Czech Republic: Higher needs but net issuance unchanged

- 16 January 2023

- Czech Republic

We forecast a better state budget result than expected by MinFin. The financing needs are higher for this year, but the net CZGBs issuance is roughly the same. We expect issuance to concentrate at the long end of the curve. Eur needs are unusually high, which MinFin will cover with a combination of sources. Rating downgrade risk is lower but still remains

Fiscal policy: Better picture than MinFin expects, as usual

The state budget for last year ended with a deficit of CZK360bn, which was CZK15bn better than expected by the Ministry of Finance (MinFin) and closer to our forecast. The detail of the result gives us two takeaways for this year: (1) MinFin has again confirmed our assumption that it is unable to spend the planned expenditure and also is underestimating tax revenues, (2) MinFin failed to draw CZK45bn from EU funds, which should be compensated this year.

Overall, the pattern of a better state budget outcome than MinFin forecasts remains. We expect CZK270bn for this year, while MinFin's plan is CZK295bn. In addition, we see downside risks given the drawdown of EU fund allocations from last year. At the same time, we retain a bias that tax revenues should be higher than MinFin expects mainly due to inflationary reasons. Other sectors of the public finances are expected to remain in surplus, improving the overall public finance picture. The general government balance is thus expected to improve from 4.6% last year to 3.2% of GDP this year according to our forecast.

