EMEA FX Talking: Weakness looks to be contained

- 16 March

- FX Talking

The EMEA region has been one of the hardest hit on the back of the energy shock, with both currencies and short-dated interest rate markets taking the strain. However, we are not looking for any significant hiking cycles in the region, and we believe central banks have local exchange rates under control. Hungary's election next month is a major market mover

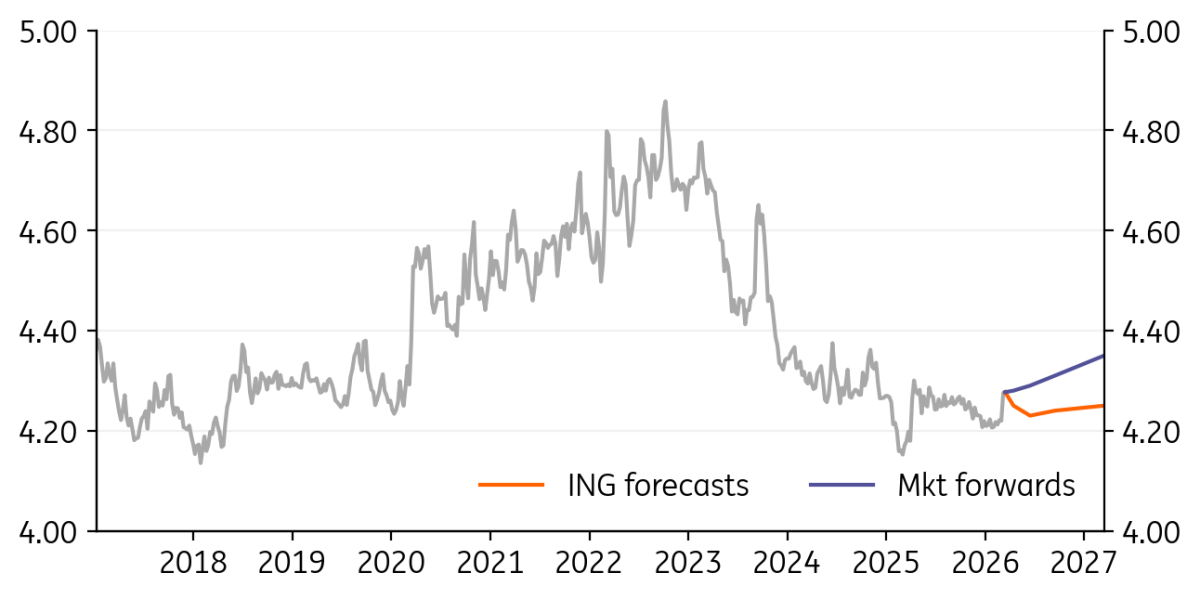

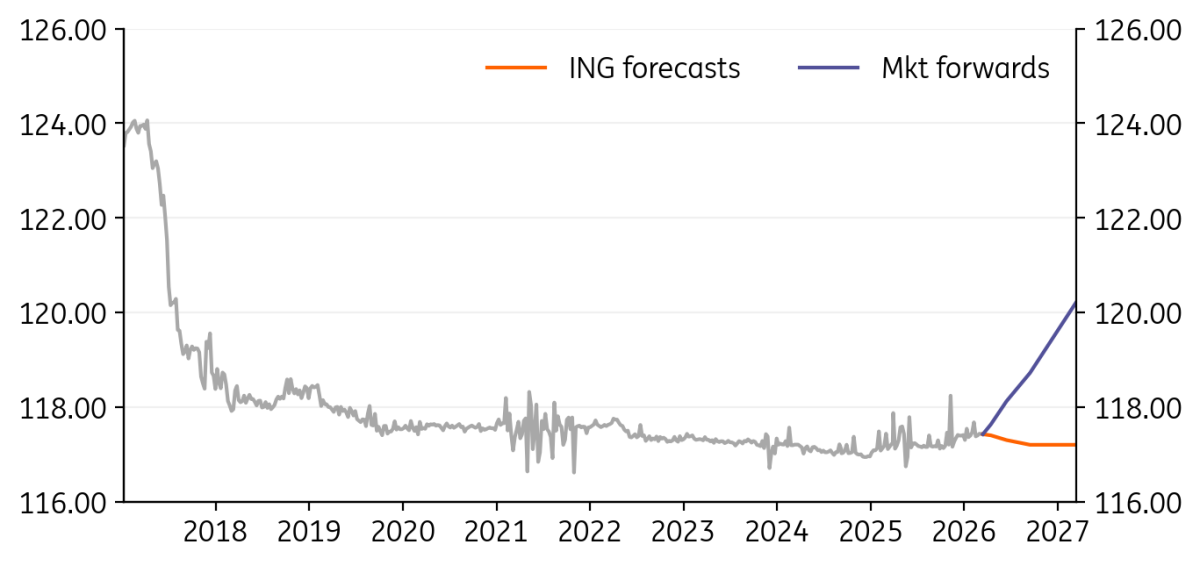

EUR/PLN: Zloty hit by Middle East conflict

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/PLN

4.2682

|

Mildly Bearish | 4.25 | 4.23 | 4.24 | 4.25 |

- As the conflict in the Middle East triggered a risk off sentiment, EUR/PLN touched 4.30, the highest level since April 2025 and the beginning of the trade war saga. The zloty also came under selling pressure due to domestic factors, as the Monetary Policy Council decided to cut interest rates in March.

- Moreover, the PLN was hit by a controversial central bank proposal to generate profit through a change in accounting rules or a (temporary) sale of part of its gold reserves – a move which, in the view of the National Bank of Poland, could substitute the European SAFE programme.

