EMEA FX Talking: Consolidating after a strong 2025 performance

- 8 December 2025

- FX Talking

It's been a good year for EMEA FX, taking advantage of the softer dollar and in some cases being driven by encouraging domestic demand stories. We do see scope for some further modest gains in the Hungarian forint, but the more solid, macro-driven gains should be found in the Czech koruna. And we expect high yielders to continue outperforming their forwards

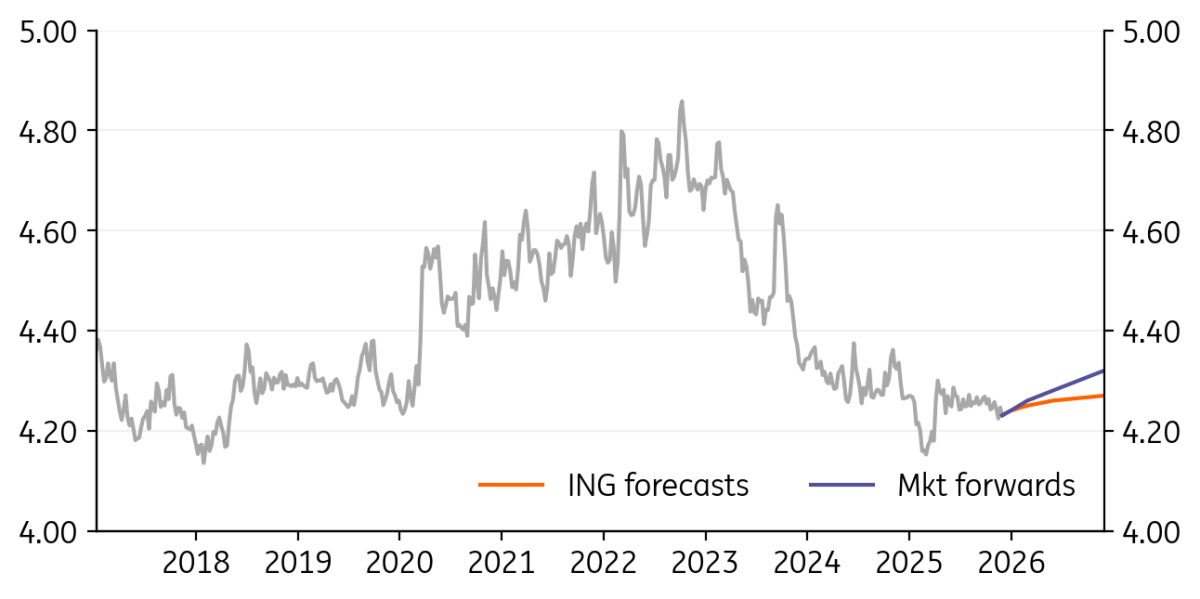

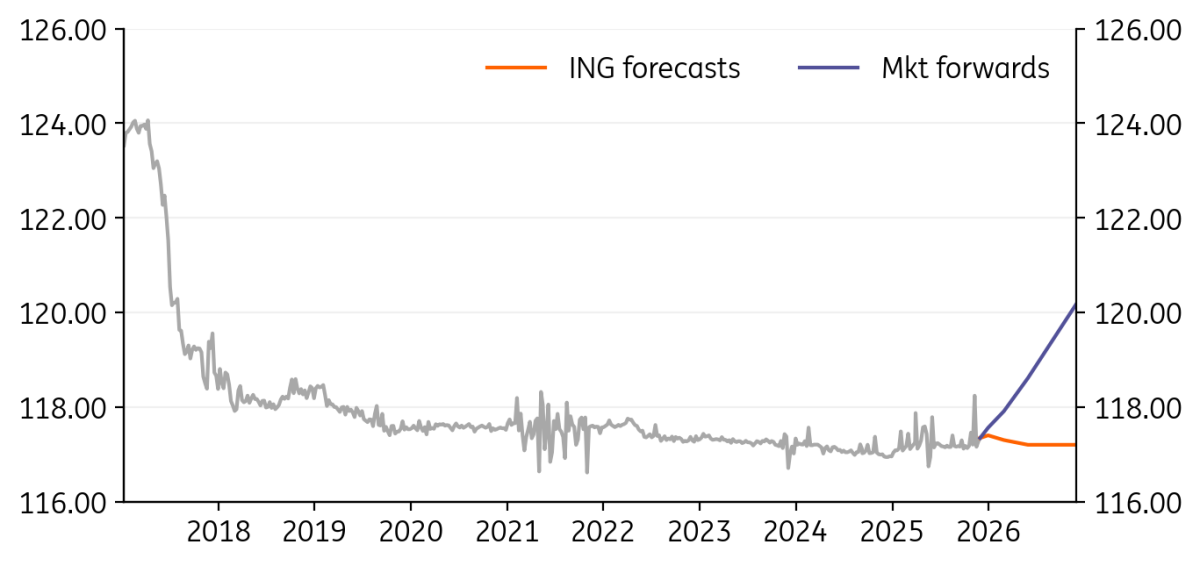

EUR/PLN: Zloty stabilises despite more dovish central bank

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/PLN

4.23

|

Neutral | 4.24 | 4.25 | 4.26 | 4.27 |

- The EUR/PLN exchange rate is moving in a tight range of 4.20 -4.25 supported by the stabilisation of the EUR/USD and a lack of data from the US economy due to the government shutdown. Signs of a possible peace agreement between Russia and Ukraine have also helped to reduce volatility in the Polish currency.

