Czech National Bank Review: The dove dressed as a hawk

- 21 December 2022

- Czech Republic

As expected, everything remained unchanged today. The central bank is in a comfortable situation with inflation below its forecast and the koruna far below intervention levels. January inflation may bring some headaches, but it should not be enough to hike rates

| 7.00% |

CNB's key policy rateNo change |

| As expected | |

No change in rates and FX regime

As expected, the CNB left interest rates unchanged at today's meeting. The central bank also confirmed that it would continue to prevent excessive fluctuations in the koruna. Given that the new forecast will not be published until February, today's meeting only confirmed the dovish majority in the board. As last time, five board members voted for this decision, with two members voting for a 50 basis point rate hike.

During the press conference, Governor Michl reiterated that the board was discussing a rate hike or rate stability today. Neither rate cuts nor the timing of future rate cuts was the subject of today's meeting. The governor also reminded that the CNB still expects inflation to approach 20% year-on-year in January due to the change in the effect of government measures, which should be the peak of inflation, and expects a slowdown thereafter. He also cited the sharp drop in domestic demand, the slowdown in the credit market and the decline in real wages as evidence of easing demand pressures on inflation. The list of risks has seen only cosmetic changes and risks remain significant in both directions.

The Bank Board is ready to react appropriately to any materialisation of the risks of the forecast

The January number will be a restart of the inflation story

From our perspective, nothing much has changed in the picture after today's meeting. The board has been trying to maintain hawkish expectations for longer, but the market instead is more focused on the global picture. In line with the CNB, we expect inflation to rise further in the next two months, but we do not expect it to reach 20% YoY. The main reason for this is our different view on the impact of government measures on CPI. We expect the price cap to have a roughly similar impact to the current saving tariff. Thus, the January re-pricing will be decisive and may surprise massively to the upside. However, in the base case scenario, we expect numbers close to 18% YoY. This should be enough for the CNB to maintain its current rhetoric and not have to do anything. But, given our expectation of rising inflation across the region, the turn of January/February may be a reminder to the market that inflation is still a problem in the region.

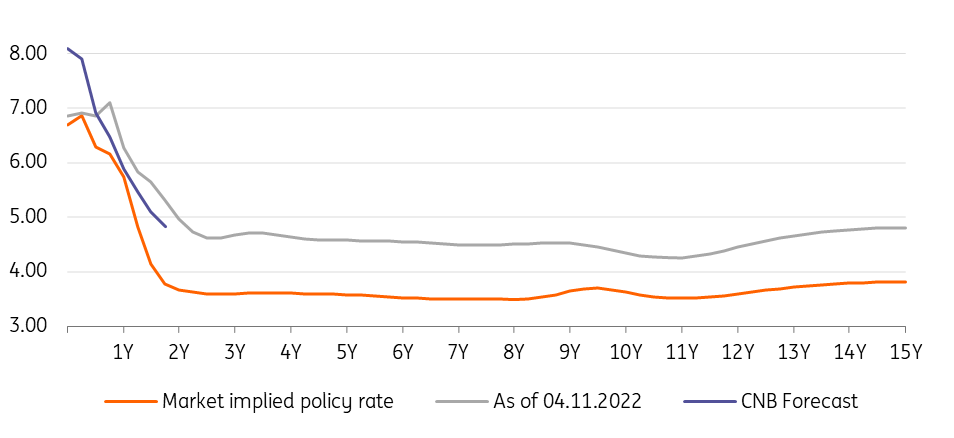

Market expectations have moved significantly since the last meeting

What to expect in rates and FX markets

The market has taken a significantly more dovish view recently and today's CNB meeting didn't change that much. Although market rates have already bounced off the bottom last week, it is still pricing in an aggressive rate cutting trajectory. At the end of next year, the market expects rates to be at 6%, which is close to our forecast. But we expect the path to that won't be straightforward, and the re-peak in inflation in January will make it a bumpy ride. Therefore, in our view, it is too early for rate receivers at the short end of the curve and at the same time the long end should be supported upwards by core rates for a while longer. Thus, overall, we expect the IRS curve higher without a significant change in slope in the coming weeks.

The koruna is hitting its strongest levels in eleven years. At the same time, we last saw CNB activity in the market in September. Overall, the koruna is playing into the central bank's hands and we expect nothing to change in the near term. In our view, the current rally is mainly driven by foreign conditions in the form of friendly EUR/USD levels and mainly falling gas prices. In addition, significant short positioning in the market in the past has supported the current rally. Overall, however, we expect this to be a temporary spike and the koruna to return to 24.30 EUR/CZK, but this is still far from CNB intervention levels.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more