Czech inflation on target as food prices drop significantly

Czech annual inflation slowed down in June, returning to target. Consumer prices shed 0.3% from a month earlier, with food and fuel prices contributing most to the drop. The recent inflation print is well below market expectations and the CNB’s spring forecast, opening the door to a continued reduction in the restrictiveness of monetary policy

A pronounced fall in agricultural producer prices kicks in but beware of volatile food prices

The pronounced fall in agricultural producer prices passes through to the final price tags. The food and non-alcoholic beverages section had the most significant negative contribution to annual inflation in June, with prices of many food items in the basket declining by more than 20% from a year earlier. However, food prices tend to be volatile, and the pronounced drop from the previous month might be reversed in the coming months. Therefore, pronounced changes in food prices are usually discounted in the considerations of the Czech National Bank Board. We were aware of the passthrough from the agricultural producer prices, but getting the timing right is challenging in this segment due to changes in margins along the supply chain.

Food prices continue in decline following the prices in agriculture

Price dynamics in services and housing remained rather elevated. Prices in the housing section continued to have the largest impact on the overall annual inflation, with a 7.0% rise in rents and a 4.7% increase in goods and services related to the maintenance of dwellings. Water and electricity charges added more than 10% each from a year earlier. Still, core inflation continued to decelerate to 2.2% recorded in June, which is below the CNB's expectation of 2.6%.

Monetary policy restrictiveness to be reduced further

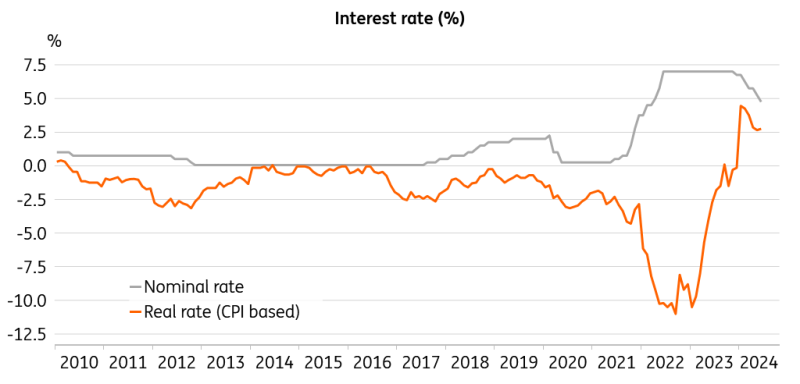

The lower-than-expected headline and core inflation have opened the door to further monetary policy easing. With the real interest rate at 2.75% in June and a mediocre investment performance amid a fragile recovery, the economy appears to be ready for a less restrictive monetary policy stance. This leads us to revise our rate outlook downwards, with the year-end rate projected at 4% and declining to 3.25% by the end of the following year.

Real interest rates remain elevated with inflation on target

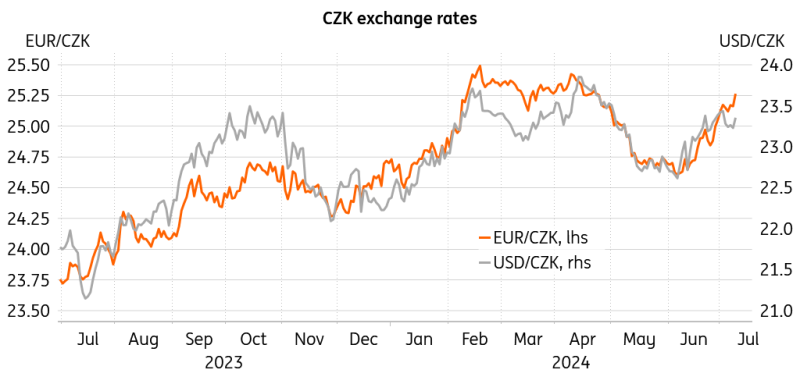

On the other hand, the relatively tight labour market coupled with elevated wage growth warrants some caution looking ahead. The weakening of the Czech koruna, driven by the recent rate cut and lower-than-expected inflation print, will also contribute to the Board's decision at the August meeting. The Board will likely decide between a 25bp and a 50bp reduction to the policy rate, similar to previous meetings. At this stage, we count on a 25bp cut, but we will wait for guidance from decision makers in the coming weeks.

The pace of recovery is the key to the inflation outlook

So, does the low inflation print disqualify the recent discussion about a build-up of inflationary pressures and the need for caution? Not really, as price pressures stemming from elevated nominal wage growth and solid consumer spending are to be assessed as potential future driving forces for consumer inflation. With the CNB being a forward-looking institution, this area will still be watched and taken into consideration. The effect would likely be tangible towards year-end if further nourished by a proper economic rebound. And the pace of an economic recovery will be key for the inflation outlook in the coming months and quarters. A gradual but continued rebound driven also by household spending still represents our baseline scenario. However, economic activity has obviously lost some momentum recently, pointing to cracks in the outlook.

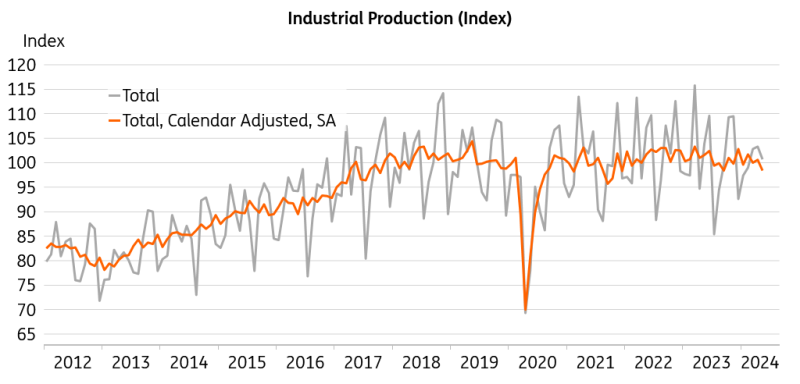

Industry is not picking up - too bad for an export-driven economy

When looking at seasonally adjusted indices, industrial production has not done well in recent months, with subdued foreign demand being the main driver of the malaise. Weak new orders cast a shadow over the industrial performance when looking ahead, representing a significant issue for an export-driven economy. Real retail sales stagnated in the past three months, clearly breaking the upward trend observed since September last year. This brings us to marginally lower our already conservative real GDP growth outlook for this year to 1%, with more doubts on the horizon than a quarter ago.

The preliminary GDP estimate for the second quarter of the year will be published at the end of this month and will shed more light on whether the recovery story goes on or will be revoked. The pace of a pickup in overall economic activity and consumer spending will be key to future price and rate developments. Should the recovery stall, the topic of lofty wages and spending propelling consumer prices is off the table. However, the exchange rate could come under more pressure in such a case, driving imported inflation.

Exchange rate weakening will also shape the next CNB decision

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article