Earning in retirement: The new norm?

- 20 February 2019

Can you afford to retire? Will you have to carry on working until you 'drop'? The results of the latest ING International Survey suggest it's a real worry for nearly two-thirds of people across Europe, the US and Australia, and notably in Spain, France and Poland. Download the full report here

Saving woes stretch retirement outlook

People in Europe, the USA and Australia could be sleepwalking into long-term saving and spending problems. That's the message from the latest ING International Survey which indicates that many of us are really worried about retirement, not least because we're having trouble making ends meet right now and finding extra cash to put aside for later is difficult for many.

Download the full IIS report here

Planning for retirement is no longer , saving now to live later. Our expectations of continuing to earn in retirement point to a new view of life after full-time work. We tend to focus on the present meaning that planning for the future can take a backseat, particularly for something as far in the distance as retirement. Future needs are less salient than others. But that is not the whole story. Many , don't earn enough to save. Here is where we stand today and how we might clarify retirement challenges by tapping into our sometimes quirky relationship with money.

Future obstacles

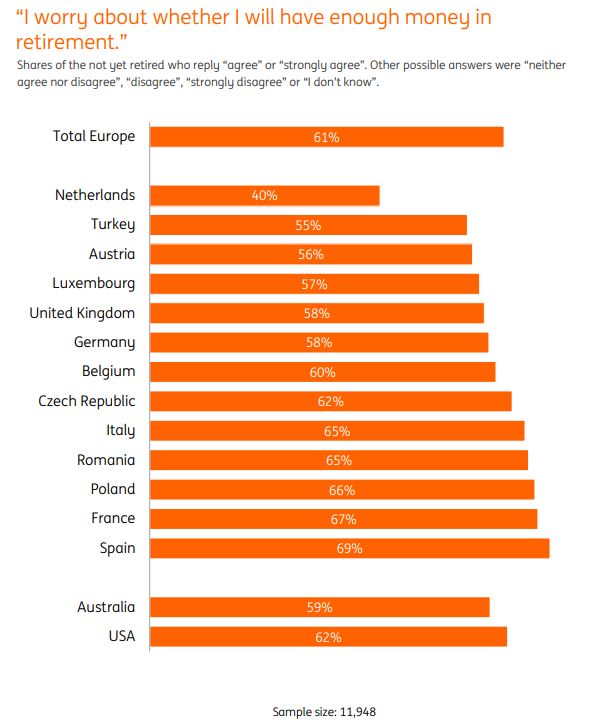

Many people say that they worry about having enough money in retirement. In fact, two in every three people agree with this statement. Retirement can be a challenging concept to plan for.

For the young, retirement can feel like an incredibly long way off, making prioritising and planning less of a focus. Yet by the time we get to retirement, it’s often too late to make any big changes that will drastically improve our weekly budget. And because , isn’t necessarily an immediate issue, it can be forgotten in the short term. There isn’t an obvious time to sit down and do the sums on retirement.

Worrying about money

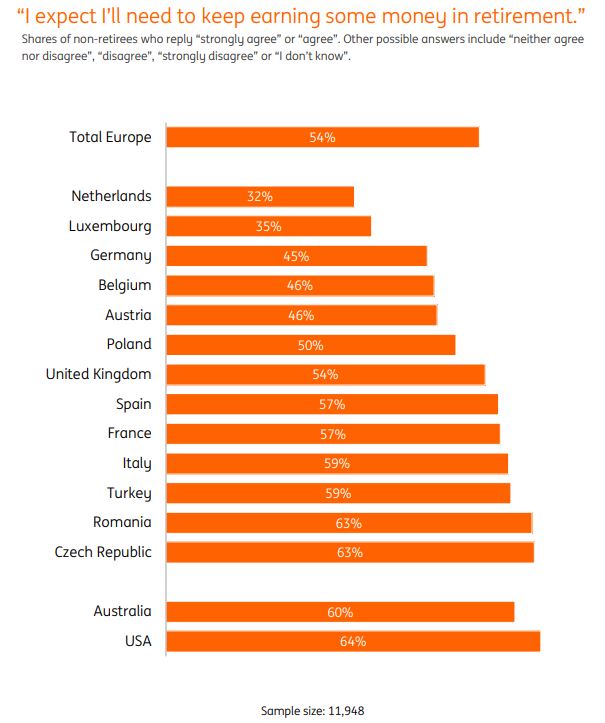

My retirement will be…..

