Despite a softer economic outlook and rising costs, activity in the Netherlands remains resilient

- 15 June

- The Netherlands

Dutch businesses have become more pessimistic about the economic outlook as energy costs are elevated, yet short-term expectations for their own activity have held up relatively well. This divergence points to uncertainty, suggesting that economic growth will remain subdued in the quarters ahead

Some solid monthly data

The first hard data for second quarter 2026 suggest that it might not be such a bad quarter for GDP, with the possibility of stronger growth than in the first quarter. Goods export volumes growth accelerated to 4.4% year-on-year in April, while the expansion of goods imports dropped to 1.2% YoY. Manufacturing production rose by a considerable 1.3% month-on-month in April, mainly due to the continuing strong growth in machinery and a strong recovery in electronics. And the manufacturing PMI rose further to a level of 55, indicating decent growth for the rest of the quarter. Encouraging was the fact that the rise in PMI was visible in almost all underlying indicators.

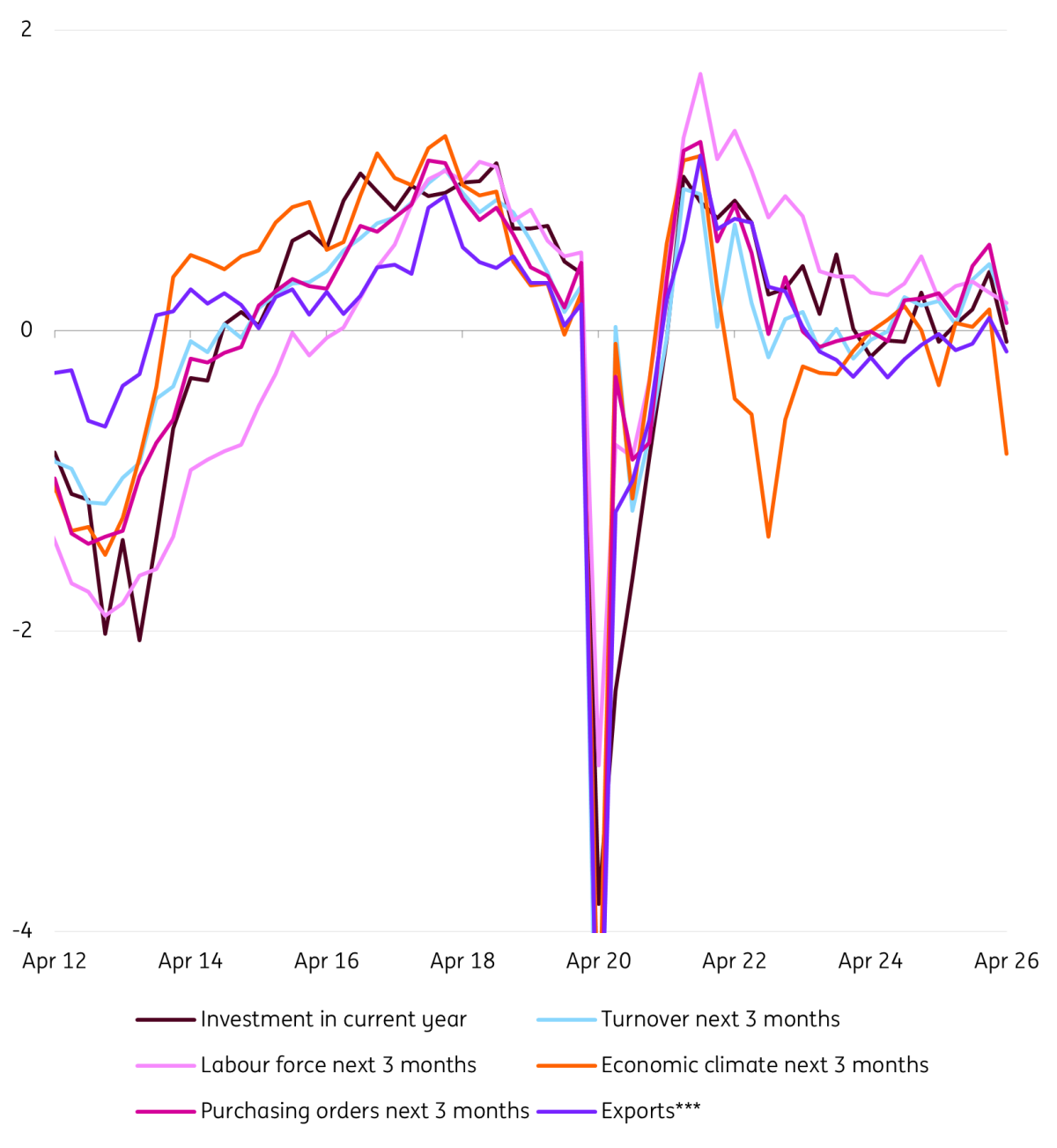

Divergence in own outlook vs. wider outlook

The quarterly business cycle survey among Dutch firms in the entire business economy by Statistics Netherlands and partners from April – the first survey since the start of the war in Iran – suggested considerably more pessimism about the economy at large. The survey also showed only a slight decline in firms' confidence in their own outlook. Most significant for the expectation of their own situation is a fall in purchasing orders. Turnover, employment, export and investment expectations have deteriorated only to a mild extent since the start of the Iran war and remain (albeit slightly) very close to their long-term averages. Firms’ assessment of their competitive position even improved. Perhaps Asia suffers more from disrupted energy flows originating from the Gulf.

While Dutch businesses became much more pessimistic about the economic climate, the expectations of their own situation has deteriorated much less

Normalised indicator* for the development over the next three months (only for investments in the current year), according to businesses** based on a quarterly survey

Investment neither plummeting nor buoyant

Although it was interesting to see that investment expectations of firms only fell a little, our forecast for capital expenditures was already at a subdued level. The expenditures are hindered by geopolitical tensions, structural constraints like nitrogen emission restrictions, electricity grid congestion, and increased competition (e.g. China).

Public (housing and defence) investment is rising though, while structural factors such as population ageing push healthcare spending higher, is helping to keep economic growth going. Planned austerity measures to accommodate higher defence spending won’t take effect before 2027 and have so far received little support. Most notably, the proposed increase in the statutory pension age was rejected. That means that public spending remains a boost to GDP growth this year, albeit less so than in 2025, while uncertainty about the fiscal drag in 2027 remains.

Downbeat consumer not in lowest gear

Despite some looming tax increases that should finance higher defence spending next year, Dutch households’ financial position on average remains decent so far, despite rising inflation. Wage growth is still high (4.2% YoY in May) and unemployment fell (3.9% in April), containing the risk of extreme precautionary behaviour. This might explain why consumption hasn’t really collapsed, despite low consumer confidence and higher inflation. Domestic consumption volumes were still 1% up YoY in April, from 0.9% in March. Nevertheless, we expect the savings rate to remain high going forward, as real income developments deteriorate amidst a low-confidence environment.

Unchanged outlook with risks remaining

All in all, it still looks like Dutch GDP growth could be higher in 2Q26 than in 1Q26. We had that already pencilled into our forecast. So, the Dutch economy still seems to continue to grow at a below-normal pace in the current and upcoming quarter, leading to a mediocre 1.0% GDP growth in 2026 after a solid 1.8% in 2025. With low consumer confidence, uncertainty about the situation in the Gulf region and lower (price) momentum in the housing market, risks to the outlook remain, but currently, there are still no clear signs of a serious recession in the Netherlands.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more