- Current risks to the zloty remain linked to geopolitical factors – less to potential Russian military provocations in Europe and more to developments in the Middle East. However, macroeconomic fundamentals continue to support the currency, as GDP growth is expected to outperform the CEE region, while inflows of EU funds should further brighten the outlook for this year and beyond.

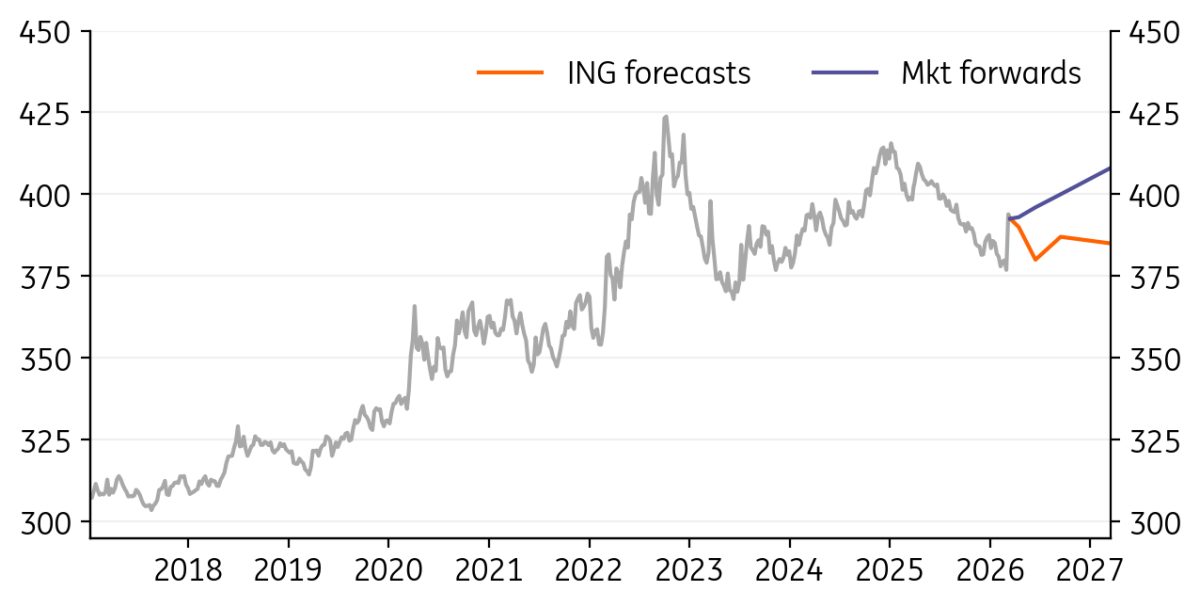

EUR/HUF: We foresee continued high volatility in HUF

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/HUF

391.66

|

Mildly Bearish | 390.00 | 380.00 | 387.00 | 385.00 |

- We are now in a 'pick your poison' situation with regard to the forint. The war in the Middle East and the energy price shock are hitting Hungary hard due to its reliance on energy imports. Even if the market calms down slightly, there is another red flag event: the general election on 12 April, which is set to be a close race.

- We think that monetary policy will be sidelined in the coming weeks, with either the energy situation or politics deciding the fate of the HUF. With the central bank being as cautious as possible, and even actively using its FX reserves to redirect import-related FX market flows, if necessary, the 385-390 range will act as a gravity line.

