Czech National Bank review: Time for a looser policy

- 8 February 2024

- Czech Republic

The CNB has accelerated the pace of rate cutting to 50bp, which we assume will be the pace for the next meetings as well. The central bank's new forecast shows a weaker economy and lower rates, while inflation is expected to return to the 2% target soon. However, the terminal rate may be higher than we thought

50bp rate cut and dovish forecast delivered

The Czech National Bank cut rates by 50bp to 6.25% today. This means an acceleration in the pace of rate cuts from 25bp in December, when the cutting cycle began. Six members voted for the decision and one member voted for a 75bp rate cut. We assume it was Tomas Holub.

| 6.25% |

50bp rate cutLower vs market consensus |

| As expected | |

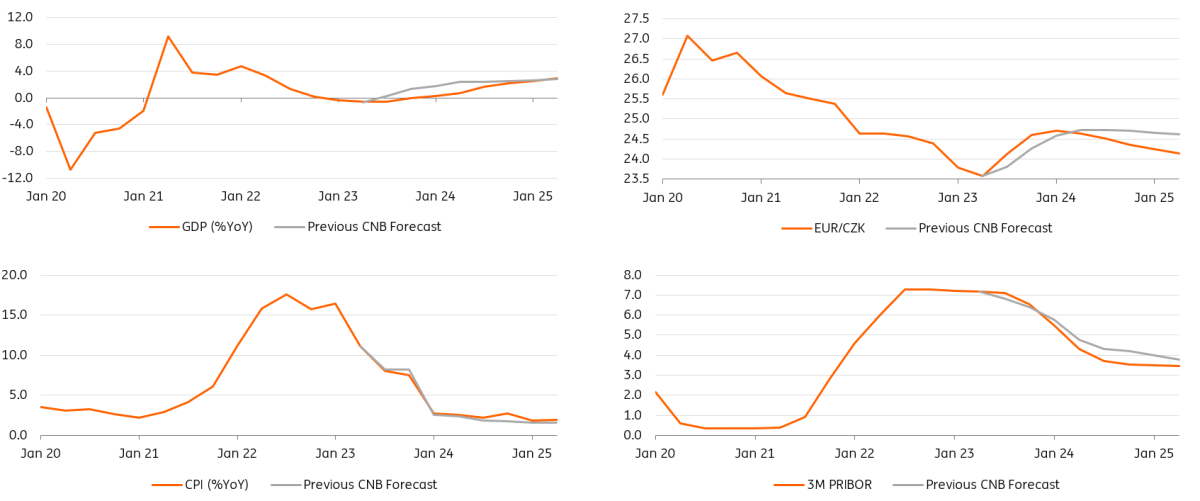

The CNB's new forecasts brought a few changes; the direction is in line with our expectations but the dynamics are somehow higher than we expected. We see the biggest surprise in GDP, which has fallen from 1.2% to 0.6% this year compared to the November forecast, while the CNB was already the most pessimistic on the market. Also, the rate path has moved significantly lower, almost 1pp at the end of the horizon with a terminal rate of around 2.50% for 3M PRIBOR. On the other hand, EURCZK is unchanged in the near term and the inflation profile is almost unchanged. The CNB expects inflation of 3.0% year-on-year for January, which in our view has room for a surprise to the downside toward 2.7% YoY, which is our forecast along with more downside risk.

CNB forecast change

No change in our forecast, 50bp for the next meetings

In our view, the press conference confirmed that the CNB is not interested in GDP and surprisingly FX is not as much of a topic as we thought. The only point of focus is and will be spot inflation, which we think will define the next steps. The presser showed the CNB's confidence in its current actions and confidence that inflation will come down, but we didn't see any indication of a willingness to speed up the pace again later today. We also saw pushback against the baseline scenario, as always, and also a view that the terminal rate is higher, possibly above 3%, which is an anchor for the CNB model at the moment.

So for now we leave our forecast unchanged with 50bp cuts for the next meetings with the rate at 4% at year-end. If inflation surprises significantly to the downside, below 2.5%, and EUR/CZK returns below 25.00, which is our forecast, we may see a chance for an acceleration later, but not for the upcoming meetings.

EUR/CZK moved slightly above 25.200 after the decision and press conference, which was our target for the 50bp rate cut scenario from our CNB preview. However, we can expect that on Friday the rates will still look for their new levels, which may push EUR/CZK to 25.300. However, as we mentioned earlier, we believe the pair will peak soon. January inflation will be published next week, which we believe may be the last reason for rates to hit the limit of priced rate cuts at the short end of the curve. Moreover, we believe that the market positioning was already strongly short before the meeting. On the other hand, the situation in the economy should turn for the better, including a positive current account balance and a drop in rates abroad, supporting a stronger CZK. Therefore, we expect EUR/CZK to return below 25.000 later.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more