Dutch consumers keep spending despite plunging confidence, ING data shows

- 20 May 2026

- The Netherlands

Dutch consumers are continuing to spend at a steady pace despite a sharp decline in confidence in April due to the Middle East conflict. ING transaction data suggests the deterioration in sentiment has yet to translate into actual spending behaviour, with little evidence of a meaningful pullback despite rising uncertainty and higher petrol prices

Consumer confidence has dropped near all-time lows on Middle East war

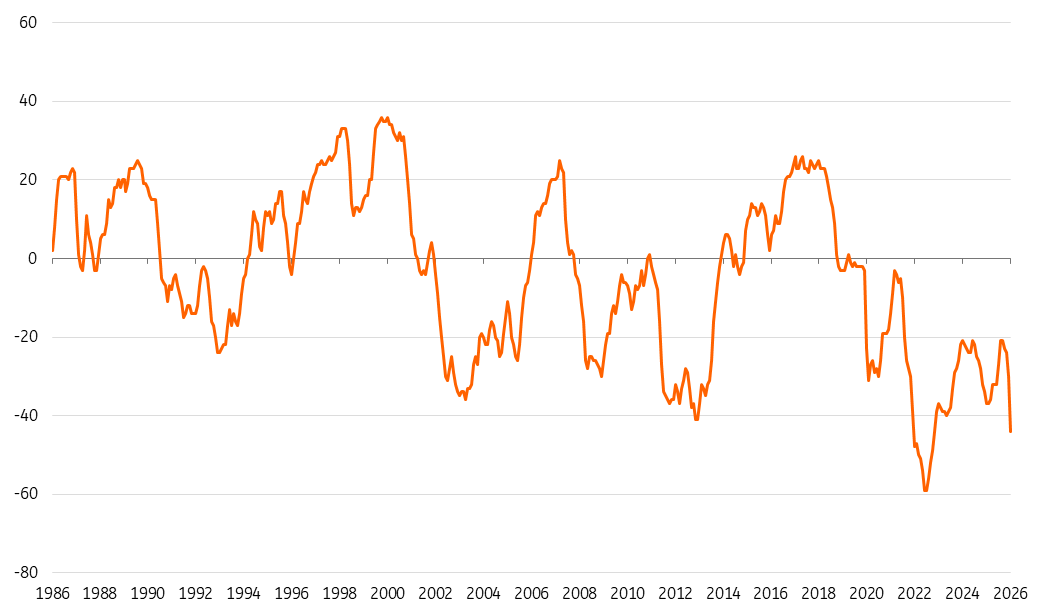

In the Netherlands, the economic impact of the conflict in the Middle East has been limited so far, largely confined to higher fuel prices. Yet consumer confidence has dropped sharply. This downturn in sentiment comes against an already fragile backdrop. Since the 2021–22 energy crisis, Dutch consumers have remained structurally downbeat, with high prices and geopolitical tensions weighing heavily. The fall in confidence from -24 in February to -44 in April therefore feels like a familiar pattern: here we go again.

The current level of consumer confidence is now the lowest on record outside the previous energy crisis. And indeed, a recent ING survey suggests that the majority of Dutch households intend to cut back on expenditures due to high prices.

Confidence close to record lows

Netherlands consumer confidence index, seasonally adjusted

Consumers have not changed spending patterns - yet

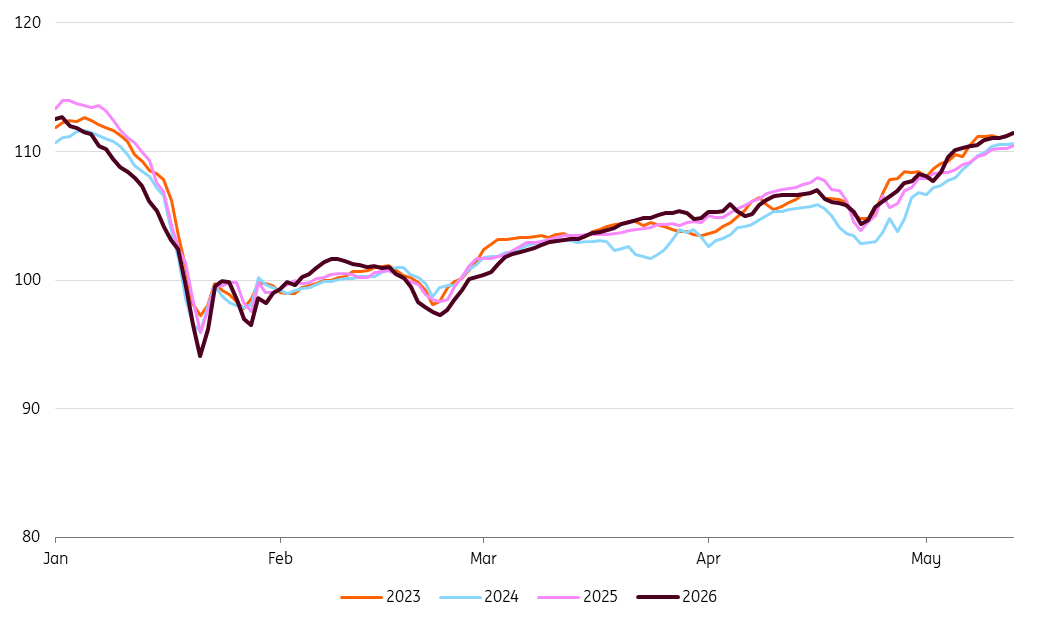

Still, consumers have not yet tightened their belts significantly. Aggregated ING transaction data of Dutch customers indicates that spending had not seen a material negative impact as of 13 May.

