Czech National Bank review: Staying on the safe side

- 2 November 2023

- Czech Republic

The CNB decided to wait for the start of the cutting cycle due to concerns about the anchoring of inflation expectations, high core inflation in its forecast and possible spillover into wage negotiations. The December meeting is live, but we slightly prefer the first quarter of next year. Economic data will be key in coming months

Rates remain unchanged for a little longer

The CNB Board decided today to leave rates unchanged despite expectations of a first rate cut. Five board members voted for unchanged rates at 7.00% and two voted for a 25bp rate cut. During the press conference, Governor Michl justified today's decision on the continued risk of unanchored inflation expectations, which may be threatened by the rise in October inflation due to the comparative base from last year. This could seep into wage negotiations and threaten the January revaluation, according to the CNB. At the same time, the board still doesn't like to see core inflation near 3% next year. So overall, it wants to wait for more numbers from the economy and evaluate at the December meeting, which the governor said could be another decision on whether to leave rates unchanged or start a cutting cycle.

| 7.00% |

CNB Key rateNo change |

| Higher than expected | |

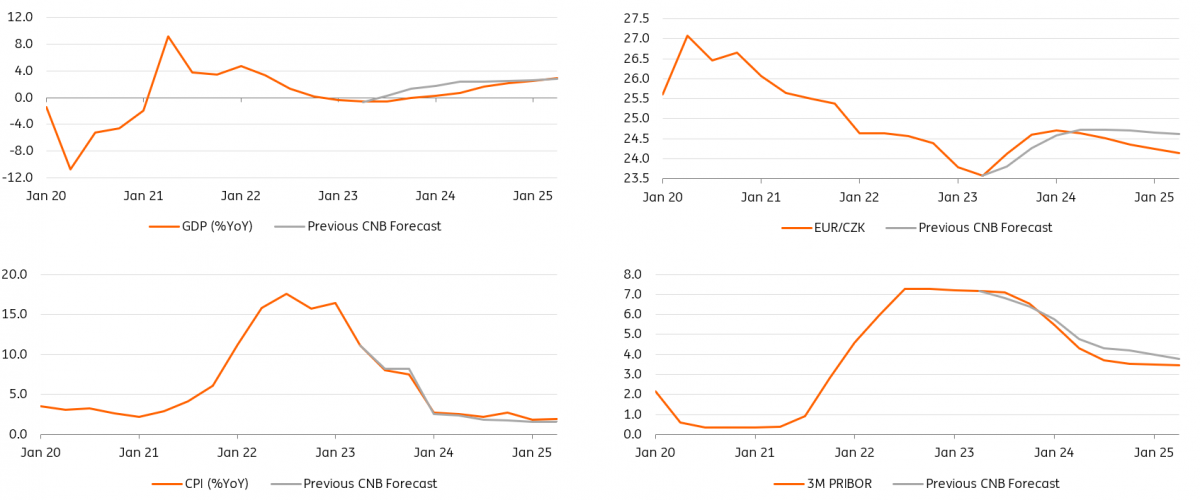

New forecast shows weaker economy and more rate cuts

The new forecast brought most of the changes in line with our expectations. The CNB revised the outlook for GDP down significantly and the recovery was postponed until next year. Headline inflation was revised down slightly for this year but raised a bit for next year. The outlook for core inflation will be released later, but the governor has repeatedly mentioned that the outlook still assumes around 3% on average next year. The EUR/CZK path has been moved up, but slightly less than we had expected. 3M PRIBOR has been revised up by a spot level from the August forecast, implying now the start of rate cuts in the fourth quarter of this year and a larger size of cuts next year. For all of next year the profile is 30-65bp lower in the rate path, indicating more than 100bp in cuts in the first and second quarter next year.

New CNB forecasts

First cut depends on data but a delay until next year is likely

Today's CNB meeting did not reveal much about what conditions the board wants to see for the start of the cutting cycle and given the governor's emphasis on higher inflation in the next three prints, we slightly prefer February to December. The new inflation forecast indicates 8.3% for October and levels around 7% in November and December. The last two months seem too low to us, but given the announced energy price cuts, this is not out of the question. So this is likely to be a key indicator looking ahead as to whether or not it will give enough confidence to the board that inflation is under control. Another key question is whether the CNB will move up the date of its February meeting so that it has January inflation in hand for decision-making.

What to expect in FX and rates markets

EUR/CZK jumped after the CNB decision into the 24.400-500 band we mentioned earlier for the unchanged rate scenario after the decision. For now, the interest rate differential does not seem to have changed much after today's meeting, which should not bring further CZK appreciation. On the other hand, the new CNB forecast showed EUR/CZK lower than we expected and the board seems more hawkish. Therefore, we could see EUR/CZK around these levels for the next few days if rates repricing remains roughly at today's levels. However, we expect pressure on a weaker CZK to return soon as weaker economic data will again increase market bets on a CNB rate cut, which should lead EUR/CZK to the 24.700-24.800 range later.

In the rates space, despite the high volatility, the market did not change much at the end of the day. The very short end of the curve (FRAs) obviously repriced the undelivered rate cut, however the IRS curve over the 3Y horizon ended lower, resulting in a significant flattening of the curve. The market is currently pricing in more than a 150bp in cuts in a six-month horizon, which in the end is not so much given the possible acceleration of the cutting pace after the January inflation release. Even though the CNB didn't deliver today's rate cut, we think the central bank is more likely to catch up with the rate cuts next year rather than the entire trajectory shifting. Therefore, we see room for the curve to go down, especially in the belly and long end.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more