ECB Cribsheet: No fireworks just yet

As the ECB officials already adjusted market expectations for the ECB meeting tomorrow and no tapering is expected, the impact on EUR/USD should be limited. On balance, risks are skewed to modestly higher EUR/USD as expectations are low and communication missteps cannot be ruled out. But expect generally unaffected EUR/USD

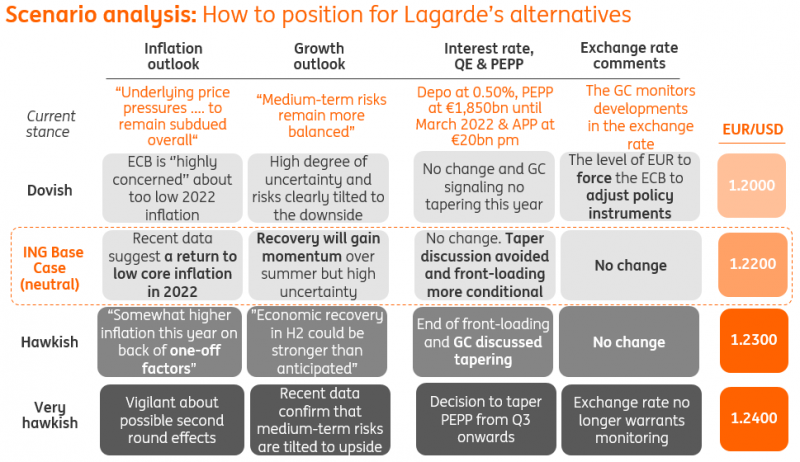

Limited impact on EUR

We expect the ECB to avoid any tapering talk, but given that this has already been communicated by ECB officials (see the ECB Preview for more details), this should not come as a surprise to markets and in turn, should have a limited impact on EUR.

Given the expectations of no change in guidance on asset purchases, the balance of risks is modestly skewed to a higher EUR, should the press conference not reiterate the tapering on hold message strongly enough or deliver some communication missteps.

Given the expectations of no change in guidance, the balance of risks is modestly skewed to a higher EUR

While not our base case, the probability of this outcome is in our view higher than of an even more dovish message vs the current already cautious market expectations. Hence the balance of risks is skewed to modestly higher EUR/USD, even if our base case is for a largely unaffected EUR/USD after the meeting.

As an aside, we note that comments from Banque de France Governor, Villeroy de Galhau, in late May did coincidentally put a top in EUR/USD at 1.2250. He said the ECB would be as least as patient as the Fed. We read this as an expression of EUR/USD sensitivity from the ECB and it will be interesting to see whether these comments re-appear in some form. Typically, central bankers would be reluctant to discuss the policy of their central banking peers at a high-profile rate meeting. And remarks of relative monetary policy settings could be frowned upon in Washington as a quasi means of verbal intervention.

The constructive outlook for EUR/USD remains intact

Beyond the June ECB meeting, we retain our constructive view on EUR/USD and target the 1.25 level this summer.

The upcoming improvement in Eurozone data and the growth outlook should help limit the US and Eurozone growth wedge. With the Fed remaining cautious and presiding over deeply negative US front-end real rates, the subsequent soft USD environment should help facilitate higher EUR/USD.

Also, with the global economy showing signs of more synchronised recovery, the EUR should benefit more given the openness of its economy

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more