- We maintain a neutral outlook for the zloty. Solid macroeconomic fundamentals and flows of European Union funds should shield the currency from significant depreciation, while the external environment remains supportive for EM FX given the expected weakening of the US dollar. This depreciation should offset the central bank’s possible dovish stance in 2026.

- Current risks to the zloty are linked to geopolitical factors. The ongoing trade war and a delay in fiscal stimulus threatens the expected recovery of the German economy, while an escalation of the conflict in Ukraine or a Russian hybrid war in the EU or Poland could act as headwinds for the zloty.

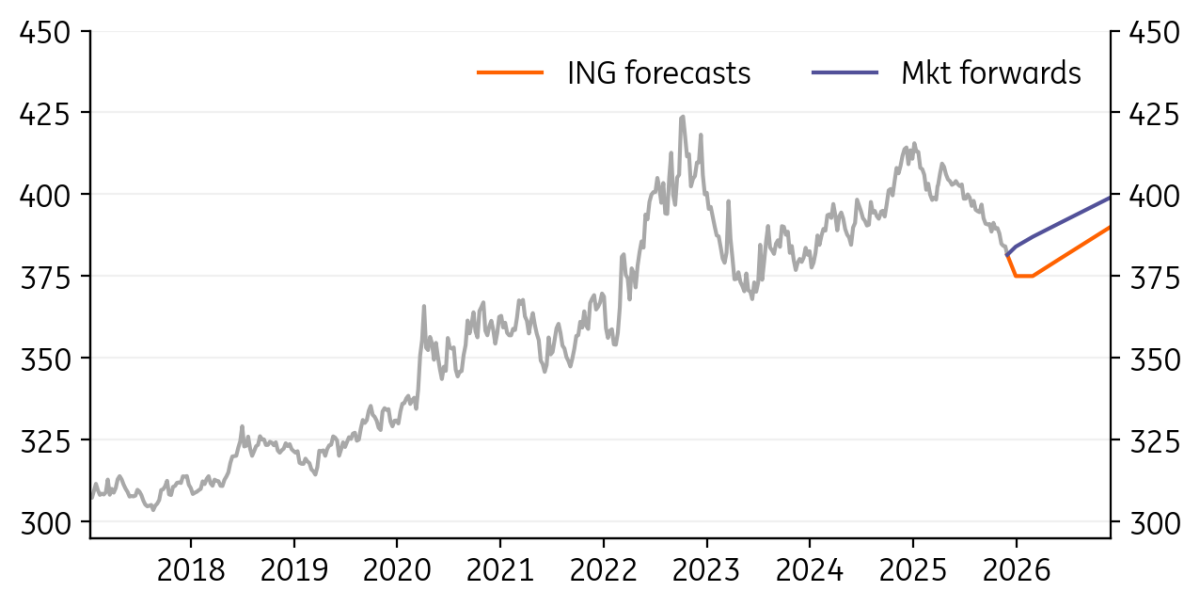

EUR/HUF: Next quarter brings two-way risk for the forint

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/HUF

381.71

|

Mildly Bearish | 375.00 | 375.00 | 380.00 | 390.00 |

- The EUR/HUF has continued its run, reaching a low of 380 - a level not seen since the end of 2023. Therefore, there is no end in sight to the HUF carry trade, at least not in the short term.

