European utilities to see steady currents in 2026

- 22 January 2026

- Energy

For the European utilities sector, trends observed in 2025 are continuing into 2026. For integrated utilities, cash flow generation is set to stabilise. For pure network operators, remuneration continues to grow with regulated asset bases that are expanding. Investments should rise by 6% on average for the sector, but with disparities among players

Call 1: The sector's cash flow generation stabilises

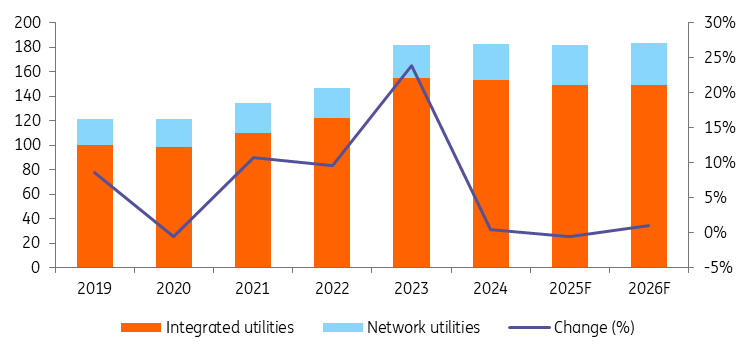

With the top 40 European utilities expected to generate around €186bn of EBITDA in 2026, the sector is projected to achieve 1% year‑on‑year growth. This growth will mostly be driven by pure network utilities, which should see their EBITDA grow by a robust 6%. Gas and electricity grid utilities should continue to benefit from a growing regulated asset base fuelled by ongoing investments to modernise, transform and expand the networks.

Modest cash flow generation growth in 2026

Top 40 European utilities aggregated EBITDA (in €bn)

The modest growth in EBITDA for the sector on aggregate conceals significant disparities within sub-segments as well as players. The most diversified utilities, both from a business and a geographical perspective, will continue to fare the best, benefiting from continued rapid growth in certain parts of the globe.

In Europe, more than 80% of the electricity sales volumes are hedged a year in advance. As a result, the sector’s cash flow generation from power production and marketing activities in 2026 will largely depend on the prices secured in 2025. With renewables representing a larger share, weather conditions to produce hydro, solar and wind power also play a big role in volumes and remuneration. In 2025, the price for the one-year forward contract for France, Germany, Italy, the Netherlands, Spain and the Nordic market averaged €74/MWh. Italy maintains the highest power price with the 1Y forward contract averaging €104/MWh in 2025, while the Nordic market pre-sold electricity at €36/MWh. For 2026, pre‑sold electricity volumes will still be 1.3x to 1.4x higher than the pre-Covid era but around 5% lower than a year ago. Further price decreases should be seen in 2027 with forward contracts locked in during 2026 fully reflecting weaker gas prices. Additional capacity in renewables will also keep pressure on prices.

Call 2: Investments expand but at a slower pace

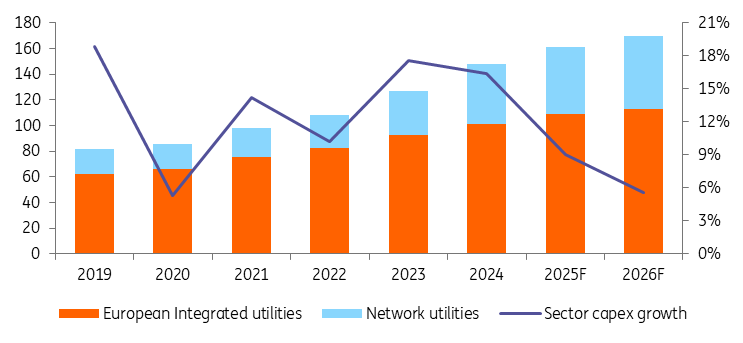

The sector’s investment activity remains robust, but growth is slowing as integrated utilities become more selective in their project pipelines, especially in renewables. The top 40 European utilities will likely invest about €173bn in 2026, a 6% increase compared with 2025.

| +6% |

growth in investments in 2026 |

Investment plans of integrated utilities point to €114bn of spending on infrastructure and projects in 2026, representing 4% growth vs. 2025. Yet disparities exist among European integrated utilities. For instance, EDF SA, Enel SpA, E.ON and EnBW remain committed to strong capital expenditure increases to build renewable projects and infrastructure, in the case of EDF, nuclear power plants. Other utilities such as EDP, Orsted and Naturgy are expected to see investment levels decline slightly or remain broadly unchanged from 2025 due to a more selective project strategy. The rise of material prices and operating costs has eroded margins and utilities are now more inclined to select the projects offering the best returns.

