A reduction in Czech financing needs, but risks remain

- 4 April 2022

- Czech Republic

The Czech government has approved a lower deficit, implying lower financing needs, but risks persist. We expect continued strong CZGB supply in April and May. MinFin faces unusually high euro financing needs

We expect a lower general government deficit

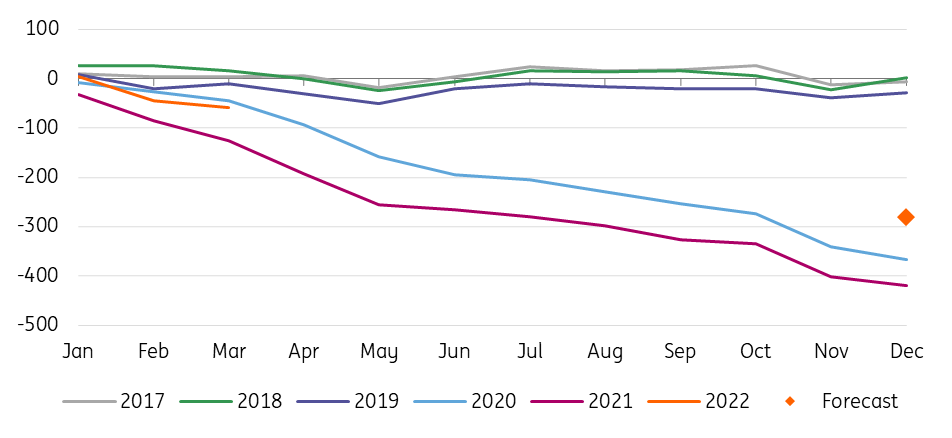

There's a positive surprise in the latest figures on the Czech budget deficit which reached CZK59.1bn in the first three months of the year. Remember, this includes results from March which was already impacted by the Ukraine-Russia war. And there could be more changes to come despite a new state draft budget having been approved a few weeks ago which indicates a budget deficit of CZK280bn, which is 4.8% of GDP. The government will introduce this in the second half of the year given the ongoing Ukrainian crisis and higher energy prices, probably along with a draft budget for 2023.

However, the discussion so far has not shown any measures that would significantly change the fiscal policy narrative in the Czech Republic. Given that it has been the practice over the last decade for the state budget to end with a better result than the government had anticipated, for now, our forecast remains unchanged in line with the current proposals, i.e. CZK280bn.

Given the positive performance of other sectors, the general government deficit should thus be around 4% of GDP for this year. For 2023 and 2024, MinFin indicates a state budget deficit of CZK270bn and CZK250bn respectively, which is the first official indication we've had for 2023 for some time. However, we believe the government will move faster to consolidate public finances. For the coming years, we expect a CZK200bn and CZK150bn state budget deficit, which should result in a general government deficit of 2.9% and 2.0% of GDP.

Czech state budget (CZKbn)

Lower Czech Government Bond supply than planned, but risks remain

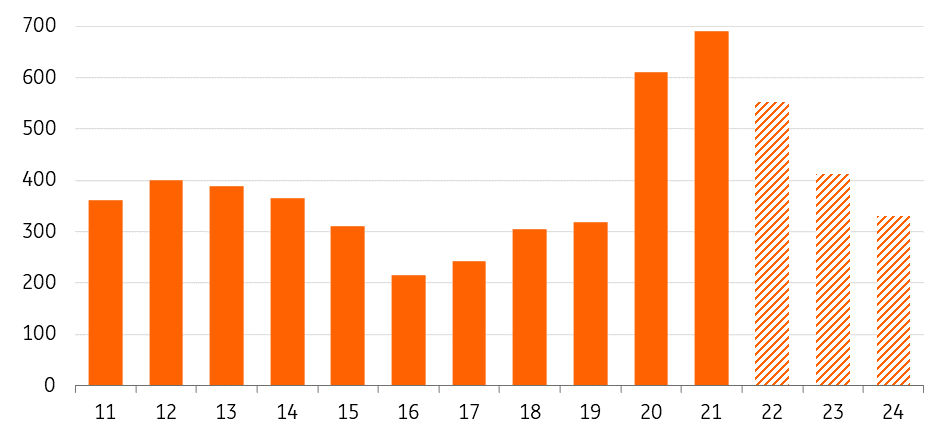

On Friday, MinFin published an update of its funding strategy based on the approved state budget adjustments. As expected, this change has moved the projections of financing needs to the level of our forecast, which is CZK552.1bn this year. According to our calculations, MinFin has secured about 27.7% of this amount in Q1, which is in line with the usual frontloading in the first half of the year. We expect CZGB supply to remain strong during April (the issuance calendar indicates up to CZK17bn in the primary auction) and May. Moreover, we can expect higher MinFin activity on the secondary market given the rich portfolio (mainly CZGB 1.75/32 and CZGB 3.50/35).

