Dutch commercial property market sees first signs of recovery, but uncertainty remains high

- 4 March 2024

- Real estate The Netherlands

Dutch commercial property prices are expected to stabilise in the first half of 2024. The scope for price growth in 2024 remains limited due to the reluctance of residential investors and declining demand for office space, and increased bankruptcies in non-food retail

Dutch commercial property market: cooling most evident in large transactions

The sharp rise in capital market interest rates in 2022 has lowered investor demand for commercial real estate globally. The same holds for the Netherlands, where the investment volume (the total value of all investment transactions) in the real estate market fell 53% in 2023 compared to 2022. For transactions of at least €100 million, which mainly involve institutional investors (including pension funds and insurers), volumes fell by about 70%.

The larger cooling in this part of the market was largely due to the rapid rise in interest rates in 2022 and increased risk perception in the commercial real estate market. This made it relatively more attractive for institutional investors to invest in less risky types of capital, such as government bonds, rather than real estate funds. It has also made it less easy for larger funds to take out bank loans. Looking ahead, realised price declines and slightly lower interest rates will help the market to recover.

Dutch commercial property prices stabilise earlier than expected

Prices in the commercial property market appear to be stabilising earlier than we expected last autumn. Back then, we assumed price stabilisation in the second half of 2024. There are three main reasons for the faster recovery:

1. Borrowing costs again lower than the peak in 2023: capital market rates have slightly fallen again since peaking in the third quarter. Compared to the peak in 2023, the five-year IRS rate is about 70 basis points lower again and this lowers the cost of financing for the commercial real estate market. Explanations for the lower rates are the declining trend in inflation and expectations that the European Central Bank will gradually start to lower policy rates after mid-2024.

2. The Dutch economy is holding up well so far: after three quarters of slight economic contraction, the Dutch economy exited the recession in the fourth quarter of 2023. Consumers spent substantially more during this period, and the labour market remains strong, with low unemployment (3.6% in January 2024) and employment growth in almost all sectors. This ensures that vacancy rates in all segments remain (historically) low so far.

3. Structural scarcity provides important support: the structural scarcity of rental and logistics properties provides important support to the market value in these segments. All else equal, this increases the scope for further rent increases and therefore has a positive impact on expected investment returns and property prices. Investors in both the rental and logistics property segments will therefore be more inclined to postpone their sale in case of disappointing investor demand. This thus limits the influx of new supply to the market, which helps prevent a downward price spiral in the Dutch commercial property market for logistic and residential properties. In the residential market, investors who fear the effects of the proposed rent regulation still have the option of offering properties in the owner-occupied housing market, where house prices have started rising again.