- On the political front, we predict that investors will react asymmetrically, as long positions related to political bets have largely been liquidated. We believe that there will be less resistance to a stronger HUF. In either case (a result-driven rally or a sell-off), however, the move will be short-lived, with the fundamentals dragging EUR/HUF back to around 385 as the dust settles on the election results.

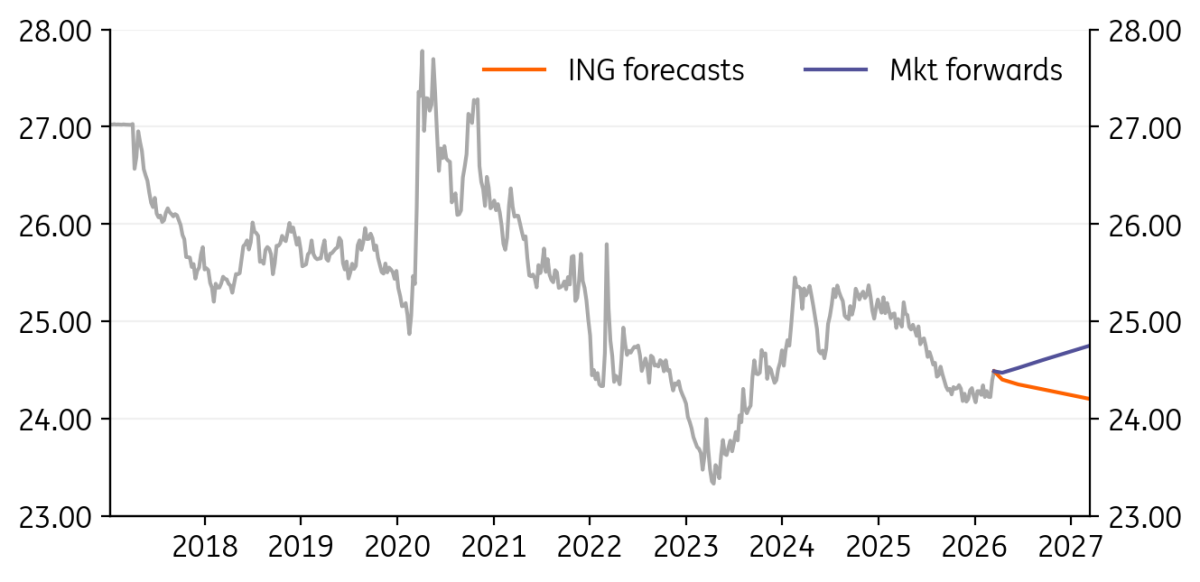

EUR/CZK: Subdued inflation, plausible growth structure, and sound fiscal back koruna

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/CZK

24.44

|

Mildly Bearish | 24.40 | 24.35 | 24.30 | 24.20 |

- The Czech economy is well positioned to face the current turmoil given that inflation is muted, economic growth has a plausible structure, and the fiscal setup is reasonable. Under conditions of an oil price shock, and more generally a negative external supply shock, the Czech National Bank will follow the appropriate recipe, which is to keep rates unchanged.

- The thing is that two almost simultaneous risks are at hand: higher inflation on the back of ample energy prices, along with a pressured economic performance due to tighter budgets, disrupted supply chains, and shaken confidence.

- And yes, elevated oil prices will mostly affect Asia and Europe, with limited options to substitute energy flowing from the Gulf. That said, the koruna has still decent macroeconomic backing and will outperform the single currency once the onset of the shock starts drifting to the past. Meanwhile, we see rather stable rate against the greenback, which is backed by domestic energy production and export.

