Dutch industry goes from top gear into reverse

- 2 February 2023

- Manufacturing, Construction and Retail The Netherlands

High prices and stagnating demand are causing a turnaround in the Dutch industry. After two years of strong growth, increasing headwinds lead to a moderate correction in output in 2023. However, developments differ strongly between industrial subsectors

Slight contraction in 2023

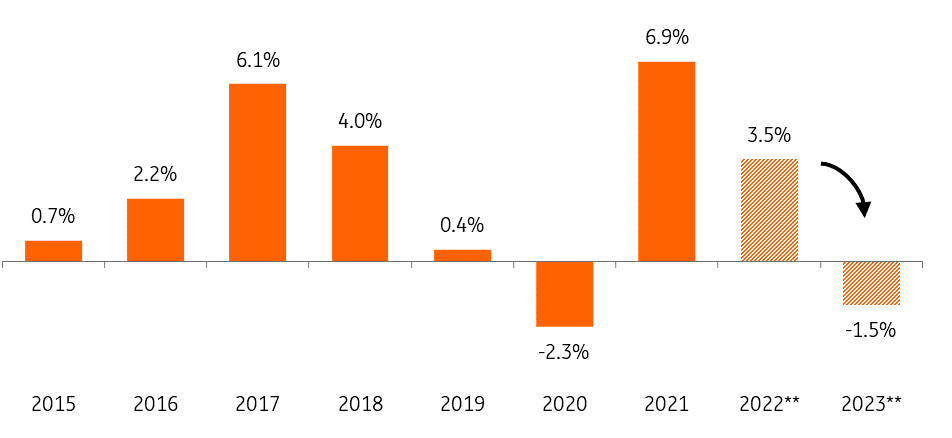

Dutch industrial production has been on a downward trend since May 2022. Major causes for this are high energy and material prices, the weakening global economy and the shift in consumer preference from goods to services since the economy reopened post-Covid lockdowns. Domestic and foreign demand for Dutch products will remain under pressure in the first half of 2023. Thanks to a strong first four months of the year, there was still growth on average in 2022. In 2023, the opposite will be the case. The year starts with a contraction, after which, at best, moderate growth will not push the annual figure above zero. Moreover, the downside risks of persistently high purchasing and energy prices on demand and further scaling-down of production in basic industries remain high.

Dutch industry from growth in 2022 to contraction in 2023

Volume growth of Dutch industry*

High energy prices and destocking weigh on production...

While stocks of finished products have long been insufficient due to supply and production disruptions, they are now at unprecedented levels relative to demand. Producers are almost as negative about their sales stocks as they were shortly after the outbreak of the Covid-19 pandemic. As a result, they have to eliminate their surplus sales stocks before increasing production again.

Producers are more negative about sales stock than at the start of the pandemic

Manufacturers' assessment of stock of finished product*

...especially in energy-intensive basic industries

The bullwhip effect that previously accelerated inventory building is now causing the reverse effect. Suppliers and end producers are reducing their stocks in line with the expected drop in sales, causing a decrease in purchasing activity. Suppliers are also reducing their inventories, but at the same time see sales immediately decline, which means that stock positions are reduced even further. Together with production restrictions due to high energy costs, this leads to a strong decline at the beginning of production chains, such as in the base chemical, base metal and plastics industries.

Strongest decline in energy-intensive industries, strongest growth in production of pharmaceuticals and capital goods

Production development of the three fastest growing and three most contracted Dutch industries, December 2021 to November 2022*

Demand will not bounce back strongly

Given the large sales inventories and the moderate economic outlook, renewed industrial growth in the Netherlands is unlikely to be exuberant over the course of 2023. Domestic demand is under pressure for the time being due to persistently high prices that hinder both consumers and businesses. Domestic investment is expected to contract slightly and household consumption will barely grow. International demand may gradually increase, but due to limiting factors such as high and volatile (energy) prices, renewed growth probably remains moderate. Energy prices are expected to remain relatively high and volatile.

Production levels fell much less than energy consumption due to savings

Despite a decline since May, total industrial production held up quite well in 2022. In November, it was still 8% higher than at the beginning of 2020 just before the pandemic started, after peaking at 14.5% in April. At the same time, industry consumed on average 30% less gas. Producers are reducing gas intensity by limiting production, purchasing more semi-finished products from outside Europe and saving energy. In addition, alternative fuels are being used more often, such as LNG, coal or oil products, such as naphtha, or residual gases, such as fuel gases from petrochemical crackers.

Strong import growth of intermediate goods

Production remains relatively high, partly because intermediate goods – normally produced using highly energy-intensive processes – are increasingly imported from Asia and the US. They serve as a substitute to keep the production of final products up when domestic intermediates' production has been curtailed. Think of ammonia, which is needed for fertiliser production, and of aluminium and zinc (non-ferrous metals), which have a wide variety of applications. This does not always prevent companies that are highly dependent on the gas price from having to reduce or shut down their production.

Imports of energy-intensive basic products increased sharply

Growth of import value per commodity category in 2021 and 2022 compared to the same period in 2019, total Jan.-Sept.*

Industrial gap: high-tech industry will grow in 2023…

As long as supply chains continue to recover and overdue production continues to drive growth in specific sub-sectors, the industry as a whole will not experience a deep trough in 2023. Due to filled order books and high production backlogs, the internationally interconnected transport equipment industry and the high-tech industry are expected to continue to grow in 2023. The impulses of the ongoing digitisation and electrification are an important growth engine. With companies such as ASML, ASMI, NXP and Besi and large suppliers such as VDL in its ranks, the Netherlands plays an important role in the structurally growing semiconductor industry.

Order books in the technology industry are still well filled

Assessment of order book level, Dutch industry*

…while energy-intensive industry is declining

The still relatively high gas price continues to dampen production, also because more and more old energy contacts are coming to an end. This puts the most pressure on production in the (petro)chemical, base metal and plastics industries. Due to the large cost share, the processes in those industries are already very energy-efficient and extensive energy savings are difficult or very costly and time-consuming. Many chemical companies also use natural gas as a raw material for their products, which means that rising energy prices hit them extra hard. Examples include Yara, which reduced its ammonia production for fertilisers, OCI, which produced less ammonia and methanol, and Nobian, which reduced salt production. Many companies at the Chemelot chemical complex have also considerably scaled back production or even shut it down completely as high gas prices reduce profitably. The fall in energy prices due to the mild winter weather offers some welcome relief.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more