EMEA FX Talking: Politics makes a comeback

- 16 May 2023

- FX Talking

Eastern European FX has been stable over the last month. High yields suggest this region continues to be favoured as a carry play. However, investors will be a little wary on the Polish zloty ahead of elections most likely in October. Further afield, elections are also the focus in Turkey and South Africa's rand has been hit by US accusations of arms shipments

Source: Shutterstock

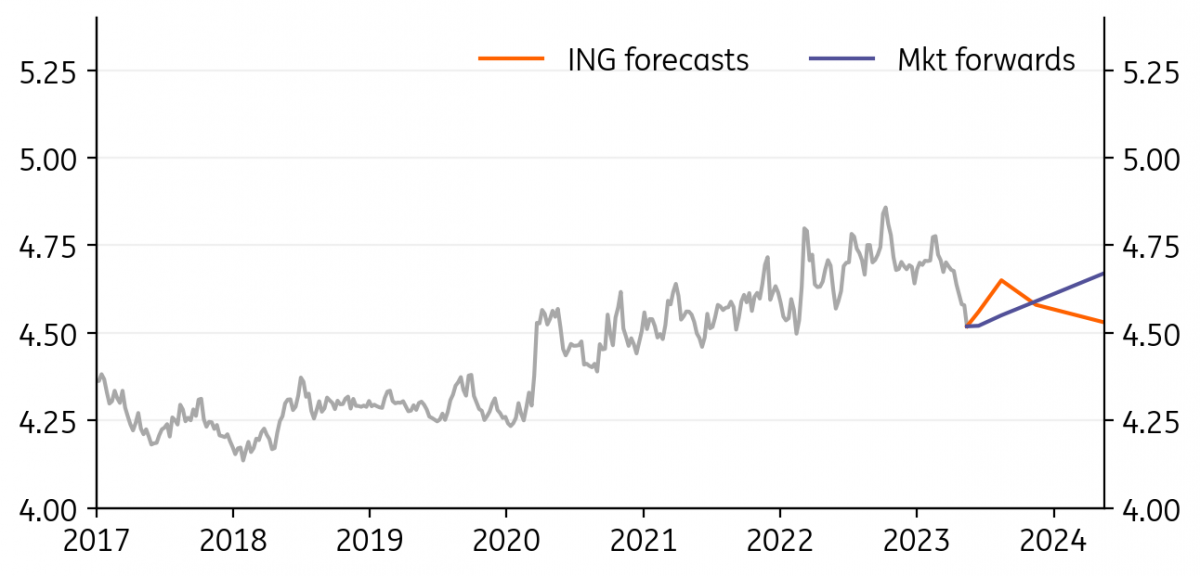

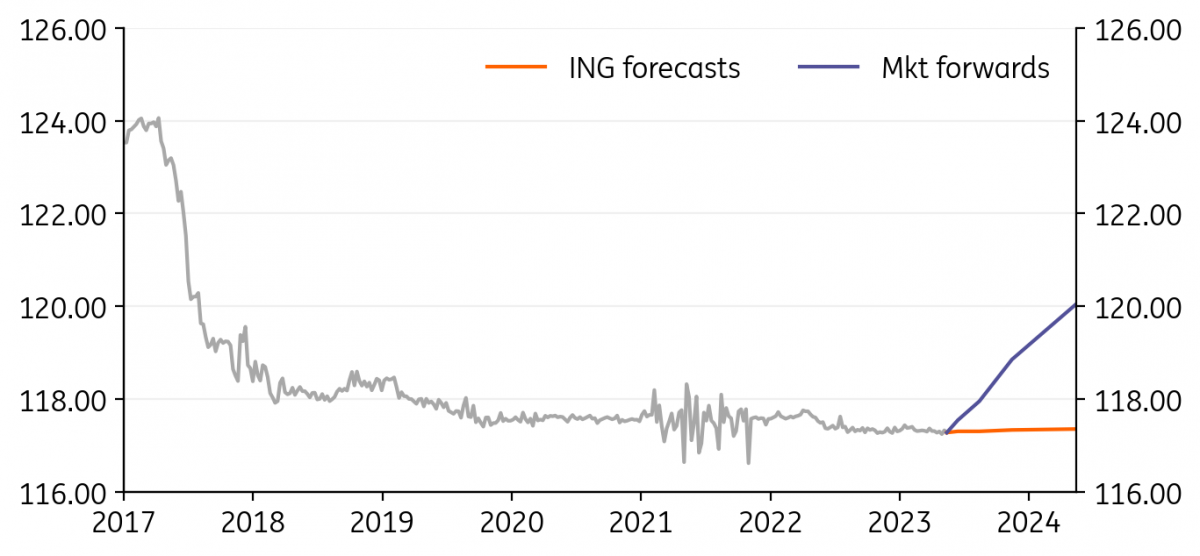

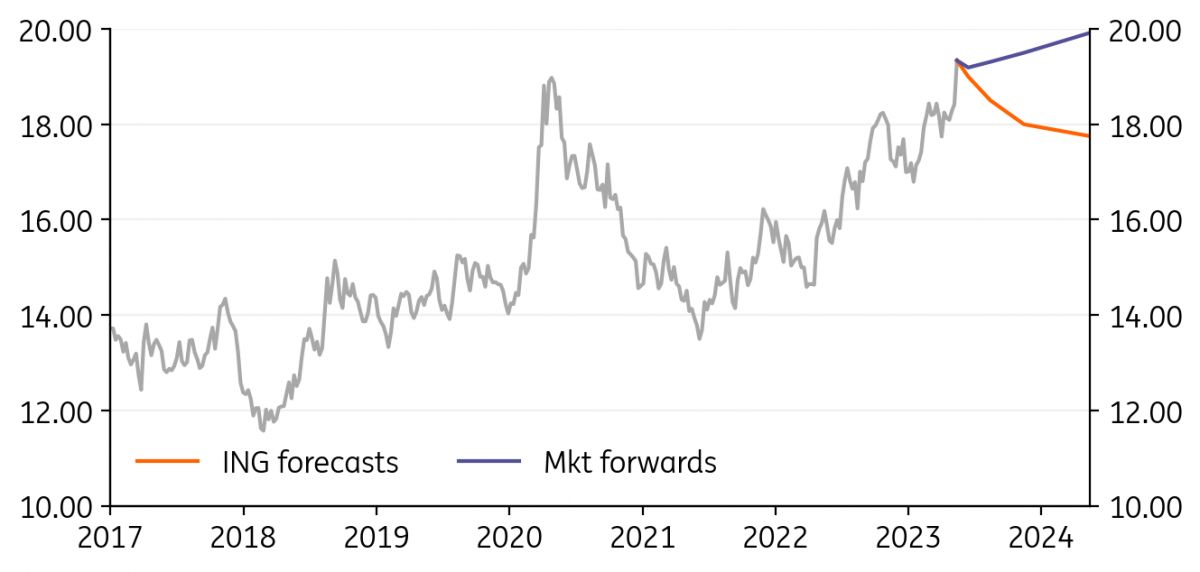

EUR/PLN: Regional sentiment supportive for the zloty

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/PLN

4.5081

|

Mildly Bullish | 4.56 | 4.65 | 4.58 | 4.53 |

- The market has largely shrugged off risks related to the FX mortgage saga, and with the trade surplus, exporters remain strong sellers of the euro. Moreover, as Fed rate cuts approach, the domestic soft-patch and National Bank of Poland easing expectations will play an increasingly less significant role. Given the improving current account and expected weakening of the dollar this prompts us to lower EUR/PLN path for the remainder of the year. Technical analysis suggests that the short term scope for further PLN gains might have been exhausted.

- Domestic political risks ahead of the parliamentary elections in October and potential escalation of the standoff in the Ukraine should prevent EUR/PLN from reaching 4.50 before 2024.