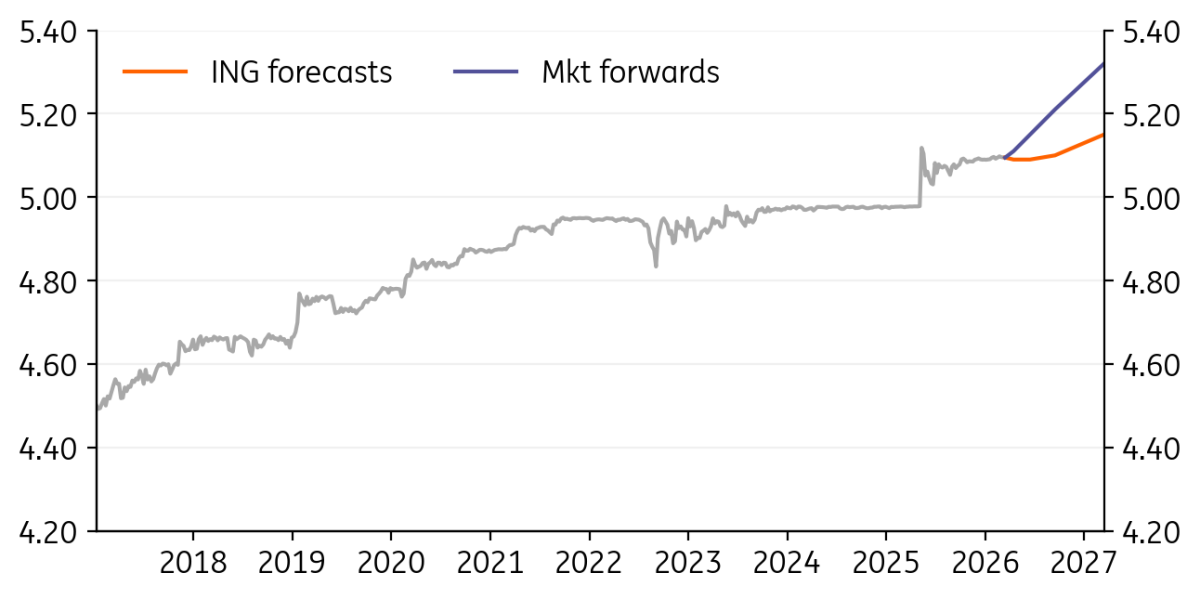

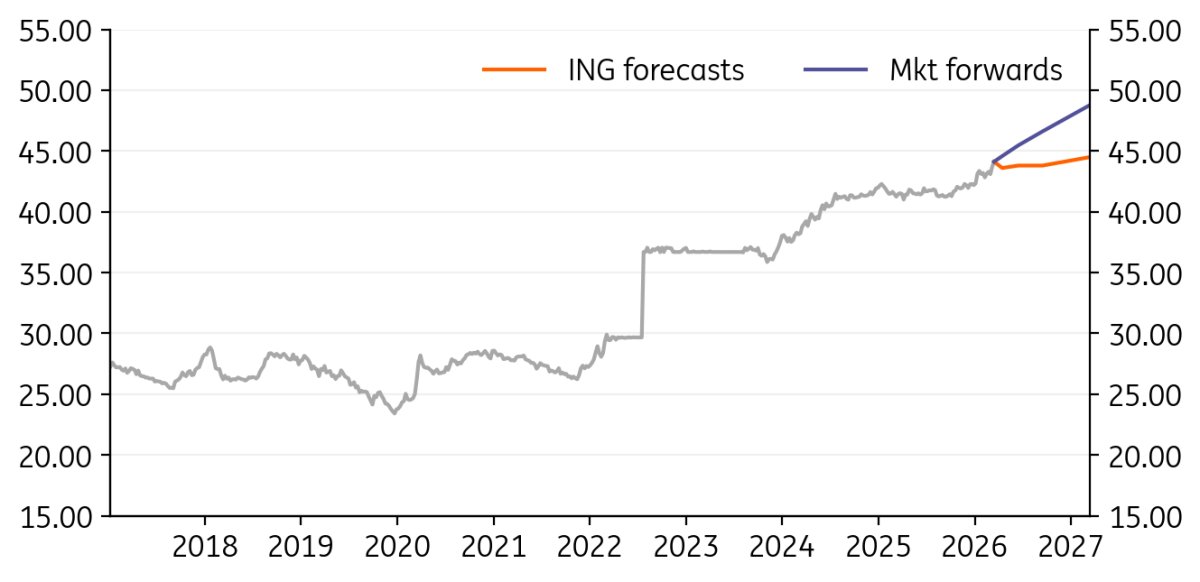

EUR/RON: The NBR continues to hold a firm grip on the currency

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/RON

5.0951

|

Neutral | 5.09 | 5.09 | 5.10 | 5.15 |

- The EUR/RON has traded largely sideways through early March, but sizeable trading volumes – suggestive of official offers – have likely prevented EUR/RON from rising in line with regional peers amid the global risk-off environment. If risk aversion persists, an earlier-than-expected upward adjustment of the pair cannot be ruled out.

- Inflation is now set to exceed 10% in the March–April prints, driven largely by the spike in oil prices, leaving the National Bank of Romania with little room for manoeuvre. At the same time, if global risk‑off sentiment persists for a prolonged period, maintaining the FX rate at current levels could become increasingly costly. Yet allowing a leu depreciation would only feed back into inflation pressures, further complicating the policy trade-off.

- In money markets, the rise in FX implied volatility signalled a rapid tightening of the RON liquidity surplus (RON45bn in February), although the magnitude was still modest compared with the May 2025 episode. Government bond yields reacted more forcefully initially but have since partially retraced. Our base case now assumes a first rate cut in August and cumulative easing of 75bp in 2026.

