Signs of a 2024 recovery emerge for Dutch commerical real estate

- 8 November 2023

- Real estate The Netherlands

Increased interest rates and investor risk perceptions of the real estate market are set to put downward pressure on real estate prices in the Netherlands until mid-2024. Demand is expected to pick up after that, but we expect a fair bit of divergence in the timing and pace of recovery for the residential, retail, office and logistic segments

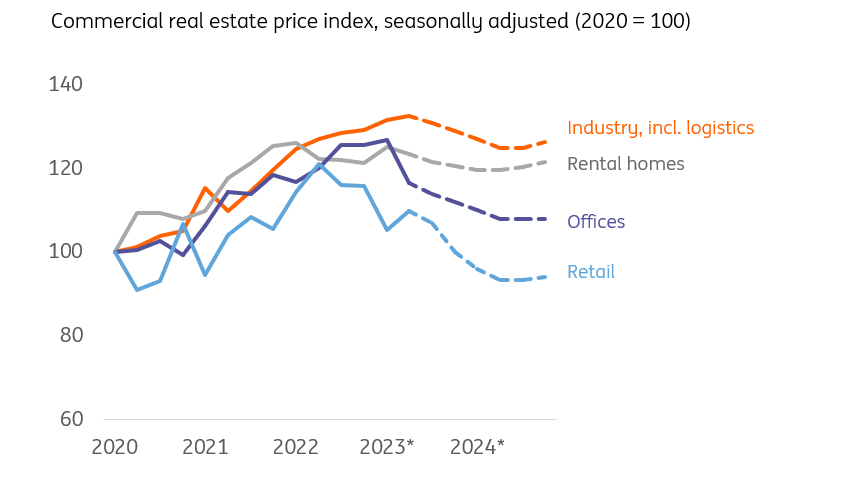

Real estate market hit hard by higher interest rates

The sharp rise in capital market interest rates throughout 2022 has seen the investment volume (the total value of all investment transactions) in the Dutch real estate market fall by more than 60% in the first half of 2023 compared with the same period last year.

Investors are still reluctant to make purchases in the commercial real estate market and are no longer willing to pay current market prices due to rising interest rates and major economic uncertainties. The prices of larger transactions, in particular, have fallen significantly, and the drop in prices of smaller transactions has been much lower. Even so, we do expect further price declines in this part of the market before investor demand picks up.

Real estate market cools further in first half 2024

We expect to see further price declines in the commercial real estate market in the first half of 2024. While the possibility of slightly lower interest rates may provide upward price pressure, three key developments will continue to apply downward pressure in the near future:

- Investors are unwilling to pay current prices because of higher interest rates and increased uncertainties. Prices have not yet adjusted completely to the higher interest rates and economic uncertainties, and this will continue to put downward pressure on prices in the commercial real estate market for some time to come.

- The cooling down of the economy will become more visible. The sharp rise in capital market interest rates is working its way through the economy with a delay and will further slow down its growth. In the non-food retail market in particular, this will translate into more bankruptcies, business closures and higher vacancy rates in the coming period but will also slow user demand for offices and logistics real estate.

- Refinancing issues will become more frequent but will remain limited. Real estate investors whose financing expires will be looking for refinancing. This will not always be successful as a result of higher financing costs and lower collateral value due to lower property prices. This may increase the number of foreclosures and, therefore, increase downward pressure on property prices. For now, we expect the impact to remain limited in the coming year, in part because lenders set their lending conditions in such a way that there is room to absorb economic setbacks (such as higher interest rates).

Structural scarcity as a crucial strut

While the real estate market is expected to cool down further in the first half of 2024, structural scarcity in the market for rental housing and logistics real estate mitigates the downward pressure on prices in these segments. And in the office market, sustainable offices on A-locations remain in demand due to limited supply. We therefore expect relatively small price declines in these segments.

Dutch commercial real estate market recovery in the 2nd half of 2024

Recovery from second half of 2024

In our base case scenario, we expect that the commercial real estate market will reach its lowest price level in the second half of 2024. Important assumptions here are that capital market interest rates will at that point be slightly lower than they are now – and that the Dutch economy will be able to avoid a prolonged recession.

Given the different structural trends in the markets for residential real estate, offices, retail and logistics real estate, the timing and speed of the recovery will differ per segment. Below, we discuss the most important developments for each segment.

Residential real estate

Certainty about future policies important precondition for recovery

Demand from housing investors will remain low in the coming period because of policy uncertainty, particularly that which surrounds the plans of the Dutch government to regulate the middle rented sector. At the same time, these uncertainties will increase the supply of residential homes by investors as the plan to regulate rents lowers expected investor returns on housing investments. Both developments play a role in increasing downward price pressure.

Nevertheless, further downward revaluations in the rental housing market are expected to remain limited due to the structural scarcity in the housing market. Moreover, the scarcity of homes is expected to increase in the coming years as new construction output falls short of expected potential household growth.

We expect prices of owner-occupied homes to rise again by next year, mainly due to the vast income growth of homebuyers in 2023 and 2024. Because of the option for investors to sell rental properties on the market for owner-occupied homes, the development of both rental and owner-occupied home prices follows a similar trend over time. The recovery of the owner-occupied housing market will therefore limit the cooling down in prices on the Dutch residential real estate market.

Demand for sustainable offices on A-locations remains solid

The continued consolidation of service sectors and the cooling down of the economy will reduce user demand for office space – and adding to this are the more negative effects of working from home. An increasing number of employees have started to work from home since the Covid-19 pandemic, and the toll this has taken on office demand will soon become more apparent. This is largely a result of the lag between when companies decide to terminate existing leases, and the point at which they're actually able to do so. Additionally, companies needed some time to find out the effect of this trend on their office space needs. By now, companies have a much better understanding of this and will act on it more often in the near future.

The drop in demand will not affect all office segments equally. Sustainable offices on A-locations will suffer the least from the drop in investor demand in the coming period, which is due to both the limited supply of these offices and their future-proof nature.

A gloomy outlook for non-food retail

In the short term, non-food retail sales are set to decline due to the cooling economy and relatively high inflation. Many retailers are also facing higher costs – including personnel and purchasing costs – while some also need to repay tax debts accrued during the pandemic. This is expected to translate into an increase in bankruptcies and business closures and also increases the likelihood of vacancies. In turn, this raises downward pressure on the investment value of retail properties in the non-food segment.

Slowing price growth for logistics

In the short term, the logistics sector will be affected by the growth slowdown in China and the ailing German industry, as the consequent drop in international trade slows user demand for logistics real estate. However, we may also see some effects moving in the opposite direction –including the ways in which the pandemic has exposed the vulnerabilities of international production chains. This has increased the buffer stocks that companies want to hold and has a positive effect on user demand for logistics real estate as a result. In addition, the supply of logistics real estate is still low compared to demand, and the risk of long-term vacancy is therefore limited. This scarcity puts a floor under the prices of logistics real estate in the Netherlands.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more