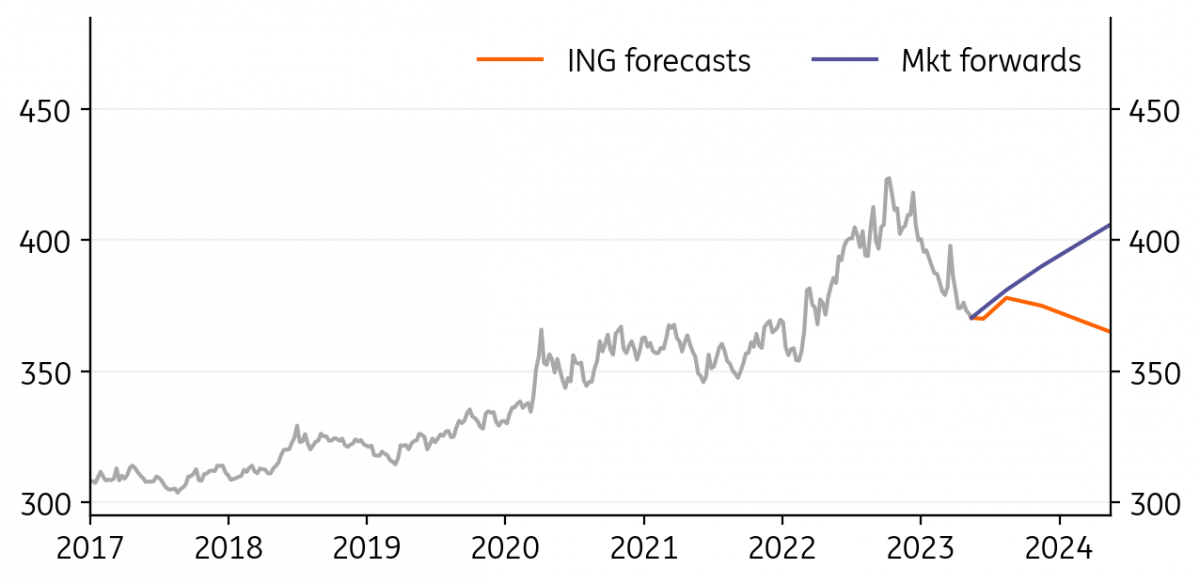

EUR/HUF: Forint can remain strong despite the monetary easing

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/HUF

369.63

|

Neutral | 370.00 | 378.00 | 375.00 | 365.00 |

- At the global level, conditions for the region remain generally positive, with the forint benefiting the most among its CEE peers, along with positive news on the EU (suspended funds) story.

- At the local level, FX carry in Hungary will remain by far the highest in the CEE region. We believe the right conditions persist for the forint to continue to retain market interest.

- Given the National Bank of Hungary’s cautious approach, which sees market pricing as an alignment point in the easing cycle, we remain positive on the forint. Though we see a sideways move in the range of 368 and 378 EUR/HUF depending on the progress in the EU story and the NBH’s boldness in the coming months.

EUR/CZK: Strong Czech koruna reduces the need for more hikes

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/CZK

23.575

|

Mildly Bullish | 23.70 | 24.20 | 24.10 | 24.10 |

- The koruna remains supported amid the CNB board’s hawkish stance, namely due to the increase in votes for a rate hike, from one to three dissenters, at the May monetary policy meeting.

- In our view, the currency is slightly overvalued at current levels and a decline of headline and core inflation below CNB expectations lessens the risk of a hike in interest rates. We expect stability in rates with a view to a possible symbolic rate cut at the August meeting.

- A soft correction of the koruna’s strength and then stability seems likely, on the back of narrowing interest rate differentials against the euro.

EUR/RON: Surplus liquidity pushing carry lower

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/RON

4.9387

|

Neutral | 4.94 | 4.95 | 5.07 | 5.07 |

- The liquidity surplus in the interbank market reached a stunning RON 30.7bn, by far a historical high. Therefore, the money market rates remain anchored to the deposit facility and less to the key rate.

- In this liquidity context, we believe that the National Bank of Romania will be more than willing to offer euro to the market, should any upside pressures on EUR/RON manifest.