EUR/RSD: NBS likely to resist upward RSD pressures ahead

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/RSD

117.42

|

Mildly Bearish | 117.40 | 117.30 | 117.20 | 117.20 |

- EUR/RSD has remained largely insulated from the recent global sell-off, likely reflecting continued official FX interventions. The pair traded mostly within a narrow 117.30–117.45 range.

- Serbia’s macroeconomic fundamentals remain supportive, underpinned by strong investment inflows and reflected in the country’s Ba2 sovereign rating. Inflation has moderated well within the target range, standing at 2.4% in early 2026. That said, Moody’s decision in early March to revise the outlook from positive to stable serves as a reminder that recent progress is not guaranteed and remains vulnerable to shifting risks.

- At its March meeting, the National Bank of Serbia left the policy rate unchanged at 5.75%, with heightened geopolitical risks featuring prominently in its assessment. FX stability is expected to remain a key priority; between January 2026 and February 2026, the NBS sold EUR810m to support the dinar, with intervention volumes likely to increase further in March.

USD/UAH: UAH remains under selling pressure

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/UAH

44.09

|

Mildly Bearish | 43.60 | 43.80 | 43.80 | 44.50 |

- The war in the Middle East and rising global energy prices have increased pressure on the Ukrainian hryvnia. At the beginning of March, the hryvnia began to weaken to record lows against both the US dollar and the euro. Even without the global risk off sentiment, the currency continues to face pressure due to ongoing war-related disruptions.

- From a macroeconomic perspective, the situation in Ukraine remains mixed. On the one hand, business sentiment weakened slightly in February due to uncertainty over the duration of hostilities and large-scale destruction. On the other hand, several factors have provided positive momentum for economic activity: sustained consumer demand, stable inflows of international aid, and slowing inflation.

- Although international reserves fell slightly in February – driven by the National Bank of Ukraine’s FX interventions and Ukraine’s foreign currency debt repayments – they remain close to their highest level since the country’s independence and are sufficient to maintain FX market stability.

USD/KZT: Lifted by oil

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/KZT

484.94

|

Mildly Bearish | 480.00 | 500.00 | 520.00 | 530.00 |

- After a flat February, the tenge appreciated by c. 2% to the US dollar in the first two weeks of March, as the war in the Middle East lifted oil prices by 42%. Strengthening in the tenge was somewhat restrained by the global flight to safety that led to the dollar’s c. 3% appreciation to key currencies.

- The National Bank of Kazakhstan, in line with earlier commitments, opted to hold the policy rate at 18.00% despite CPI decelerating to 11.7% in February. This move should reinforce the capital account amid rising external risks related to higher imported inflation and a reduction in risk appetite.

- We remain constructive on KZT in the near term, as commodity exporters of the CIS region are beneficiaries of the renewed tensions in the Middle East, but the longer-term effect will depend on the duration and may be muted by counterbalancing outflows on the capital and current account.