On the other hand, market demand has fallen below the long-term average in recent auctions, leading MinFin to shorten the maturity of the offered bonds. Thus, bonds from the 5-10y bucket are coming to the market for the first time in a long while. Given the monetary policy outlook, MinFin is trying to spread the CZGB supply into the 2H22 through a T-bills issuance. For 2023 and 2024, we expect financing needs of CZK412.3bn (MinFin: CZK482.3bn) and CZK329.9bn (MinFin: CZK379.9bn).

Total financing needs (CZKbn)

CZGBs in euros is the main instrument of foreign currency financing

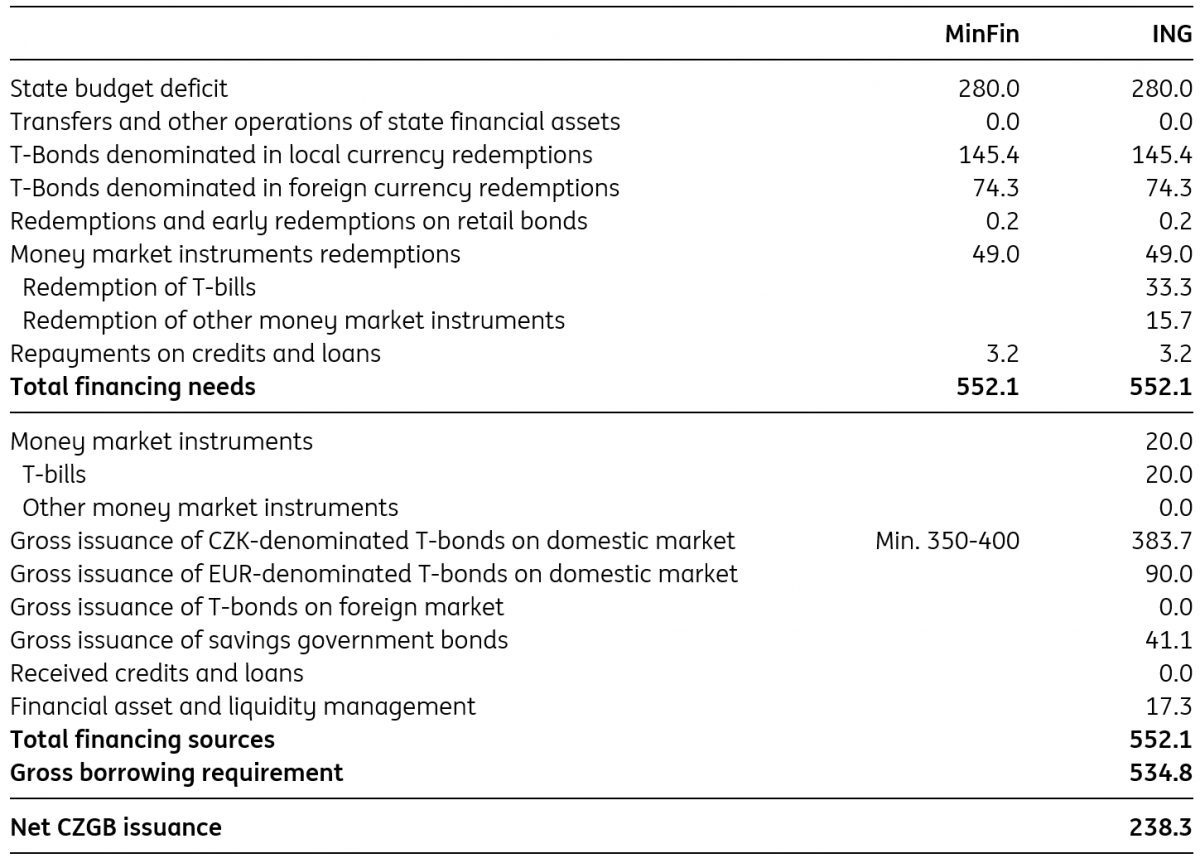

This year, MinFin faces unusually high euro financing needs totalling EUR3.4bn, of which EUR2.75bn is a Eurobond redemption and EUR0.64bn a money-market loan. According to the ministry, the loan has already been repaid. Given the drawdown of supranational loans in the past year, it is difficult to estimate how much of the euro needs remain to be covered.

However, MinFin can be expected to prefer euro-denominated CZGBs issued under local law. Recently, this became ECB eligible after two years of negotiations, which should increase demand from foreign investors. This instrument was introduced in 2019 and has always met sufficient demand so far, but the volume offered has only been in the hundreds of millions of euros. In addition, MinFin also mentions the possibility of issuing T-bills denominated in euros in its strategy. We see the issuance of a traditional Eurobond as unlikely at this point.

Financing needs for 2022 (CZKbn)

Market view

The Czech National Bank's hawkish meeting last week indicates that we are not yet at the peak of the tightening cycle and further rate hikes will come soon. So market expectations are rising massively, giving room for CZGB yields to move even higher. That said, we believe CZGBs are closest to the peak in the region. Asset spreads have tightened massively over the past week due to the move in the IRS curve. Given the continued high supply of CZGBs in the coming weeks and yields catching up with the IRS, the asset spread should widen again.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more