- We think the forint will reach the 370–375 range by the end of this year and into next, particularly if tangible progress is made in the Russia–Ukraine ceasefire/peace negotiations.

- The FX outlook is becoming murkier as the 2026 general election in spring approaches. Moreover, the looming EU SAFE loan decision in 1Q26 is creating a two-way risk, and we think the market will err on the side of caution, taking some profits, and pushing EUR/HUF back up to around 380-385 in six months' time.

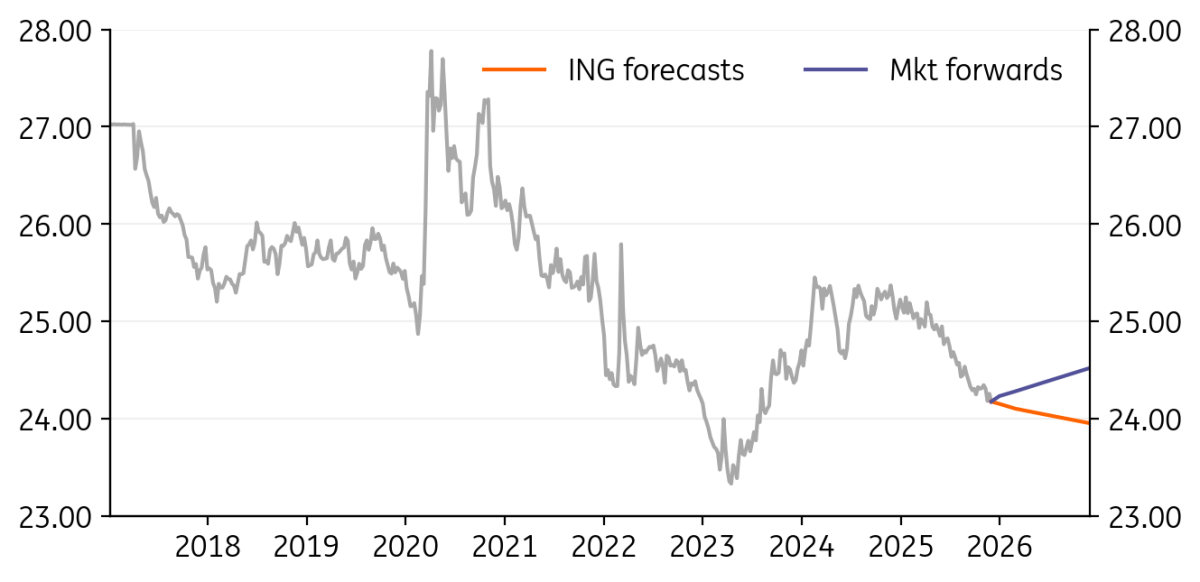

EUR/CZK: Strong economy, sound fiscal stance support the koruna

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/CZK

24.17

|

Neutral | 24.15 | 24.10 | 24.05 | 23.95 |

- The Czech economy is set to continue its solid rebound, outperforming the eurozone. The Czech National Bank will likely hold rates steady at 3.5% for quite some time, while headline inflation is set to hover close to target over the next year. Such a combination makes the real interest rate average of 1.4% over the next year a solid foundation for the koruna. Even more so, as the eurozone’s real interest rate will likely be substantially lower.

- Both growth outperformance and punchy interest rate differentials will further support the koruna on its gradual appreciation path. At the same time, the CNB governor does not seem to be spooked by somewhat stronger koruna levels. We are on the same page, taking the stance that a strong currency generally reflects the decent structural shape of the economy, especially compared to other eurozone economies such as Germany or France. A solid fiscal stance and relatively low debt will become an even more tangible advantage in the not-so-distant future, providing more oomph to the domestic currency.