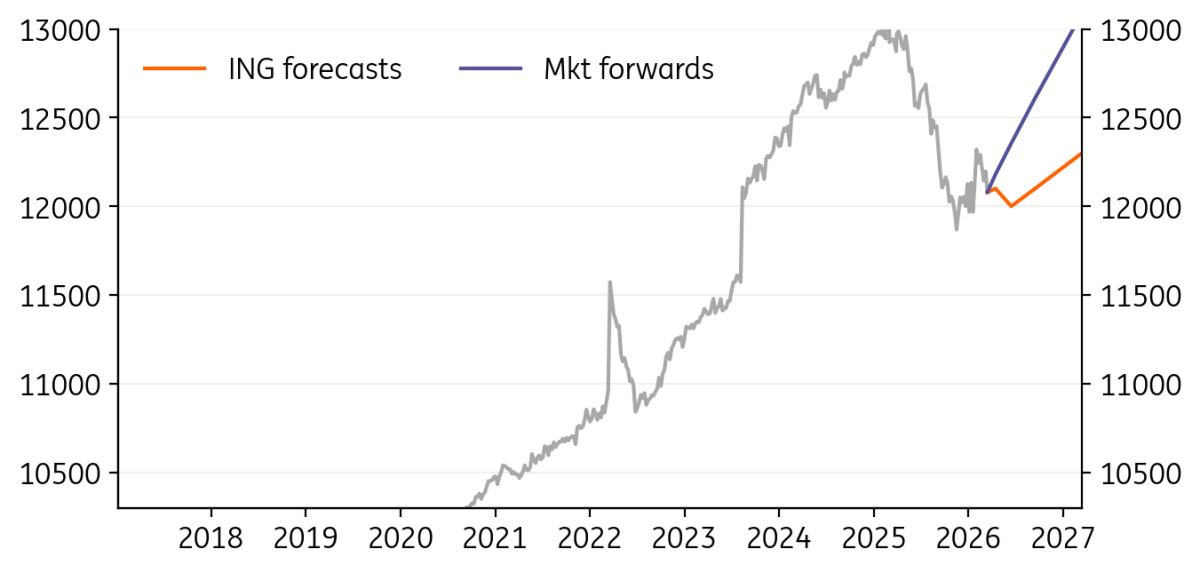

USD/UZS: Yet to catch up with gold

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

12100.00

|

Neutral | 12100.00 | 12000.00 | 12100.00 | 12300.00 |

- The Uzbekistani soum posted a 0.6% appreciation to the US dollar in the first two weeks of March after similar appreciation for the full month of February. It was a benefactor of the 12-day war of June 2025, however, this time gold prices didn’t react to the rise in global uncertainty and dropped 5% after rallying 21% in January-February.

- We believe the soum is still undervalued relative to the gold price level, as the central bank has been holding back physical gold sales, exporting only 85 mt of gold in 2025 vs c. 100 mt annual capacity.

- We believe Uzbekistan is best positioned in the CIS space from the macro standpoint given its exposure to gold and distance from Iran. However, it remains to be seen to what extent this will pass through to the UZS performance given the country’s persistent twin deficits and elevated CPI risks.

