Czech PMI weakens but does not flip into panic mode

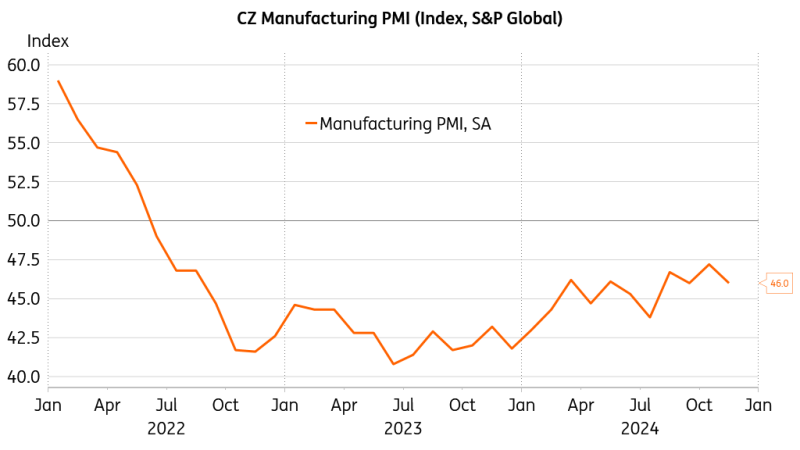

The manufacturing PMI dropped deeper into the contractionary zone in November, coming in below market expectations. The weakness in output and confidence reflected infirm foreign demand. At the same time, the reduction in jobs slowed substantially, providing some hope that the industrial malaise may be coming to an end

Industrial output drops, but layoffs slow down markedly

The Czech manufacturing PMI dropped to 46 points in November, coming in weaker than market participants expected. A pronounced decline in both production and new orders dented business confidence, which dropped to a 10-month low. Bleak foreign demand, structural issues in the European automotive sector, and challenges to the German economic model were the main issues reported in the survey.

PMI still below the expansion watermark

New export orders fell at the fastest pace since July due to weak demand from key export markets, with manufacturers responding by reducing production further. The pace of decline was more substantial than in the previous survey period, yet the second slowest since March 2023. At the same time, layoffs have eased to the lowest levels observed since March, even as business confidence slipped to its weakest point since the start of the year. On the pricing front, producers registered a soft increase in overall costs, yet this was not passed on to customers. In fact, selling prices declined again amid bleak demand and increased price competition.

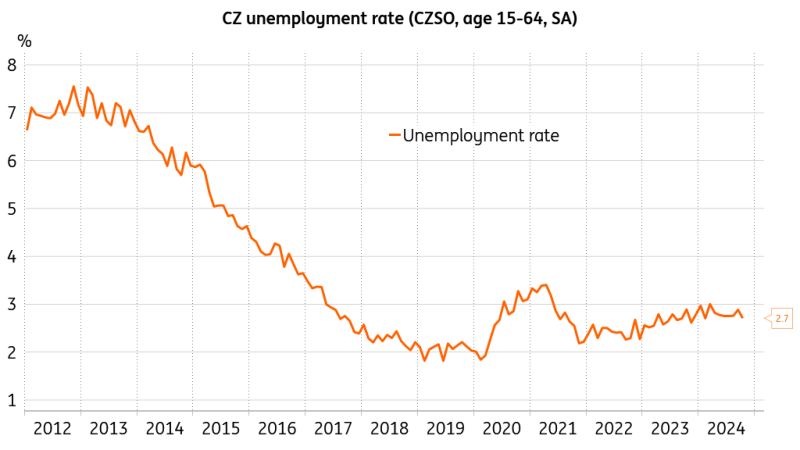

The unemployment rate softens in a still-tight labour market

According to the latest CZSO survey, the Czech unemployment rate softened to 2.7% in October, shedding 0.2ppt from the previous reading. The employment rate reached 75% in October, and the economic activity rate reached 77.1%, remaining broadly stable since mid-last year.

Labour market tightness persists

We see the labour market as remaining tight, with some duality between the skilled and unskilled market segments. The skilled labour force remains a scarce resource, while recent layoffs in industry were predominantly skewed towards low-skilled workers. However, the recovery in the construction sector presents a hopeful prospect, as it could partially offset the symptoms of the protracted industrial underperformance and absorb some of the free labour force.

Underinvestment is a medium-term challenge

Overall, the November manufacturing PMI corrected the previous uptick, with industry factoring in more uncertainty regarding potential tariffs from the upcoming US administration and reflecting the inability of the German economy to hit bottom. Indeed, bleak demand from the main trading partner is a serious issue for the export-orientated Czech industrial base. At the same time, we do not foresee the situation escalating into panic mode. Additionally, the Czech automotive sector appears to be handling the widespread industry disruptions in Europe relatively well.

As for anecdotal evidence, the Skoda unions are demanding a pay rise that exceeds inflation and an increase in bonuses for each employee, despite the challenging situation at VW. The unions' reasoning highlights Skoda's good financial results within the group, with its 1Q-3Q profit being up more than a third over the preceding year. At the same time, Skoda's operating margin reached 8.3%, while Spain's Seat makes half of that, and the leading brand, VW, makes a quarter.

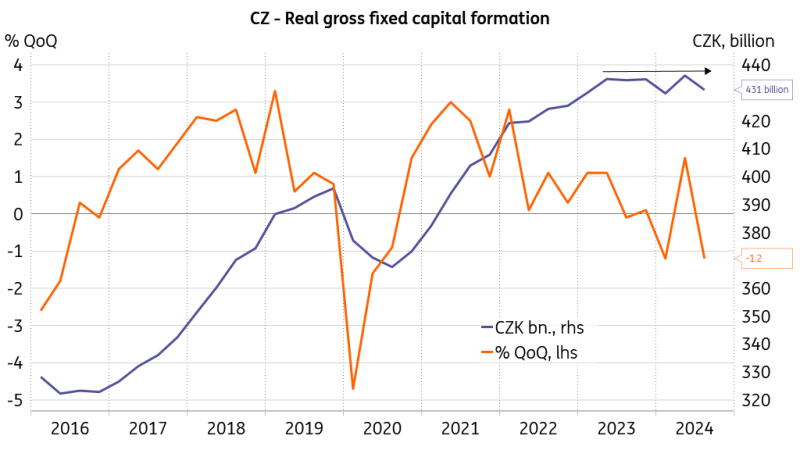

Investment activity has stalled

That said, economy-wide fixed capital formation in the third quarter dropped to levels observed in early 2023, meaning that progress in fixed investment has been non-existent for over a year and a half. That is just not good news for an industry-heavy and export-oriented economy. The question is whether high borrowing costs or structural issues, amid elevated uncertainty about the future of European industry, are to blame. If it's the former, reducing interest rates would help. If it's the latter, other barriers hindering economic expansion and stifling investment incentives must be addressed.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article