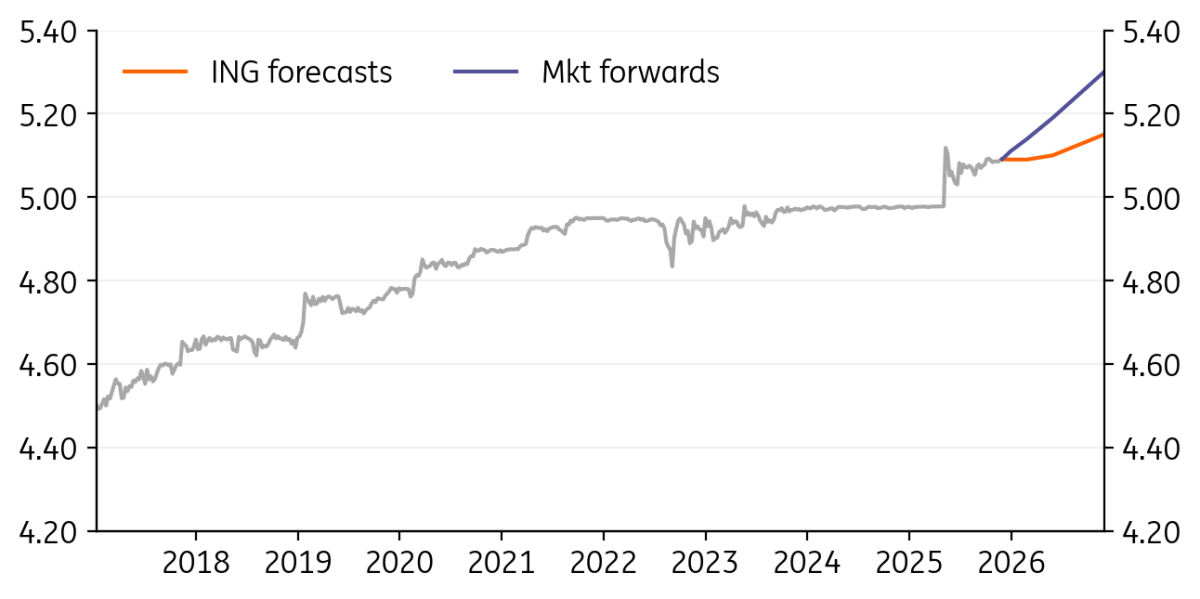

EUR/RON: No large changes expected ahead

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/RON

5.09

|

Neutral | 5.09 | 5.09 | 5.10 | 5.15 |

- EUR/RON has been pushing slightly higher in the 5.09-5.10 area, with some speculative flows potentially at play. Risks stemming from the fiscal situation have moderated for now but the political and inflationary developments continue to bring some uncertainties ahead.

- The visible improvement in the October budget deficit outturn (-5.7% vs -6.2% of GDP in 2024, same month), coupled with the European Commission’s suspension of the Excessive Deficit Procedure for Romania, bode well for Romania’s sovereign rating considerations ahead. Moreover, the tight deadlines for the National Recovery and Resilience Plan investments should keep economic activity afloat in the quarters ahead, despite rather lacklustre consumption recently.

- On the monetary policy outlook, our base case remains that the National Bank of Romania will start easing again from May 2026 onwards and we expect a total of 100bp of rate cuts through next year. We continue to expect policymakers to hold a firm grip on the currency, with the pair broadly stable ahead, ending the year around the current levels and 2026 at 5.15.

EUR/RSD: RSD adjustment unlikely to bring instability

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/RSD

117.40

|

Neutral | 117.40 | 117.30 | 117.20 | 117.20 |

- EUR/RSD went up through late November towards the 117.40-117.50 range from the previous range of 117.10–117.20. Uncertainties related to the impact of the NIS refinery shutdown, and its impact on the economy, have likely added some pressure to the currency. Fuel constraints impacting economic activity, as well as budget revenues to an extent, pose key risks ahead.

