Czech inflation slows down, but less than expected

Czech headline inflation slowed down to 2.8% annually, coming in above market expectations. We think the Czech National Bank is likely to proceed with a rate cut this afternoon, but the potent wage growth, accelerating prices in agriculture, and relatively elevated inflation print will definitely steer the discussion, contributing to a hawkish tone

Food prices strike back

Czech annual inflation softened to 2.8% in January from 3.0% in December. The print came in above market expectations of 2.6%, mainly due to a more substantial increase in food prices. In contrast, price growth in the service sector slowed down in annual terms, suggesting a relatively stable rate of core inflation. Price growth has eased when food and energy are excluded as defined by the CZSO. Energy prices were the main drag on overall price growth, likely driven by lower electricity prices.

In any case, this afternoon's CNB meeting is expected to convey a hawkish message, especially since the proposed 25 basis point cut has become uncertain due to the relatively strong headline inflation figure. We saw the cut as a deal done if January's inflation print came in below 2.7%. Nevertheless, the estimated 2.8% increase in consumer prices might be too potent, although driven by volatile food prices. We will likely see a split vote, with the base rate reduction pushed through by a tight majority.

That said, the CNB forecasting and communication infrastructure is built pretty tightly around the CNB’s breakdown of CPI. There was never much hesitation about that in the building. The challenge lies in accurately reconstructing the breakdown that the CNB wants to see, given the limited scope of the flash estimate. This makes decision-making difficult. It is clear that much of the boost comes from food prices, which can be deemed volatile. At the same time, January's food price hike may only offset the Christmas discounts on food, alcohol, and tobacco. Meanwhile, some accumulated cost pressures in agricultural producer prices are expected to drive pricing in the food segment over the coming quarters.

Industrial output remains weak while construction lifts off

Czech industrial output shed 3.0% year-on-year in real terms in December, while gaining 1.6% from the preceding month. The annual decline in industrial production was mostly linked to the production of motor vehicles but was also affected by the high comparison base from the previous year. The production of electrical equipment, especially automotive components, also lost ground compared to the preceding December.

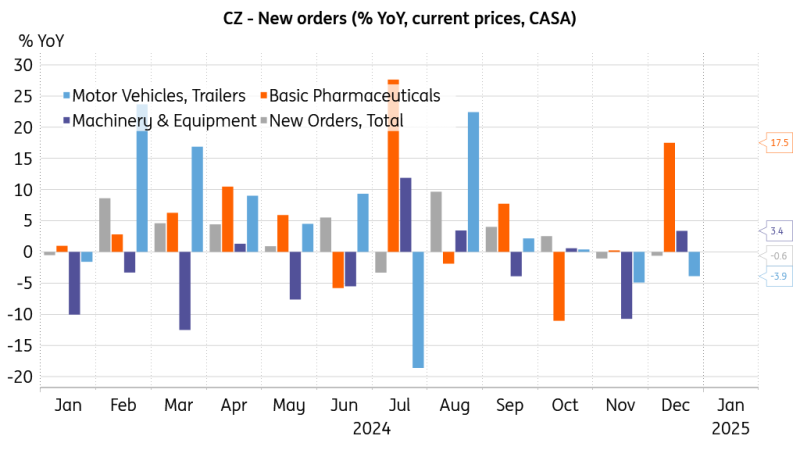

New orders continue to disappoint

The value of new orders at current prices dropped slightly in December compared to the previous year when measured in calendar and seasonally adjusted terms. Similar to the output, the annual decline in the value of new orders was mostly driven by the motor vehicle manufacturing and electrical equipment manufacturing sectors. The average number of registered employees in the industry decreased by 2.0% YoY in December, while the average monthly nominal wage increased to 7.2% YoY.

Construction output rose by 9.7% YoY in December and was 4.5% higher than the previous month. However, 5.7% fewer dwellings were started, and 60.1% fewer dwellings were completed compared to a year ago. The average monthly nominal wage gained 10.3% from the previous December. The rather robust wage increases will also shape today’s discussion at the CNB meeting.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article