- Given the above, the anticipated upward shift in EUR/RON could take a bit longer to materialise, though we still maintain our call for the pair to shift higher between 2.0% and 3.0% by the end of this year.

EUR/RSD: The hiking cycle is likely over

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/RSD

117.30

|

Neutral | 117.30 | 117.30 | 117.33 | 117.35 |

- After raising the policy rate by 500bp over the course of a little over a year, the National Bank of Serbia seems to have ended its hiking cycle as the key rate was kept on hold at 6.00% at the 11 May meeting.

- We believe that future policy decisions will be much more data dependent. The inflation peak is clearly behind us, but our central scenario does not envisage headline inflation back within the NBS’s 1.5%-4.5% target range over the next two years.

- We maintain our expectations for an essentially flat EUR/RSD profile for the rest of 2023, with FX intervention likely to occur sideways in a rather narrow range.

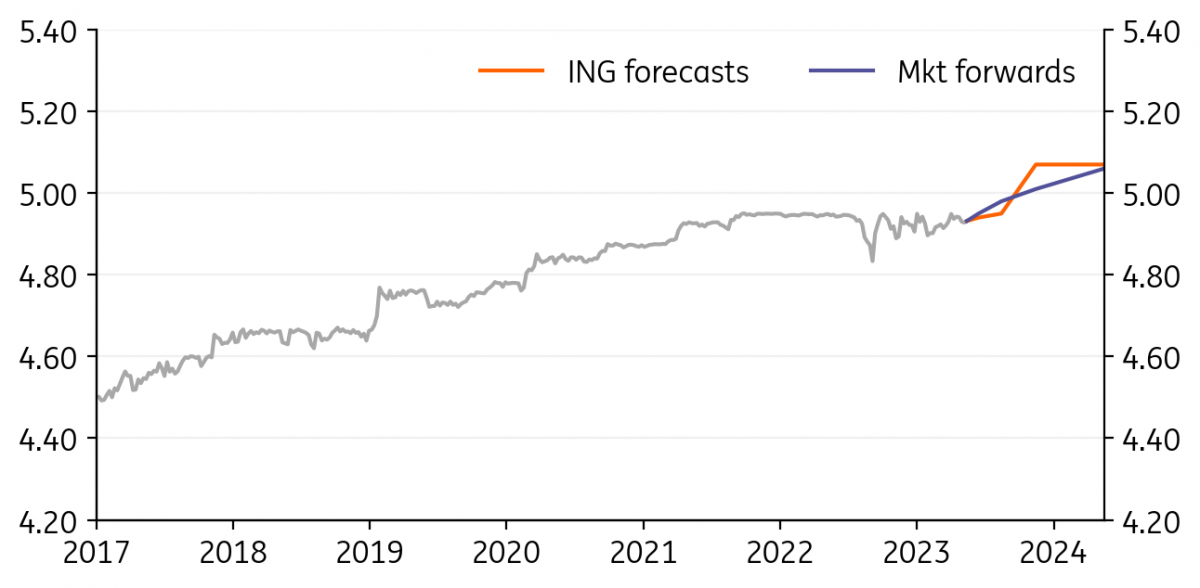

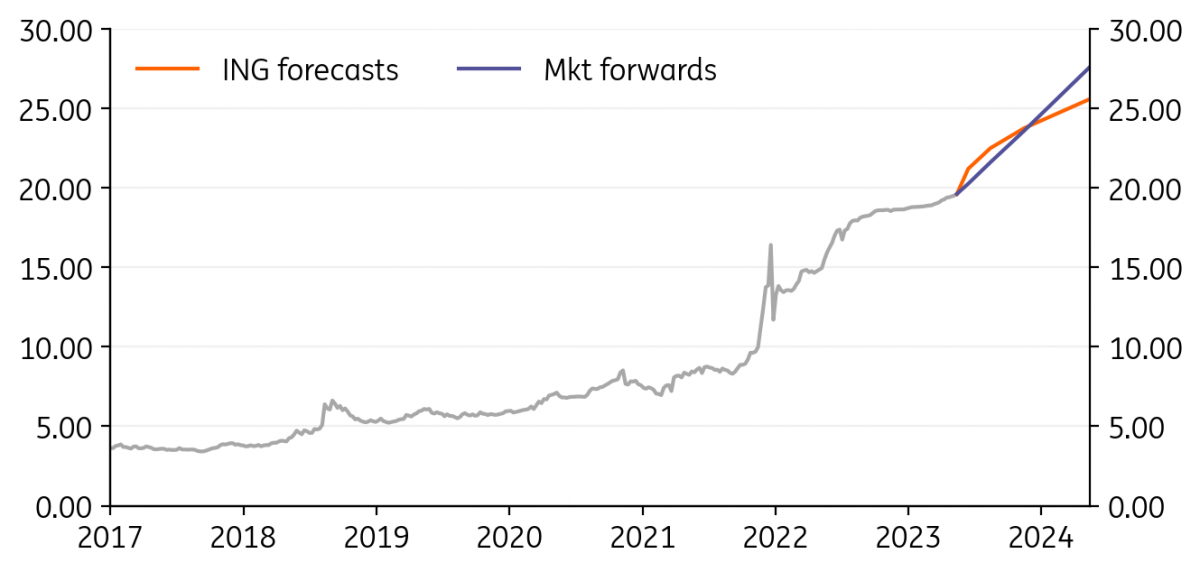

USD/UAH: Short term risks less severe, but longer ones remain high

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/UAH

36.917

|

Mildly Bullish | 37.00 | 39.00 | 39.00 | 37.00 |

- Foreign aid and lower monthly costs of FX intervention (around US$1.5bn in April, down from the monthly peak of US$4bn in June 2022) resulted in Ukraine’s international reserves reaching the highest level in 11 years (US$35.9bn). This significantly lowers the risk of any prompt hryvnia devaluation.

- There is still no end to Russia’s war in sight and the economic toll has been increasing. Ukraine’s current account also remains in deficit. Therefore, we still anticipate the Ukrainian currency to weaken in the coming months as a measure to bolster competitiveness.

USD/KZT: Export flows seem supportive for now

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/KZT

451.05

|

Mildly Bearish | 450.00 | 457.00 | 463.00 | 470.00 |

- USD/KZT traded in a narrow 445-455 range in April, approaching our near-term target of 440 in the beginning of May, despite the recent weakness in oil prices, possibly reflecting higher exports via non-Russian trade routes.

- At current levels, the tenge is again close to the peak levels seen earlier this year and in early 2022.Further appreciation from those levels is not out of the question but would require more positive surprises on exports and capital flows.

- Thanks to the recent downgrade of ING’s house view on USD, we can slightly strengthen our KZT forecast profile. However, Kazakhstan is still exposed to geopolitical risks due to its close trade relations with Russia.