- Ultimately, before this event, Serbia’s macro fundamentals looked robust underpinned by strong investments, prudent fiscal policy, and ample FX reserves. Higher energy spending has been featured in the 2026 budget, which envisions a deficit of 3.0%.

- At its November meeting, the National Bank of Serbia kept the key rate in place at 5.75%, as global uncertainties continue to prevail. We continue to believe that FX stability should remain a key focus ahead, with the Bank buying a net EUR355mn as of October to keep the pair stable.

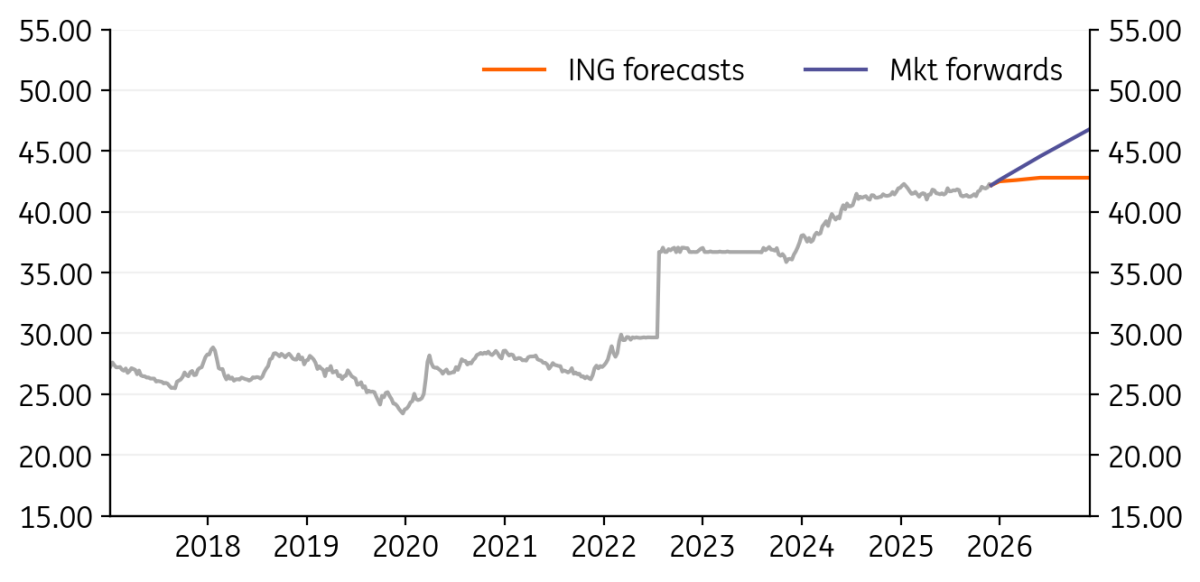

USD/UAH: Weaker UAH due to ongoing war

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/UAH

42.19

|

Mildly Bullish | 42.50 | 42.60 | 42.80 | 42.80 |

- The USD/UAH exchange rate rose in November and temporarily touched the 42.4 level – a multi-month high. The hryvnia remains under pressure due to ongoing war-related disruptions. Recent significant losses from intensified aerial attacks on critical infrastructure, power outages, and a shortage of qualified staff have impeded economic activity.

- Ukraine has reached an agreement with the IMF on a new arrangement to potentially gain access to USD8.1bln. However, the outlook for the hryvnia depends heavily on a possible peace plan with Russia. If conditions are strongly unfavourable for Ukraine, this could translate into a lower willingness to invest in the country or risk re-starting the conflict.

- Ahead of the December National Bank of Ukraine meeting, CPI inflation dropped to a yearly low but remained in double-digit territory. Despite the easing of inflation, the central bank remains cautious. This stance is helping to sustain demand for hryvnia-denominated assets and limits speculative pressure on the currency.

