Electoral calendar and political risks in emerging markets in 2020

- 12 December 2019

Political risks in emerging markets have generally been associated with elections and on the face of it, 2020’s electoral calendar is busy as usual. However, most of them stand in the shadow of the US presidential elections and there is a lack of heavyweights compared to previous years. The focus will be on contested elections in Asia and sub-Saharan Africa

Emerging Market Asia

- In Sri Lanka, President-elect Gotabaya Rajapaksa is expected to call for snap elections in Feb 2020. This should see a consolidation of power with the nationalistic Sri Lanka People’s Front (SLPP) winning and Gotabaya’s brother, Mahinda, likely remaining PM. The power grab will make policymaking more straightforward but there are concerns on spending promises which are undermining an already stretched fiscal position and an ongoing US$1.5bn IMF Extended Fund Facility (EFF).

-

South Korea will hold parliamentary elections on 15 April with the Democratic Party (Minjoo) of President Moon Jae-in previously holding a comfortable lead over the Liberty Korea Party in polls but this has evaporated following the corruption allegations against the previous justice minister who stepped down in October. In line with this, approval ratings for Moon dropped to a low of 39% in mid-October.

CEE/CIS

- In Poland, the ruling Law and Justice Party (PiS) retained a single-party majority in the 13 October parliamentary elections, partially thanks to pre-election spending promises. Likely around May 2020, presidential elections will follow. PiS-backed incumbent President Duda should win in the first round but combined support for an opposition candidate remains a threat in a run-off and if so, would constrain the government due to the PiS’ insufficient majority to repeal a presidential veto.

- In Romania, the spotlight moves onto the parliamentary elections (by December 2020). The minority government under the National Liberal Party (PNL) has vowed to call snap elections but is unable to do so by itself. Major concerns have been voiced with a planned 40% pension hike in September 2020, thus an earlier election date would provide room to address the adverse fiscal impact with some anticipation. Since the European elections and a referendum on justice laws in May 2019, opinion polls have turned in favour of the PNL.

- We expect policy continuation following parliamentary elections in Serbia (April). In the same month, North Macedonia will hold snap elections (12 April) with a caretaker government in place from 3 January onwards. It remains a close call but the snub by the EU (on opposition from France) regarding accession status despite the domestically unpopular name change deal earlier in 2019 could support the opposition VMRO-Democratic Party for Macedonian National Unity.

- The electoral cycle starts in Croatia with presidential elections over the turn of the year (22 Dec and 5 Jan for run-off) with polls indicating a win for incumbent President Kolinda Grabar-Kitarovic. Parliamentary elections are scheduled a year later but an early election is possible. The ruling Croatian Democratic Union (HDZ) leads in the opinion polls. Watch for some pre-election spending (credit negative).

MENA/SSA

- Despite PM Abiy Ahmed’s political and economic reforms as well as a peace deal with Eritrea, Ethiopia has recently seen ethnic tensions and violence. Thus, a delay of the general elections (scheduled for May) can’t be ruled out. While the opposition has been historically weak, there has also been growing dissent inside the ruling coalition with Abiy’s plan to merge the coalition into a single party facing opposition.

- Meanwhile, Cameroon’s parliamentary elections which initially should have taken place already in 2018 have been set for 9 February – a further delay however remains a possibility. The 2018 presidential election outcome reaffirmed Paul Biya as President (in power since 1982) but was disputed by the main opposition (and led to the arrest of its leader) which has also called for a boycott of the upcoming elections.

- Elections in Ghana (by December 2020) are likely to remain relatively peaceful with the New Patriotic Party (NPP) and President Nana Akufo-Addo having a head start thanks to the strong economy, notwithstanding the key concern being the adverse impact of pre-election spending on much needed fiscal consolidation.

- The election outcome remains unpredictable in the Ivory Coast (31 October) as it is unclear whether incumbent President Alassane Ouattara will stand again or is allowed to do so. Outtara argues that a constitutional change in 2016 introducing a two-term limit for presidents doesn’t apply retrospectively – a final court ruling is still due. To complicate things further, the ruling coalition fell apart in 2018. 2015’s elections were peaceful, but the 2010 presidential elections resulted in a civil war.

- In Israel, we see higher chances for a second repeat election (currently not included in the electoral calendar) as Knesset lawmakers face an 11th December deadline to nominate a candidate and form a government. If unsuccessful, snap elections are likely by March. Moreover, PM Netanyahu has been indicated on corruption charges, although a trial is unlikely to start soon. He could stay as PM until convicted or a new coalition is in place. The lack of a working coalition has constrained policymaking, with the lack of a timely 2020 budget meaning curtailed expenditure.

Elections and political events in 2020

Political risks weigh especially on countries with weaker fiscal capacities

While electoral periods have often been the source of political risks, we have recently seen unrest and violence spreading across large parts of emerging markets with hot spots in South America and the Middle East.

The roots often lie in perceived corruption, social injustice and political freedom but it is impossible to capture all elements. The chart below compares countries in emerging markets on political stability and perception of corruption, and we find that many of the recent high profile protests take place in countries with weaker scores on both (highlighted in bold). Chile is an exception, considered as strong on both dimensions and yet facing prolonged unrest. To assess governments’ capacity to deal with dissent (often via social spending), we included government debt as a 3rd element (bubble size). Lebanon’s fiscal position is undeniably stretched while Chile and Peru have the most comfortable positions.

Political risks can be associated with weak political stability and perception of corruption

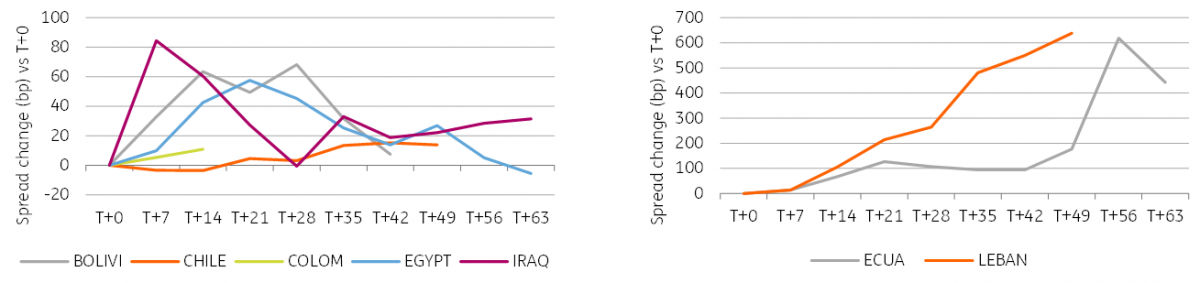

In line with this, we found that markets have reacted differently in each case. To set a playing field, we used US$-denominated sovereign bonds in the 10yr maturity bucket of selected sovereigns. The two charts below display the spread reaction of those following the start of protests, with T+0 being the week preceding the risk event. The spread widening has been large for fundamentally weaker sovereigns while limited for investment grade names (e.g. Chile/Colombia). Ecuador and Lebanon remain under heavy pressure due to the urgent need for reforms and limited room to manoeuvre. Others have seen some relief but are not out of the woods (notably Iraq).

Chile/Colombia insulated, Bolivia/Egypt/Iraq recovering vs substantial sell-off in Ecuador/Lebanon

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more