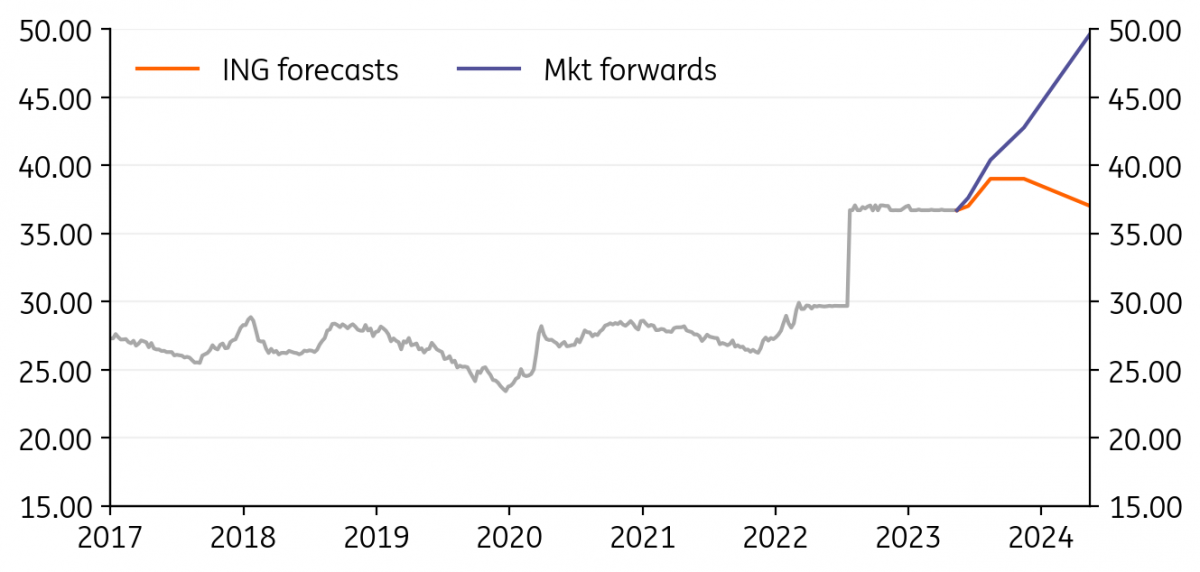

USD/TRY: Focus now on elections

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/TRY

19.661

|

Mildly Bullish | 21.20 | 22.50 | 23.75 | 25.60 |

- At the April MPC, the Central Bank of Turkey reiterated its “Liraization” strategy. It concluded that the current stance was adequate in terms of supporting the necessary recovery after the earthquakes and maintaining price and financial stability.

- The key challenge for the CBT currently is to maintain currency stability in the near term. In April, it asked banks to limit the amount of dollar purchases they make in the interbank market to ease pressure on the lira. Following the move, banks began widening spreads between their bid & ask prices for foreign currencies, while volatility has increased to some extent.

- Given elevated inflation and ongoing upside risks, the real value of the exchange rate will remain in focus – as will elections.

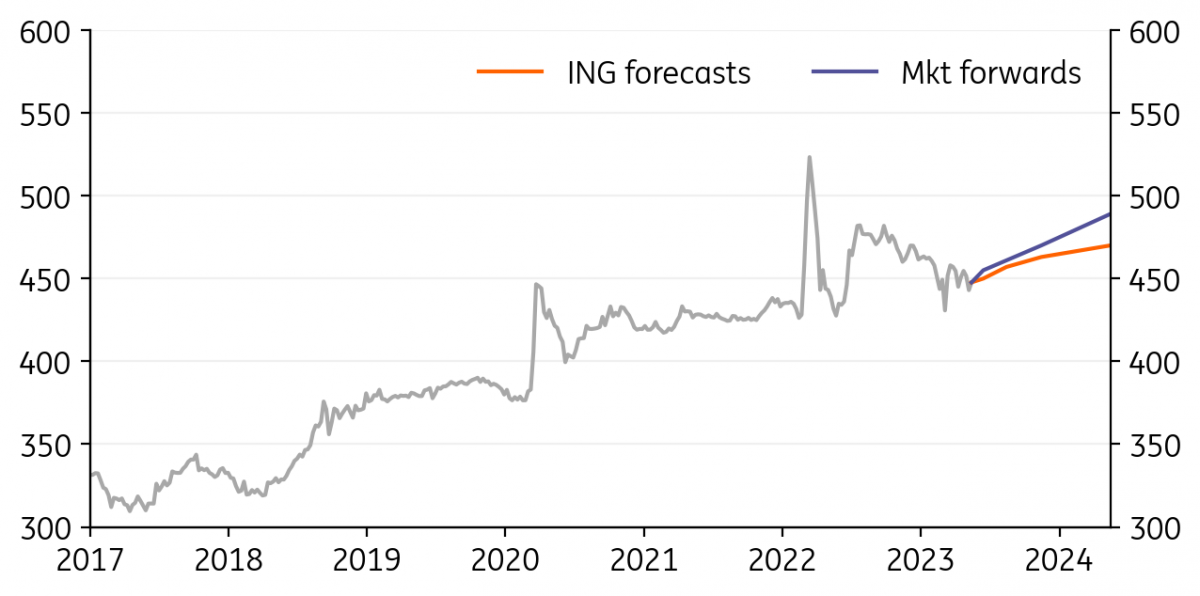

USD/ZAR: Taking sides

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/ZAR

19.117

|

Neutral | 19.00 | 18.50 | 18.00 | 17.75 |

- The war in Ukraine forced investors to re-assess geopolitical power blocs and examine what being a member of the BRICS meant in practise. China’s position on Russia has been reasonably clear, but Brazil, India and South Africa have emphasised neutrality. The bombshell allegation by the US Ambassador in early May is that South Africa supplied military aid to Russia last December.