But just 26 percent of those in Europe who aren’t retired, expect to have the same standard of living post full-time work. Even though 47 percent of us don’t know how much goes into our retirement savings each year and 36 percent don’t contribute in addition to what’s put aside by employers or the state.

Because people feel uncertain about their retirement and there is a general feeling of ‘not having enough money’, many assume they’ll need to keep earning. More than half of these expect to do this through working in the gig economy or temporary positions.

Worry seeps into plans for continuing to earn in retirement but is not necessarily enough to convince us to sit down to calculate how much extra we could be putting away into retirement each week. Retirement can be considered a ‘future problem’ , putting money away is a loss now.

People also have very wide-ranging predictions for how much they will need to live in retirement. In our European sample of those aged 25-34 years, 18 percent predicted they would need between 100 and 500 thousand euros if they never had to work again, while 19 percent predicted they would need between 1 million and 3 million euros. A quarter thought they would need more than this to never need to work. A natural aversion to calculating and a preference for round numbers means that if asked, many will pick a number that sounds reasonable to them.

Keep on working?

Managing what we have

Taking the hit now to put away for later feels like a loss. If we don’t feel we have to, it can be easy to question why we should do it right now. But it’s not just loss aversion or challenges planning for the future at play here. Many don’t have the option to put more aside for retirement.

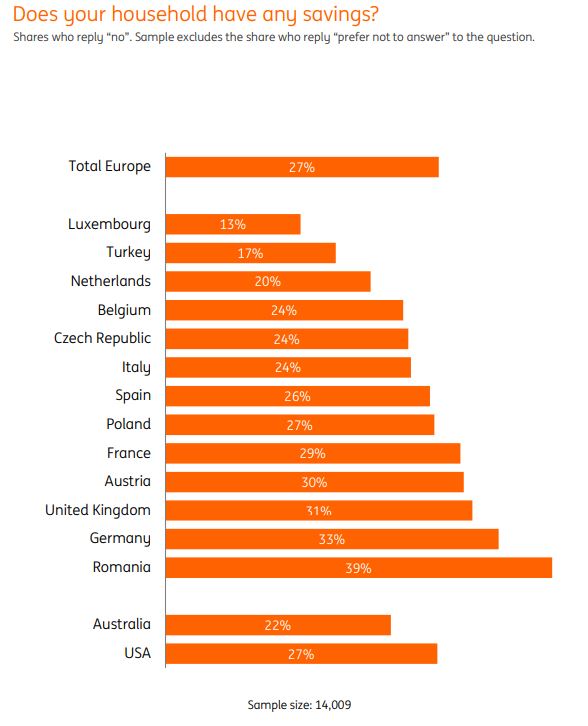

Of the quarter of us across Europe who have no savings, 66 percent say that they don’t earn enough to save. Half of us also say we sometimes run out of money at the end of the pay period. And while most of us can reduce spending in order to manage until the next pay comes in, three in ten say that they turn to credit cards and one in five borrow money from friends or family. While credit card debt comes with the risk of interest charges eating further into our limited saving capacity, introducing money into relationships also comes with risks. Strained relationships add to the stress of running out of money before the next pay cycle.

Saving and investing are sensitive subjects, particularly in relation to the relatively overwhelming topic of preparing for retirement. And this is not helped by the fact that we often feel uncomfortable talking about our finances. Because of this we tend to shy away from asking questions that could provide useful advice in navigating financial challenges. It would be an important step forward to open up these conversations in a way that responds to our natural disposition to avoid this potentially prickly topic. This can help bring the future into the present and integrate retirement saving into every-day thinking.

More than a quarter of Europeans have no savings

Can technology help us save for the long-term?

Another way we can integrate future-focused planning into the more manageable context of day-to-day is the myriad of personal finance apps that are entering the market. What our results suggest, however, is that Fintech is not having a large impact on personal investing which can support longer-term saving. Instead, most mobile bankers are using apps for spending and transferring money.

Planning in advance, such as for retirement, comes with unique challenges. While our financial position is influenced by multiple factors outside of our control, such as low wages or unexpected expenses, our habits and behaviours directly contribute to our long-term financial wellbeing. It will pay to know the basics of what your retirement years might look like, even if you don’t feel you can save any more right now. Knowledge is a powerful thing.

Read the entire ING international Survey report here

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

In case you missed it: Hoping for stability

- This bundle contains 8 Articles