Czech producer prices rise as agriculture drives food costs higher

Czech production prices accelerated across all major sectors, with firm pricing in agriculture set to drive consumer price tags in the food segment over the year ahead. Higher energy bills drove price dynamics in industry, while tough competition made it difficult to pass cost increases through to end prices

Energy prices likely to bite into margins

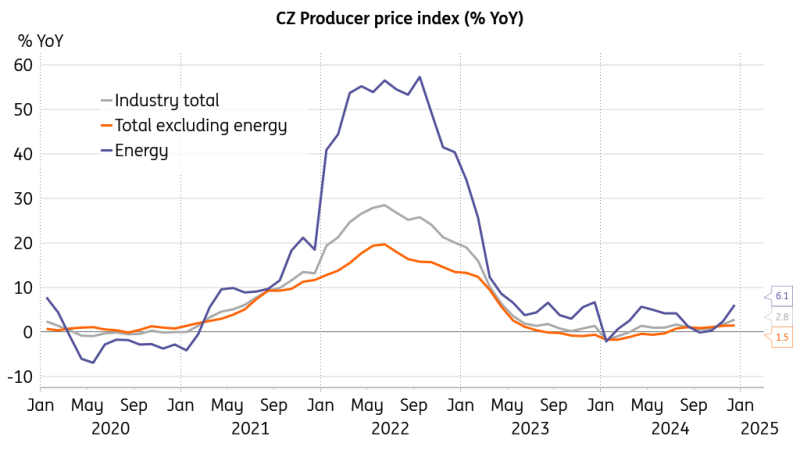

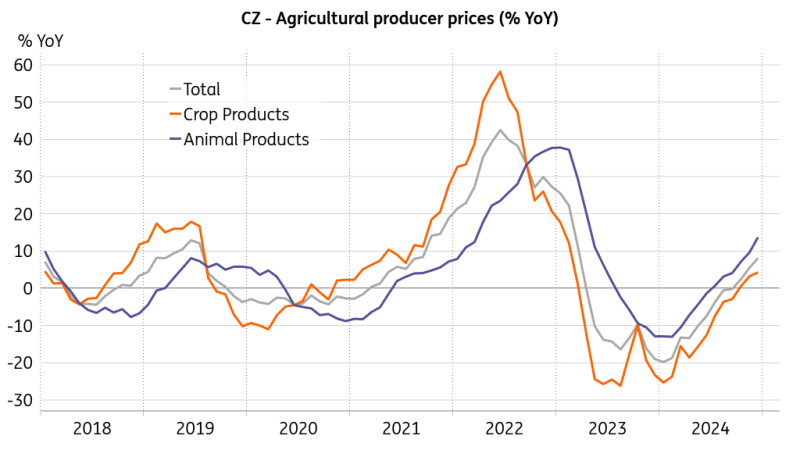

Czech industrial producer prices accelerated to 2.8% year-on-year in December, adding 0.6% month-on-month. Agricultural producer prices rose to 8.1% YoY, increasing 1.2% MoM. Construction prices were 2.6% above where they were in December a year prior, and prices of market services for businesses were up by 3.8% YoY. Both added 0.1% in monthly terms.

Monthly price gains in industry were mainly driven by the 3.4% MoM price increase in the section of electricity, gas, and steam, linked to more potent natural gas prices and a weaker koruna against the dollar throughout the last quarter of the year. Prices in food manufacturing added 0.3% MoM, with notable price gains for dairy products, oils, and fats.

Energy prices start to propel production costs

When assessed by major industry group, prices of energy rose by 6.1% YoY, those of capital goods by 3.0% YoY, and those of non-durable goods by 1.8% YoY. Industrial producer prices, excluding energy, added 1.5% YoY. Tough competition in manufacturing – driven by weak demand across Europe amid challenging conditions in the automotive sector – does not allow for producers to pass on the rising energy costs on to final prices.

That, in turn, bites into producers' margins and undermines their ability to continue with solid wage increases, representing a clear threat to the Czech economic rebound so far driven by consumer spending. Predicting the right timing here is challenging, as firms tend to support experienced and skilled workers even when faced with temporary difficulties. However, we'd argue that temporary is no longer the proper adjective for the Czech industrial malaise, as industrial output has stagnated since 2018 and has found itself on a mild downward trend for over a year.

