonomy disclosures are mandatory for all entities falling under the Corporate Sustainability Reporting Directive (CSRD).

Following the major scope reduction of the CSRD introduced with the sustainability Omnibus, only entities with over 1,000 employees and a net annual turnover above €450m will be required to disclose their Taxonomy eligibility and alignment.

What does it mean for banks?

The Omnibus I was introduced with the aim of simplifying reporting and allowing corporates and financial institutions to boost productivity. However, in this section, we review the various ways this will affect EU banks and highlight what we see as (at best) ambiguous impacts for the sector. We identify three main impacts: (1) smaller banks falling out of scope, (2) lower data availability and (3) regulatory discrepancies.

Smaller banks falling out of scope

Starting with the change of the enforcement threshold, we estimate the number of credit institutions that would be exempt from the CSRD and Taxonomy disclosures.

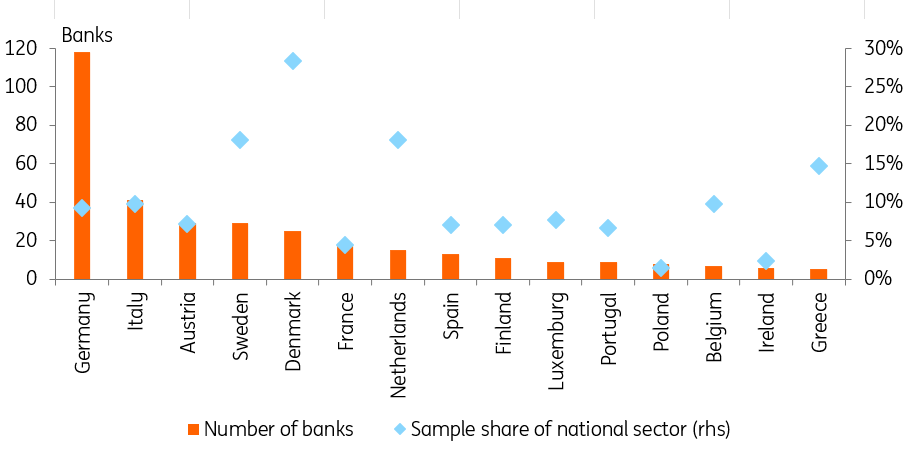

To do so, we compiled a sample of over 340 banks from 15 EU Member States. It includes both globally significant institutions (under the direct supervision of the European Central Bank) and smaller banks (supervised by their national regulator). Despite some variations, on average, our sample captures just above 10% of all financial institutions nationally.

Number and share of banks included in our sample

For each financial institution, we collected data on the number of employees and the latest net turnover metric available (revenue for banks). Using the thresholds adopted in the sustainability Omnibus, we estimated the number and share of banks that will fall out of scope of the CSRD and consequently also of the European Taxonomy disclosures.

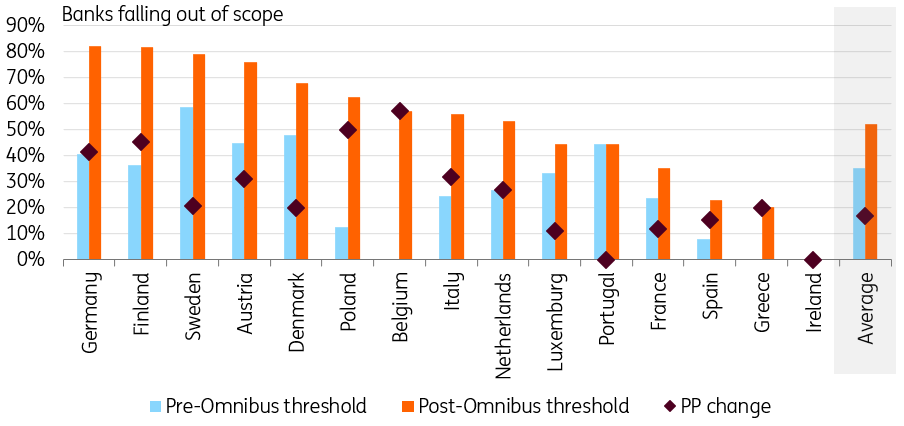

When the legislative process for the sustainability Omnibus started, the first wave of disclosures was already in place. It included all entities with over 500 employees. Looking at our sample, it implies that nearly 220 banks were already in scope and had to disclose both the CSRD and ESRS in 2025 (for the financial year 2024). Consequently, about 35% of our sample was already outside the scope of the CSRD before the Omnibus proposal.

Unsurprisingly, this share increases significantly with the new threshold. On average, now about 52% of the sample falls out of the Directive’s scope. More importantly, this share rises to 80% of the national sample of banks in countries like Germany, Finland and to over 70% in Sweden and Austria. This reflects the structural characteristics of these jurisdictions, where the banking sectors are made up of a large number of smaller institutions. This contrasts with other jurisdictions such as Ireland, Greece, Spain and France, where the banking sector mostly comprises larger institutions. Therefore, these countries see their share of banks not required to disclose remain below the 50% mark.