In March, the first month of the war, Dutch spending growth actually accelerated despite falling confidence and increased uncertainty. The mild March weather seems to have played a role as categories like fashion and recreation and culture saw an increase in spending. This still holds true when correcting for inflation.

April presents a somewhat muddier picture, as inflation data has so far not been published for the Netherlands and a higher number of holiday days led more Dutch consumers to spend time abroad. Even so, transaction values increased again despite one of the lowest confidence readings on record. Adjusting for inflation will likely show slower growth, but not an outright decline, based on our headline CPI forecast for April.

So far in May, there are also no clear signs of a shift in spending behaviour. While precise comparisons are complicated by the timing of weekends and public holidays, the overall pattern remains broadly in line with previous years, suggesting consumers are not yet cutting back.

No material negative impact on spending for now

Value of transactions* (28-day moving average as index, February = 100), not adjusted for inflation

No drastic cuts to discretionary spending

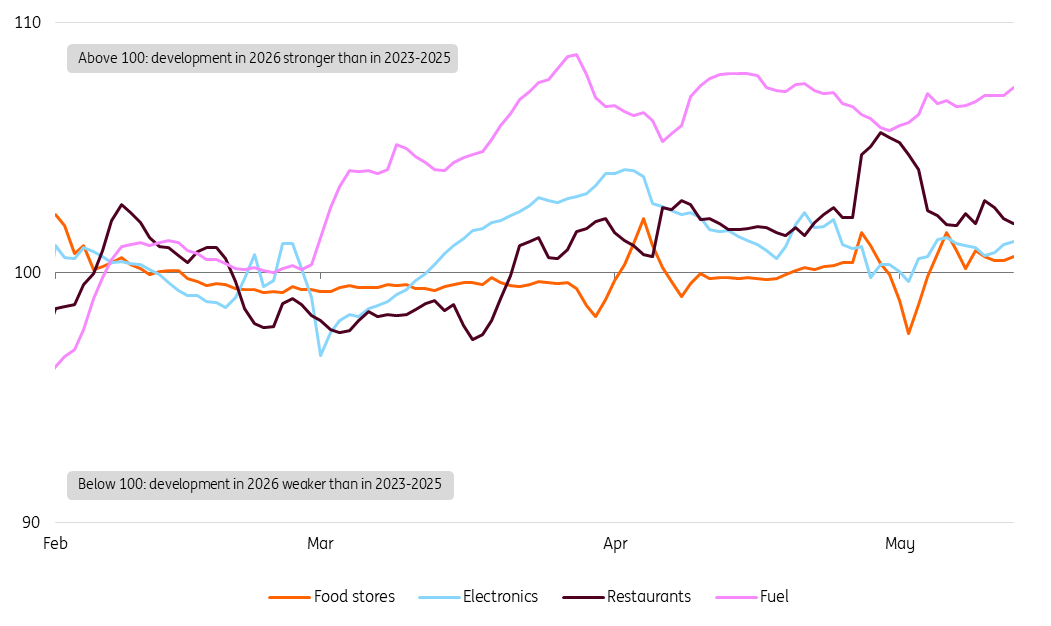

Of course, transaction values at the petrol station have increased. Higher prices result in higher turnover at the pump. But so far there is no clear spending category which has suffered. For essentials like supermarket spending, we see a similar pattern to recent years, while it is slightly higher for personal care spending. The data over a short period of time is influenced by weather conditions, and holidays, etc. But there is little indication that people have been cutting back.

When comparing transaction values in 2026 to the three years before, growth has been faster in restaurants and, to a lesser extent, in electronics. These are hardly necessities. Recreation and culture spending lag behind somewhat, but spending on media is similar to the trend in recent years while home and garden spending is up a bit. Overall, the picture shows no significant change in discretionary spending.

Spending patterns relatively unchanged compared to previous years

Value of transactions* (28-day moving average as index, February = 100), development in 2026 compared to average of 2023-2025, not adjusted for inflation

Muted spending ahead but no cliff edge decline

The resilience in spending so far reflects the support Dutch households are still receiving from high savings, low unemployment and decent wage growth from a historical perspective. However, the outlook for household consumption remains highly uncertain, given the wide range of possible outcomes from the Middle East war.

In our base case, we expect growth in spending to become more muted over the months ahead. So no sharp drop off, but clearly some effect from the global turmoil is still to come. For now, Dutch consumers are surprising to the upside – no matter what they say in surveys.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more