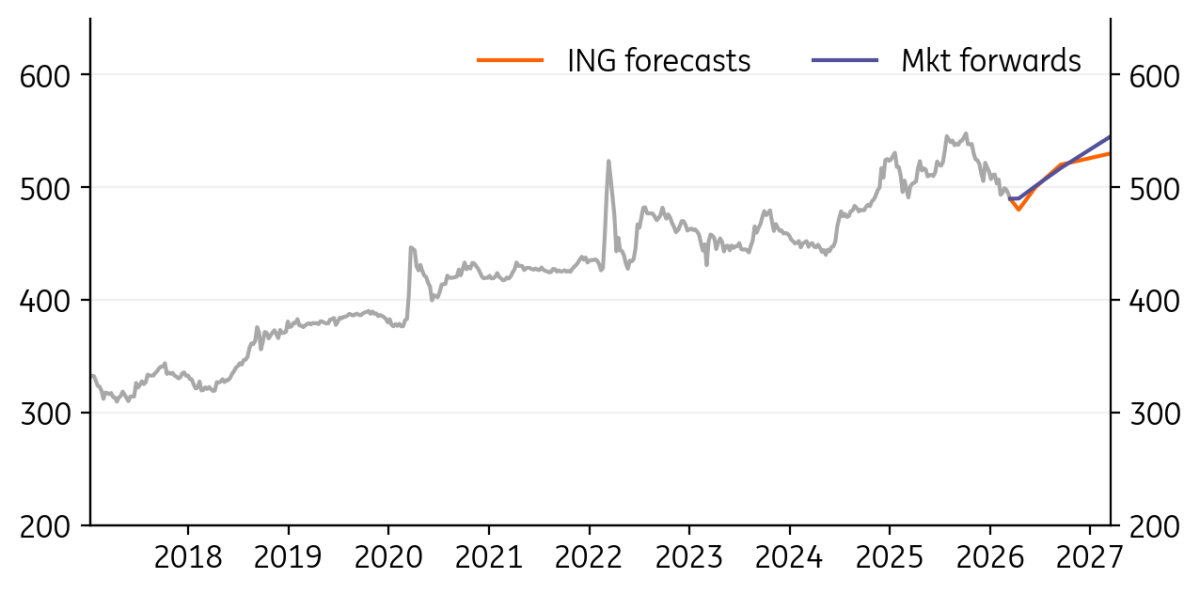

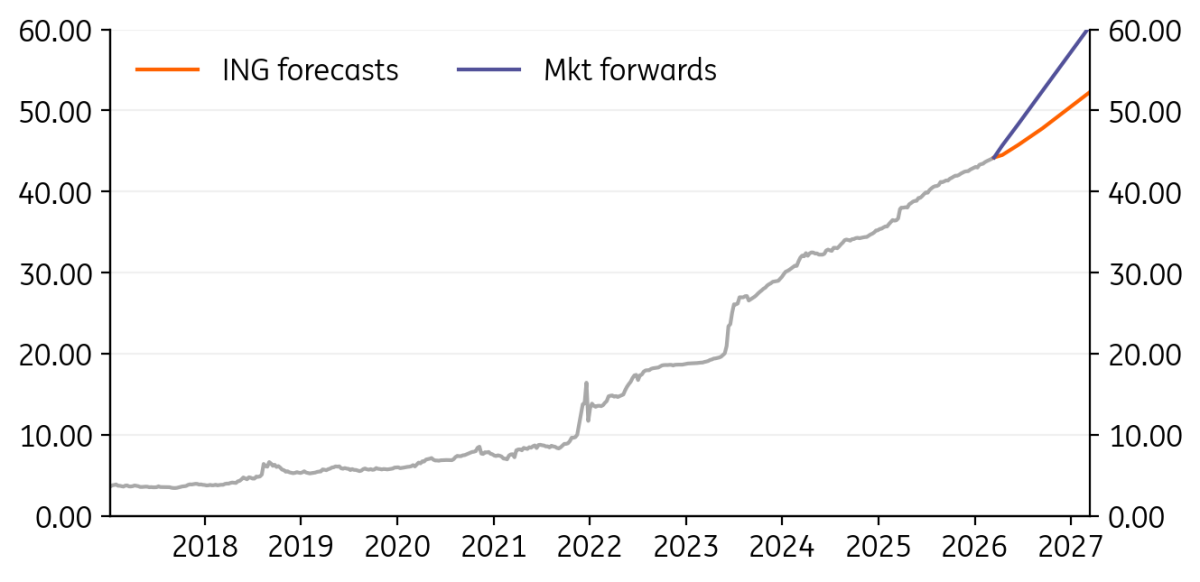

USD/TRY: Geopolitical shock to weigh on the macro outlook

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/TRY

44.19

|

Mildly Bullish | 44.50 | 45.75 | 47.80 | 52.30 |

- The geopolitical shock from the Middle East conflict has increased near-term risks to the macro outlook with effects on the risk premium, inflation, monetary policy and the current account balance. The economic impact of these developments will depend on both the scale and duration of the disruption.

- As geopolitical uncertainty continues, Turkish policymakers have moved quickly and in a coordinated manner to stabilise markets by a) providing FX supply to the system, b) reducing TRY supply that could go to FX, c) supporting demand for the lira and d) increasing the size of daily securities purchases. The Central Bank of Turkey did not change the 37% policy rate in March. However, continuing reserve losses may lead the bank to raise the policy rate and maintain flexibility to tighten further, if needed.

- In addition to the CBT, the Ministry of Finance has also taken action to absorb the impact of oil prices. It introduced a tax regulation which essential means that if refinery prices go up because of higher global oil prices or a weaker exchange rate, the government can cut the special consumption tax on these products by up to 75% of that increase.