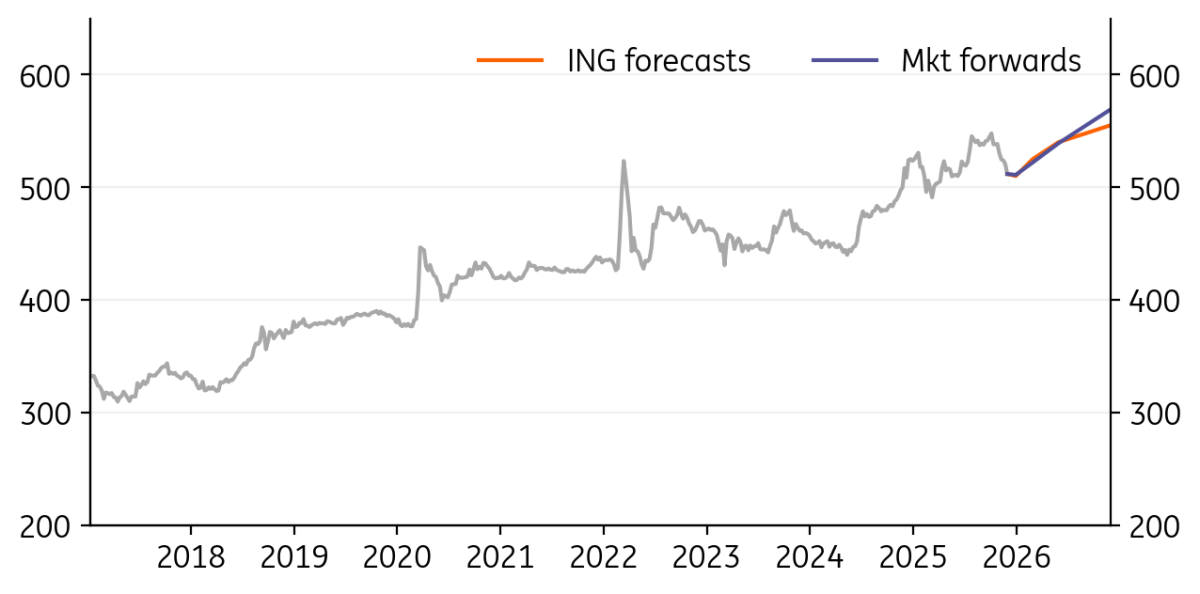

USD/KZT: Ending the year on a strong note

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/KZT

504.12

|

Mildly Bullish | 510.00 | 525.00 | 540.00 | 555.00 |

- The tenge rose 3.2% against the US dollar in November and continued to rally in the first week of December. While the direction of travel is aligned with our expectations, the scale of appreciation has exceeded our forecasts.

- The strong performance was likely supported by strong growth in oil exports (+23% year-on-year as of September), production (20% YoY in October), as well as persistently strong $1.5bn net FX sales by the government in November.

- We expect the tenge to finish the year on a strong note thanks to the robust near-term oil sector fundamentals and expected $1.4 bln net FX sales by the government in December. For the longer run, we remain cautious given the structural weakness in the balance of payments.