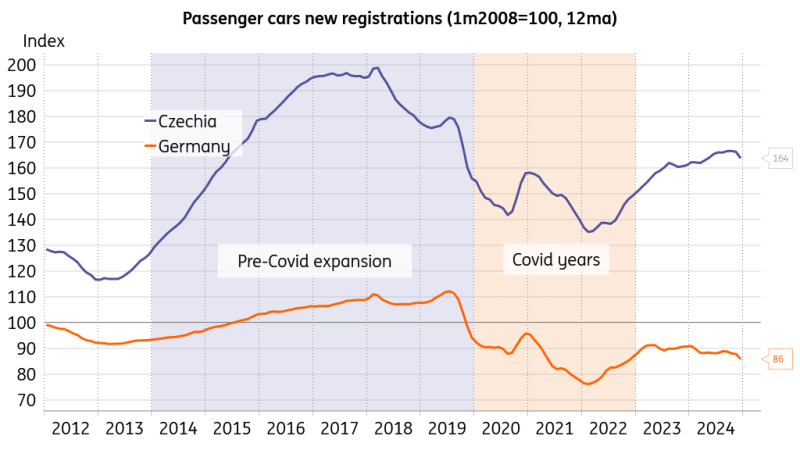

New car registrations weaken

When it comes to the dull European automotive sector, we should also consider the role of the global consumer: Chinese customers are unlikely to invest their money in vehicles produced somewhere that exists as a fierce ideological rival of their home country – especially if there is a qualitatively comparable and cheaper option produced domestically. European car manufacturers across the region now find themselves in a challenging situation, as they're also unable to offer European customers exactly what they're after.

Food prices to drive consumer inflation this year

Pricing in agriculture was mainly driven by accelerating prices of animal production, which picked up by 13.7% YoY and 4.2% MoM. At the same time, the price dynamic in animal production represents the more persistent part of the food segment, likely driving the food price tags for consumers in the coming months and quarters. Once again, higher energy prices make all food production more expensive, starting with higher costs for fertilisers and ending with higher energy bills for keeping end products cool.

Price dynamics in agriculture heats up

Overall, the acceleration of agricultural producer prices will feed into food prices for consumers, with a three to six-month lag for a full pass-through of costs. This poses an upward risk for consumer inflation this year. Pricing in business services strengthened for a third consecutive month, suggesting a continuation in price growth inertia in this sector. With European industry remaining under pressure and lame demand from key European trading partners, rising energy bills are definitely not good news for the Czech industrial base, especially amid conditions of raging global competition.

Rapid chess

When it comes to European and Czech competitiveness, all input for production seems to grow more and more expensive than in other major industrial economies, e.g., energy, materials, and labour. Usually, advanced economies enjoy an edge in their technological and institutional setups in a way that a) some areas of critical input – such as labour – are employed more efficiently, or b) some of these inputs are significantly cheaper, such as energy. Europe's combined technology and institutional setup means that all three production components – energy, materials, and labour – are far more expensive than those of its competitors. At the same time, the advantages of higher quality, innovative features, attractive design, and excellent customer service are increasingly outweighed by these higher costs.

How can rising production costs be reconciled with competitiveness when the relative advantages in quality, innovation, and design are rapidly diminishing? Well, something has got to give. A more pessimistic view could be that Europe is poised to become an economy characterised by a declining income in the coming years – particularly when compared with its competitors In this respect, drawing up medium and long-run projections for European economies can be a challenging and dismal business.

And guess what happens with Europe's ability to project its interests on the fast-changing geopolitical chessboard? Even if Europe were to find common ground in terms of revamping its economic growth strategy when looking forward, it’s the sea of time needed to push things through that makes its efforts in vain. The global game played nowadays is rapid chess, not correspondence chess. If Europe doesn't awaken from its industrial lethargy and start to move faster soon, then we'd be tempted to reiterate the famous vanitas vanitatum et omnia vanitas – vanity of vanities, all is vanity.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article