Share of banks falling out of scope of the CSRD

The massive reduction of the CSRD scope will therefore directly benefit banks that were included in the first wave of enforcement but are now falling out of scope of the disclosures. These institutions will see their reporting burden drop. For the smaller financial institutions that were going to start reporting with the second implementation wave, this also results in a reduction in their reporting requirements and puts an end to a year of regulatory uncertainty.

That being said, for banks still in scope, this will have the opposite impact by complicating compliance through more complex data collection. We further discuss this point in the next section.

More complex data collection

Considering that banks inherently rely on their client’s data for their own sustainability disclosure, the significant scope reduction will adversely affect institutions still reporting. Research estimates that only about 6,000 companies will still be required to disclose their sustainable information under the CSRD following the Omnibus. This represents a 92% drop from the initial scope of the Directive.

While corporates that are not required to report on their ESG data can still do so through voluntary disclosures, the change implies that the bulk of banks’ corporate clients will not have to gather or share their information. That is specifically true as the ‘value chain cap’ protects any entity not in scope of the CSRD from being forced to disclose information to any business partner requesting it (thus including banks).

In the event that the banks’ clients are collecting and willing to share data gathered through the voluntary disclosure framework, this doesn’t ensure that it will cover all necessary data points and can imply major disparities between disclosures in terms of both data points collected and the reporting quality.

To address this, banks have two solutions: Firstly, they can develop bilateral agreements with their clients to gather and share the necessary data points. However, considering the data collection cost for clients, it remains difficult to imagine this as a viable solution.

Secondly, financial institutions could make use of more proxies in their report to compensate for the lack of data from their clients. While this solution would offer the benefit of limiting costs, the current state of the Directive limits the use of such proxies. To be a realistic option, the regulator should review and loosen those limits to allow a broader use of these methods. Additionally, relying on proxies could raise questions about the reliability of the data, as it would not accurately reflect the true state of banks' books.

To conclude, even if some corporates may still choose to voluntarily collect and disclose ESG data, the sustainability Omnibus increases the reporting complexity for banks still in scope. This could translate into both higher costs and lower quality disclosures.

Regulatory discrepancies

The finalisation of the Omnibus I answers questions related to the enforcement scope after a year of legislative uncertainty. However, it raises new questions for banks.

It is now clear that most banks will not have to disclose their ESG data under the CSRD. It is also certain that institutions still in scope will have to disclose fewer data points and that reporting standards will be simplified by mid-2026. That being said, the simplification did not affect all ESG disclosures that credit institutions are subject to.

Indeed, under the Capital Requirement Regulation (CRR), banks are also required to disclose sustainability-related information. More specifically, the Pillar 3 reporting requires banks to collect and share a significant amount of ESG data. Unlike the CSRD and the Taxonomy, these requirements were not part of the sustainability Omnibus and therefore not subject to any simplification yet.

The European Banking Authority (EBA) proposed some changes to the Pillar 3 requirements and launched a consultation in 2025 with the aim of aligning Pillar 3 disclosures with the Omnibus package, reflecting the scope reduction. While the consultation concluded, the EBA hasn’t implemented changes to reflect the Omnibus simplification, at this point in time.

Banks are therefore left stuck between a rock and a hard place with, on one side, fewer and simplified requirements and on the other side, unchanged regulations. As long as a discrepancy between the various ESG disclosures exists, banks will have to collect the same amount of ESG data. This occurs while banks receive less information from their clients - and when data is provided, it is often of lower quality.

A successful simplification or a baby thrown out with the bathwater?

Our analysis of the sustainability Omnibus points to ambiguous impacts on the European banking sector. While the smaller financial institutions will benefit from falling (or remaining) out of scope of the CSRD and Taxonomy, those remaining in scope will not see this as a positive.

The main channel through which the Omnibus I will negatively affect banks still in scope of the sustainable disclosure is the data quality and availability. As the overwhelming majority of corporates are now out of scope of ESG reporting requirements, banks will not have access to these necessary data points.

In addition to the difficulty of gathering the data, one may question the quality of the information still available and shared, especially through entities’ voluntary disclosures. Overall, this will have a negative impact on bank reporting both in terms of cost and quality of the final disclosures.

While the reporting burden related to the CSRD and Taxonomy might be lowered through the simplification, banks are still subject to other regulatory requirements, also including ESG data points.

These regulations have not been simplified yet and don’t reflect the changes brought by the Omnibus I. Therefore, banks are faced with heightened discrepancies between ESG requirements - all while having reduced access to clients’ data. The EBA suggested changes to its Pillar 3 requirements to adjust to the Omnibus and lower the discrepancies, but the finalisation will still take time.

While the existing versions of the CSRD and the European Taxonomy were far from perfect, one can question whether the changes brought by the sustainability Omnibus will really benefit financial institutions. More importantly, these changes have, in several respects, altered the very essence and original purpose of the Directives. While the CSRD and the Taxonomy were designed to channel greater investment towards sustainable activities, the extent to which that objective survives this wave of simplification is now open to question. Did the Commission succeed in simplifying the overly complex ESG disclosure requirements or did it throw out the baby with the bathwater?

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Bank Outlook 2026: Bank funding and exposures in motion

- This bundle contains 7 Articles