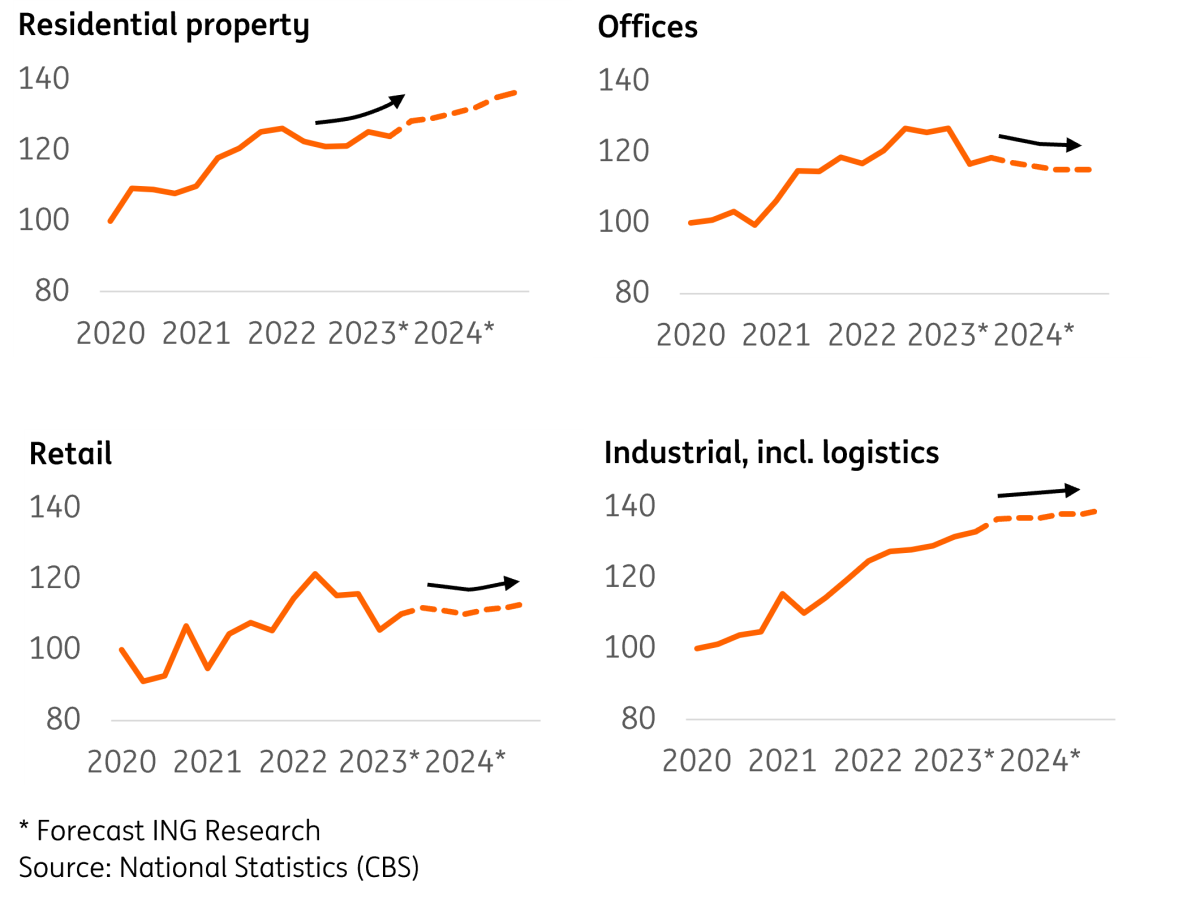

End of Dutch commercial property price falls in sight

Commercial property price index, seasonally adjusted (2020 = 100)

Limited room for price growth in 2024

Although prices are stabilising, the scope for price growth remains limited in 2024. A combination of further rent increases and further interest rate cuts would be needed to meet investors' yield requirements. In addition, economic growth prospects in the Netherlands are only moderately positive and economic uncertainties remain high. Moreover, problems with refinancing could cause downward price pressure to intensify in the coming period.

Uncertainties high, especially downside risks

Although the above scenario of price stabilisation in the Dutch commercial property market seems the most likely at the moment, the uncertainties surrounding this scenario are higher than usual. Moreover, the risks around key drivers in the commercial property market - such as interest rates, inflation and refinancing risks - appear to be mainly downside risks.

In addition, the Dutch rental housing, office, retail and logistics property submarkets each have their own dynamics and trends. We discuss the main market and policy developments below.

Rental homes: no further price declines despite investor reluctance

Residential investors will remain reluctant to make new purchases as long as the uncertainties around the plans to regulate rents persist. In addition, unfavourable fiscal policies implemented in 2023 have also reduced investor interest in the Dutch residential property market compared to previous years. At the same time, we expect more demand for residential properties from investors whose strategy is to sell rental properties in the owner-occupied market after rental contracts expire. Given the structural tightness in the Dutch housing market, investors expect they will be able to make favourable returns in this way.

Offices: demand for office space decreases further

Limited economic growth, further consolidation of service sectors and staff shortages are curbing demand for office space. In addition, the number of bankruptcies is expected to increase and the shift to working from home will further reduce demand for office space in the coming period. These developments will put downward pressure on office values. On average, the decrease in value will be greater for less energy-efficient offices and offices in less accessible locations. Energy-efficient offices in easily accessible locations remain in demand due to their limited supply.

Retail (non-food): improved purchasing power contributes to recovery

A combination of lower inflation, higher wages and an improving housing market means consumers will, on average, have more to spend this year. However, the number of bankruptcies in the non-food sector is rising further, especially among clothing and electronics businesses. This limits the scope for further price growth in the retail property market.

Logistics property: structural scarcity remains important support

Despite moderate economic growth in the short term, longer-term growth prospects for the sector are positive. Moreover, the current supply of logistics property is still scarce compared to the demand This increases the scope for further rental growth and puts upward pressure on the price development of logistics property.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more