- The rand took the above news very poorly – and questions whether US Congress will re-examine South Africa’s eligibility for duty free access to US markets under the African Growth and Opportunity Act. Sanctions risk is just adding to ZAR malaise.

- Weak growth, a widening current account deficit and now the threat of pariah status can keep the ZAR soft this summer.

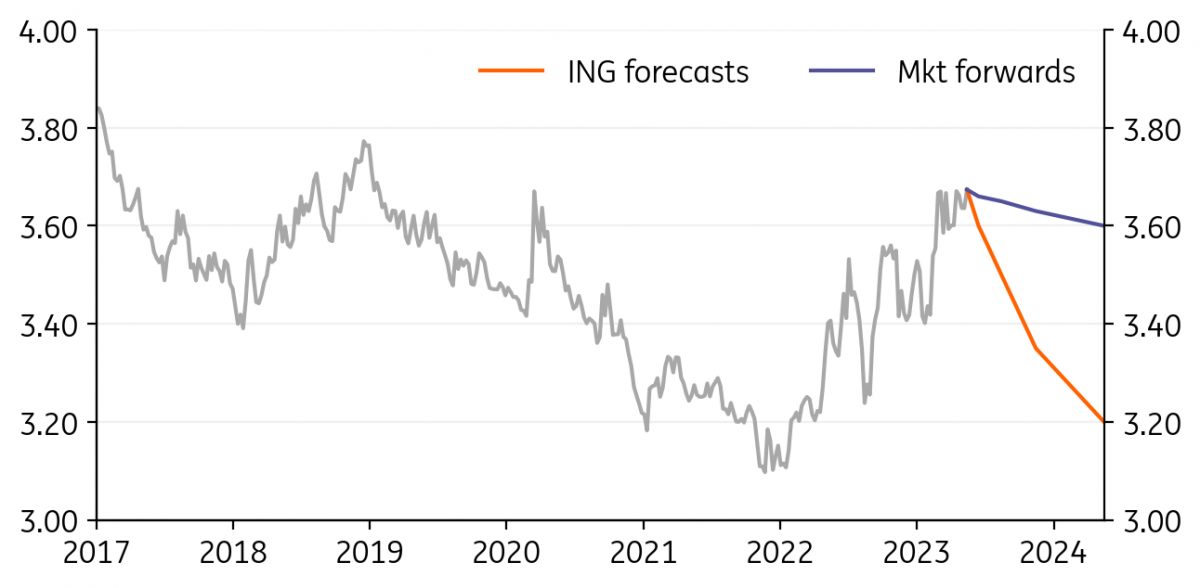

USD/ILS: Few signs of ILS recovery

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/ILS

3.6594

|

Mildly Bearish | 3.60 | 3.50 | 3.35 | 3.20 |

- USD/ILS continues to press the highs near 3.70. There are no concrete signs as yet that the Bank of Israel has been intervening to sell FX (intervention normally shows up in FX reserve releases). That may be because the political situation is so tense.

- There are no signs that the government is ready to soften its stance on its controversial reforms. But equally the government could fall if it fails to pass a budget by 29 May.

- Our bearish long-term view on USD/ILS is premised on the Fed being able to cut rates and a broad dollar bear trend winning through. However, sticky US inflation and steady Fed rates would leave USD/ILS open to a temporary spike to 3.80.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Bundle

15 May 2023

FX Talking: The rocky path to a weaker dollar

- This bundle contains 5 Articles

tba