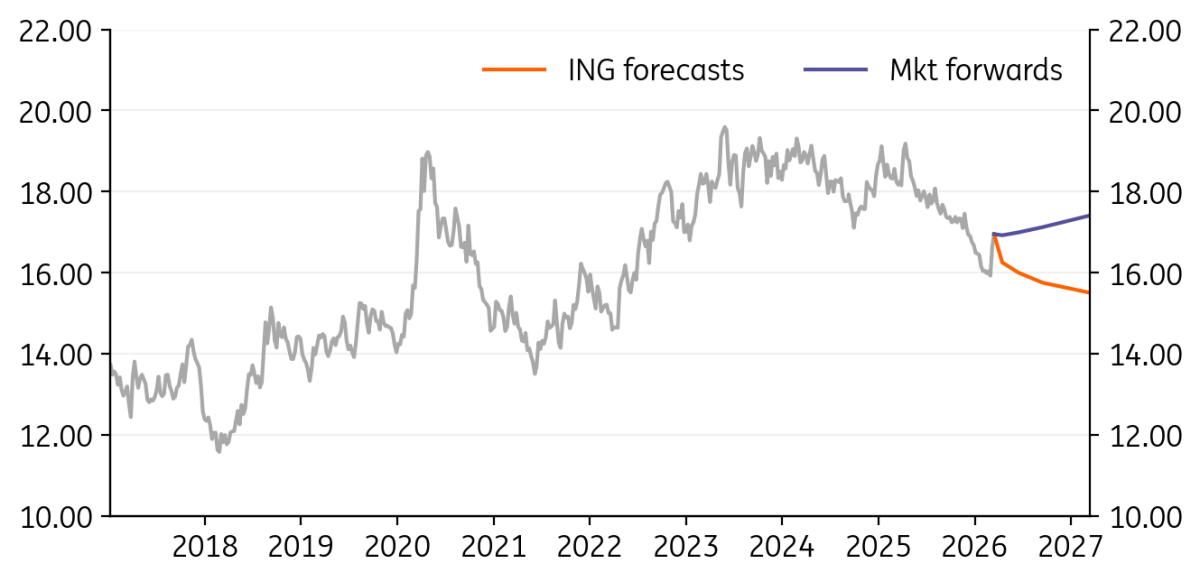

USD/ZAR: Energy crisis curtails the SARB easing cycle

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/ZAR

16.88

|

Bearish | 16.25 | 16.00 | 15.75 | 15.50 |

- Before the Middle East crisis, South African markets had been enjoying goldilocks conditions of low inflation, the prospect of rate cuts, bond inflows and a stronger rand. The oil shock has reversed all that, curtailing expectations of any further cuts from the South African Reserve Bank and prompting foreigners to sell $2bn of South African bonds in the first week of the crisis.

- As for all markets, the duration of the shock will be key, and the market is now starting to price a 25bp SARB rate hike. That will come sooner if USD/ZAR trades to 17.50

- Back in 2022, USD/ZAR rose 25% on the energy shock. Today, the SARB’s new, lower inflation target at 3% suggests the central bank will act sooner to tighten if energy prices don’t turn around soon.

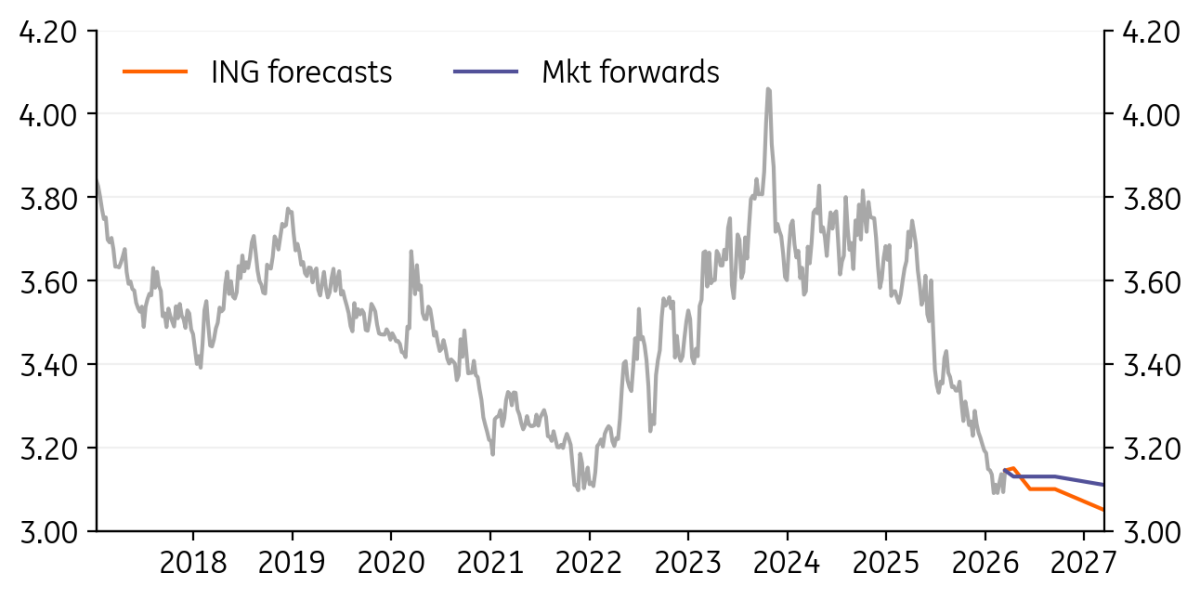

USD/ILS: Shekel remains resilient

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/ILS

3.1367

|

Neutral | 3.15 | 3.10 | 3.10 | 3.05 |

- Somewhat surprisingly, the Israeli shekel remains incredibly well bid during this third Gulf War. It is hard to know the driving factors, but presumably portfolio and perhaps some US defence flows are going through the FX market. It is not as though Israel benefits from an energy crisis and indeed Israel’s terms of trade have declined as oil and gas prices have spiked.

- Unlike elsewhere in the world, Israel monetary policy rates have been re-priced 25-45bp lower across the curve. This is presumably based on the view that the shekel stays strong and that Israel has been warned off FX intervention by Washington.

- We suspect Israel will want to keep USD/ILS above 3.00 for the export sector and will cut rates if need be.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Bundle

16 March

FX Talking: Same shock, new drill

- This bundle contains 6 Articles