State budget development and 2023 forecasts

Higher needs but CZGBs net issuance unchanged

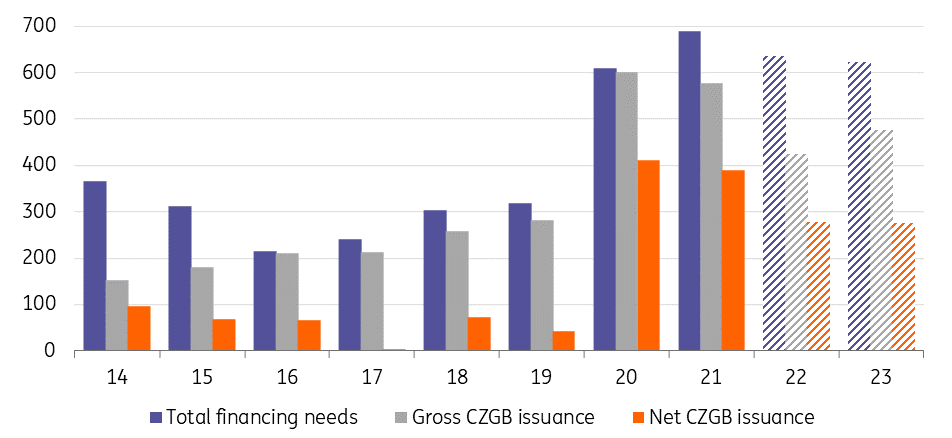

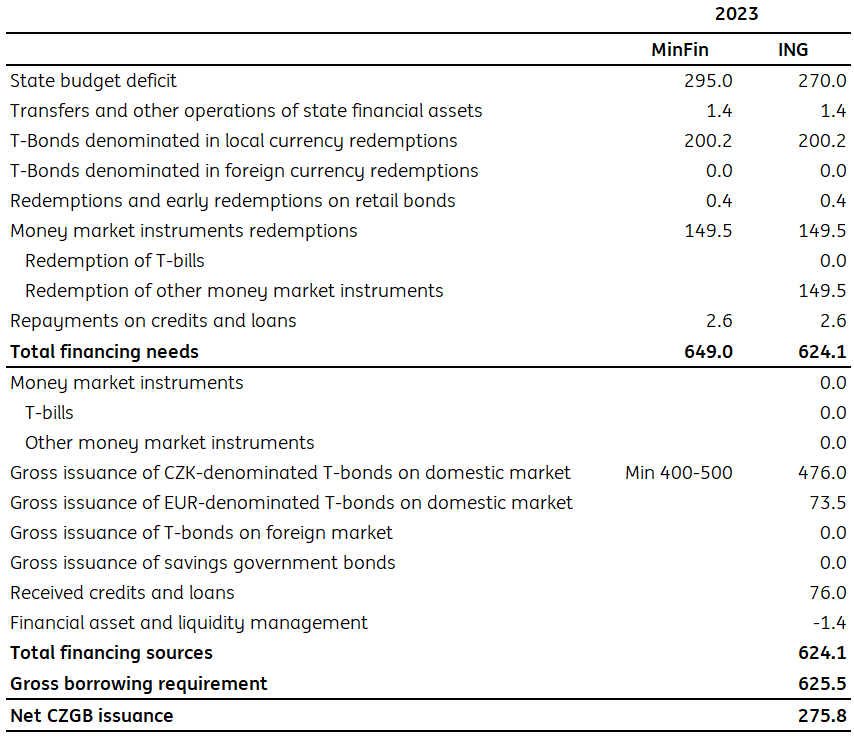

Financing needs amounted to CZK635.6bn (8.6% of GDP) last year, of which CZK424.3bn was financed through the issuance of Czech government bonds (CZGBs). For this year, MinFin expects an increase in financing needs to CZK649bn (8.7% of GDP), and we expect lower needs of CZK624bn (8.4% of GDP) due to a lower forecast of the state budget deficit. Gross CZGBs issuance is projected by MinFin in the range of CZK400-500bn, we expect CZK476bn, which would imply a year-on-year increase of 12.3%. However, there is also a significant year-on-year increase in the volume of CZK200.2bn of bond redemptions, which implies essentially flat net CZGB issuance at CZK275.8bn this year compared to last year.

Total financing needs and CZGBs issuance (CZKbn)

Two CZGBs are maturing this year, CZK88.3bn in April and CZK118.2bn in October. The first auction this year confirmed that demand is sufficient and the market has no problem with lower yields. Combined with the cash buffer, we think MinFin is in a comfortable position to spread the CZGBs issuance over the year. Moreover, MinFin expects the Czech National Bank (CNB) rate cuts in the fourth quarter, in its latest forecast. While the normal pattern has been frontloading in the first quarter, and last year we saw unusually high supply in the third quarter, we expect a more even spread of issuance this year. However, if conditions are favourable for MinFin, the practice of larger-than-planned auctions can be expected.

In terms of parameters, the average maturity of CZGBs is currently only slightly below MinFin's 6.5-year target. If market conditions allow, we expect MinFin to focus on issuance at the long end to leverage the curve inversion. We believe issuance will be concentrated in CZGB 5.50/28 and 5.00/30, which combined can cover CZK140bn of needs within their issuance limit. Overall, the current five-year maturity issuance limits could cover this year's total issuance, but given the lower demand for super-long bonds, we expect MinFin to introduce new issues later this year.

Financing needs for 2023 (CZKbn)

Unusually high EUR needs financed through CZGBs

An interesting topic this year will be the euro's financial needs, which are unusually high for the Czech Republic. We identify that CZK140.5bn of the CZK624bn financing needs are euro-denominated, roughly €6.1bn. These, in our view, will be financed by MinFin through a combination of euro-denominated CZGBs (€3.0bn), repayments of euro-denominated loans to energy suppliers (€1.9bn) and loans from supranational institutions (€1.2bn). In addition, the mismatch between funding maturities will now be newly covered by euro-denominated T-bills instead of money market loans.

For now, MinFin has two euro-denominated CZGBs in the market. The longer of the two, CZGB 0.00/27, still has a free issuance limit, but to cover the entire need, we think MinFin will issue a new bond with a longer maturity to build the EUR curve. In addition, these bonds have become ECB eligible, so we believe this will be the preferred route over conventional Eurobonds.

CZGBs maturity calendar (CZKbn)

Technicals: Risk of rating downgrade is lower

In our view, the downgrade risk that we have highlighted in the past is gradually diminishing due to the calming of energy prices, government measures to protect households and industry, and a slightly better fiscal picture. In addition, the CEE region's rating review calendar is favourable for the Czech Republic given the first review only in March (Fitch), when we could already hear more details from MinFin regarding the planned consolidation of public finances for the coming years. However, we still see a risk of a possible downgrade, especially for the Fitch rating review.

In the GBI-EM space, essentially all eligible bonds except CZGB 1.95/37 and 4.85/57 are already included in the index at the moment. Perhaps at the end of the year due to a shift within the maturity buckets, we will see a chance for CZGB 1.95/37 to be included. On the other hand, we expect CZGB 0.45/23 to lose the GBI-EM title in March and 5.70/2024 in October this year.

The share of foreign holders of CZGBs fell to 26.5% last November, continuing a long-term gradual trend. Even so, the ratio remains the highest in the CEE region. Nevertheless, in nominal terms, the holdings of CZGBs by foreign entities remain slightly above CZK700bn. The decline in the ratio resulted from rising holdings by the local banking sector, which increased by 26% to CZK1101bn between January and November last year alone.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more