Capital expenditure is still on the rise, although at a lower pace

Top 40 European utilities' capital expenditure (in €bn)

For pure network utilities, the requirement to expand and modernise grids and gas pipelines should result in an additional 12% increase in capital expenditure in 2026, bringing total investment for the top 20 operators to around €59bn. While German and Dutch Transmission (TSOs) and distribution (DSOs) system operators proportionally have the largest investment programmes, several network utilities have announced new increases. French TSO, Réseau des Transport d’ Electricité will increase investments significantly. Between 2025 and 2040, investment needs are now estimated at €100bn. In Italy, Terna announced an ambitious investment programme to accommodate new renewables and interconnections while Snam will invest in renewable gases and new infrastructure. The same is true for Belgian TSOs. In the Nordics, the push for electrification and on/offshore wind integration obliges players such as Fingrid and Statnett to increase capital expenditure as well.

Inflation and the energy crisis in 2021 and 2022 impacted transmission and distribution network utilities, resulting in higher operating costs and materials. Some European regulators have already adapted their regulatory frameworks to allow TSOs and DSOs to recoup these past costs. The sub-sector’s large investment needs have also driven these changes. In the Netherlands, 2026 is the final year of the current regulatory framework, which has seen a change of methodology to take operating costs into consideration. The Dutch regulatory body, the ACM, is now contemplating a cost-plus methodology for the next regulatory period. Germany is also working on the introduction of a cost-plus system, while it has already existed in Belgium for a long period of time. The methodology is now considered as the most appropriate in an environment of long-term investments as it takes into consideration the variation in inflation, operating costs, funding costs and other capital market elements, ensuring utilities remain financially viable.

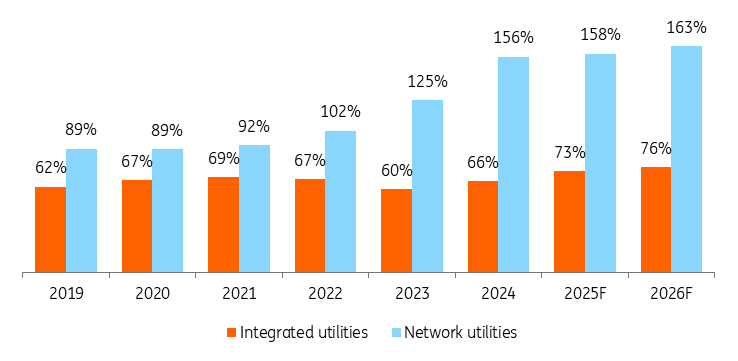

Call 3: Spiralling debt means network utilities have to tackle funding challenges

The elevated level of capex, particularly for network utilities, is a source of concern for companies’ credit metrics and funding capacities. Integrated utilities have benefitted from large cash flow generation thanks to their diversified business model. Grid operators, due to their capped revenues, have seen investment needs reaching levels far above their self-financing capacities since 2022. The situation has kept deteriorating, and we expect network utilities’ capital expenditure to represent 164% of their EBITDA on average in 2026.

For network utilities, cash flow generation is not sufficient to cover investment needs

European integrated and network utilities: evolution of the cap-to-EBITDA ratio over the years

In 2023, utilities issued €68bn in bonds on the EUR market. In 2024, the amount reached €72bn. In 2025, EUR bond issuance decreased to €62bn. Several utilities have looked for alternative funding solutions other than bank loans and bonds. Dutch utilities have already received shareholder loans and TenneT has had a total of €23bn in loans available to finance the capital expenditure. Future TenneT Netherlands’ senior bonds will benefit from the Dutch state's guarantee and allow issuance at lower yields. TenneT Germany will receive c.€9bn from its new shareholders. With the deal between RWE and Apollo asset management, Amprion will benefit from additional funding resources that should reassure credit investors. The Belgian electricity and gas distribution utility Fluvius plans to receive €600m from its shareholders in the first half of 2026.

European regulated network utilities will need to continue looking for external funding to keep credit metrics and ratings at acceptable levels. Access to funds will become a major element in the determination of their credit ratings as signalled by rating agencies’ methodology focus. In 2026, we expect utilities to issue around €70bn in EUR, supported by still growing investments, high bond refinancing needs and more Reverse Yankees. American utilities have also entered a strong investment growth period with capital expenditure growing 10-15% and issuing in the EUR currency allows them to benefit from lower rates in the current market conditions.

All in all, the European utilities sector should not surprise in 2026, with continuing trends such as moderate earnings growth. Elevated investment needs, in particular for the expansion of the infrastructure, will push network utilities to find diversified sources of financing.

* top 40 European utilities - integrated utilities (Acea, A2A, EDF, EDP, EnBW, Enel, Engie, E.ON, Fortum, Hera, Iberdrola, Naturgy, Orsted, RWE, Suez, Vattenfall, Verbund, Statkraft, Veolia, Centrica). Network utilities (Alliander, Elia, Enagas, Enexis, Eurogrid, Fingrid, Fluvius, Italgas, National Grid, Nederlandse Gasunie, Redeia, RTE, Snam, Statnett, Stedin, TenneT, Terna, Amprion, Ren, Redexis)

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Energy Outlook 2026: Abundant supply amid a challenging transition

- This bundle contains 6 Articles