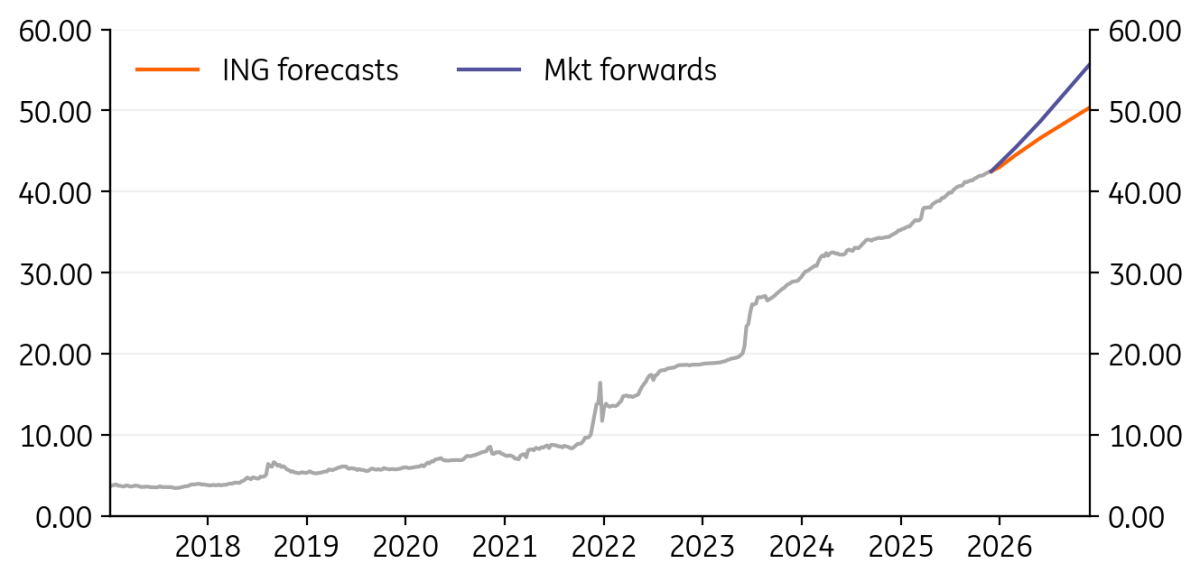

USD/TRY: Central Bank of Turkey likely to remain cautious

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/TRY

42.53

|

Mildly Bullish | 43.00 | 44.50 | 46.60 | 50.40 |

- Despite the headline weakness in third quarter GDP, the seasonally-adjusted quarterly pace has remained strong, defying earlier expectations of a significant slowdown in momentum. Meanwhile, leading indicators including the PMI, capacity utilisation, and consumer and real sector confidence point to an acceleration in GDP growth in the fourth quarter.

- While November’s inflation data supports continued easing, 3Q GDP and early 4Q indicators suggest demand is not soft enough to secure disinflation in line with the envisaged 2026 path. This increases upside risks to inflation amid ongoing rate cuts and looser financial conditions.

- Accordingly, the central bank will likely remain cautious, with a measured pace of cuts, driving the policy rate down to 38.5% in 2025 (from 39.5% currently) and to 27% in 2026. However, risks to the rate trajectory are on the upside given possible negative inflation surprises and the political newsflow.

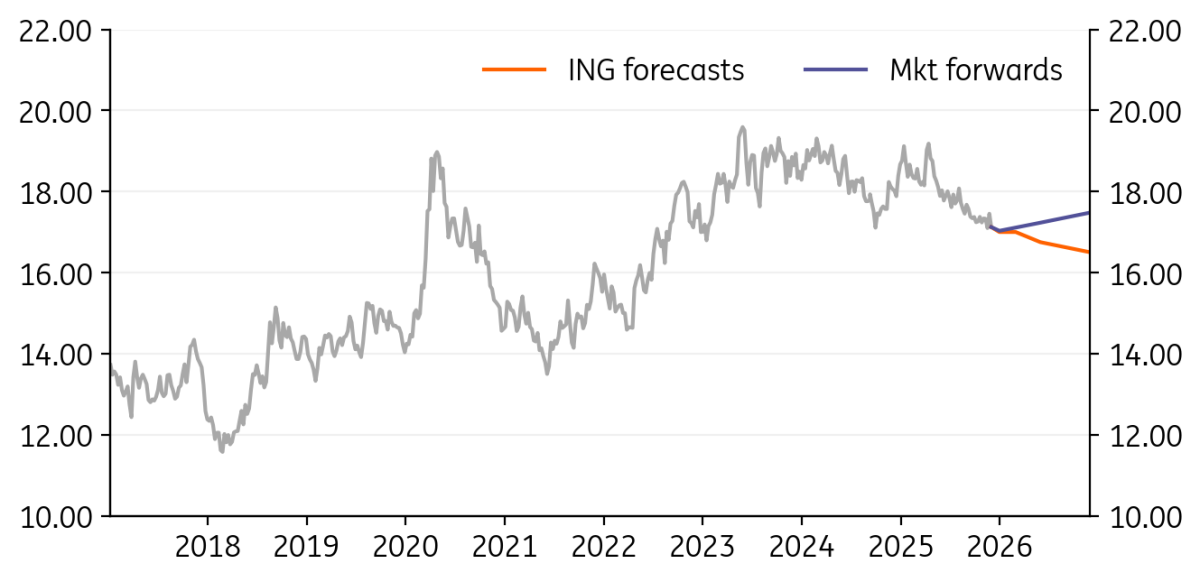

USD/ZAR: Lots of positives for the rand

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/ZAR

16.93

|

Neutral | 17.00 | 17.00 | 16.75 | 16.50 |

- We’ve previously talked here about the shift to a new CPI target (now 3% +/- 1%) and what it has meant for the bond market. Here, 10-year local government bond yields have fallen to 8.25% from 11% earlier this year. Last month’s sovereign upgrade by S&P has helped as well – the first adjustment since a downgrade in 2020. In addition, South Africa’s removal from the Financial Action Task Force’s grey list is good news for borrowing costs.

- Rising commodity prices and what they mean for the rand’s terms of trade is still very supportive as well.

- Growth forecasts are being revised up, and credit growth looks quite positive. USD/ZAR could head further under 17.00 this year.

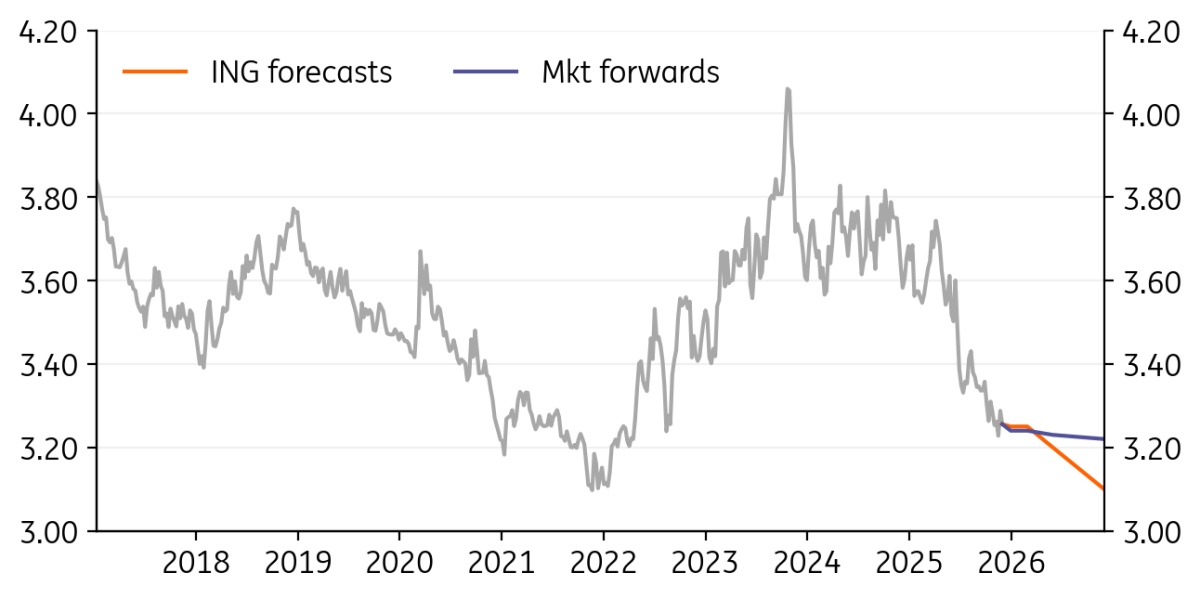

USD/ILS: Back to its lows

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/ILS

3.23

|

Neutral | 3.25 | 3.25 | 3.20 | 3.10 |

- The peace dividend in Gaza has seen USD/ILS drop back towards the lows of the year. Indeed, it briefly traded below 3.20 last month. Third quarter GDP saw a strong bounce-back after weakness in the second quarter, and the Bank of Israel is now hoping that some of the supply constraints will ease – especially in the labour market. It recently cut rates 25bp to 4.25% and the market expects another 100bp of rate cuts over the next year.

- The mild tech shock on the US left the shekel relatively unscathed and the Bank of Israel now says there are strong capital inflows to the Israeli tech sector this quarter. In the past, these have been worth as much as $5bn per quarter.

- We retain the view USD/ILS will be pressing 3.10 next year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Bundle

8 December 2025

FX Talking: We need to talk about Kevin

- This bundle contains 4 Articles