Czech industrial output contracts, yet new orders rebound

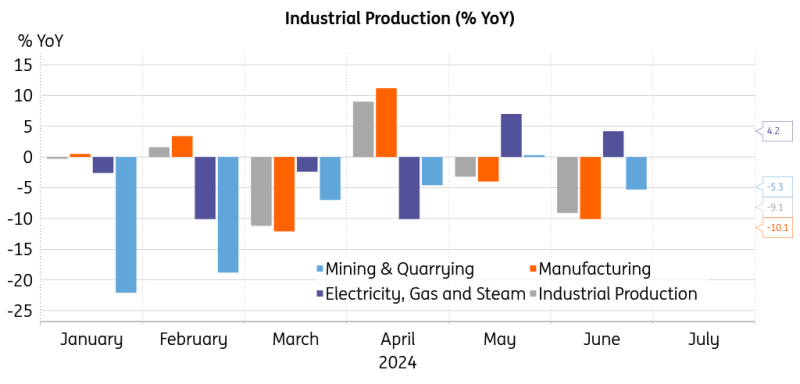

Czech industrial production came in below market expectations, falling 9.1% from a year earlier. However, this was partially due to a high comparison base and more working days in the previous year. The acceleration in new orders suggests some improvement ahead, while average wage growth in industry decelerated

June was not too bad after all, but uncertainty has increased

Czech industrial production dropped 9.1% year-on-year in June, partially due to a high comparison base and more working days from the previous year. The long-term decline in machinery and equipment production continued, along with further weakness in basic metals and metallurgy. In contrast, industrial production in June added 0.7% from the previous month in seasonally adjusted terms.

Industrial output remains under pressure

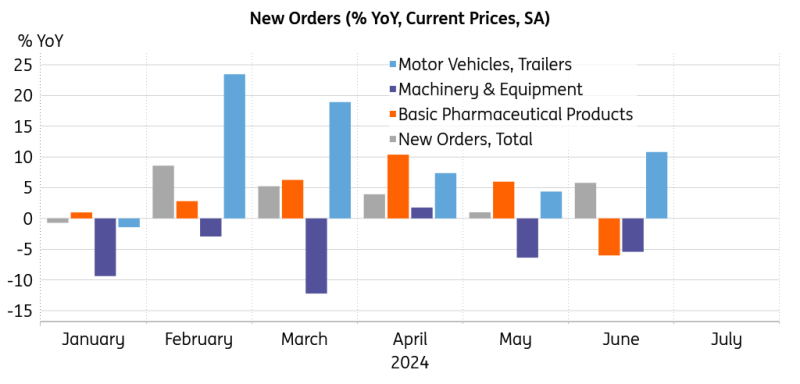

On a positive note, the value of new orders at current prices rose by 4.1% YoY, with new orders from abroad adding 4.8% and domestic new orders up 2.8% from a year earlier. The automotive sector was the main driver of the acceleration in new orders, with an average annual increase in 2Q of 7.6%, which was above the historical average observed between 2016 and 2019. However, the weakness in the Czech industrial sector is still ongoing when gauged by output and employment. The average number of registered employees decreased by 2.1% from a year earlier, while average annual wage growth in industry decelerated to 3.5% YoY in June.

New orders accelerated with automotive in the lead

Dichotomy between industry and households continues

Overall, the picture of industrial performance in June is not all bad news, despite the negative surprise in the headline annual figure. New orders seem to have gained ground, providing a positive signal for future performance. Wage cost growth eased, which aligns with our view that the prolonged malaise in manufacturing should put a lid on lofty wage growth. The dichotomy between industry and households in the Czech economic rebound remains tangible, with continued strength in retail spending on the one hand and weak industrial output on the other. The critical question is whether the recent downward trend in industrial production has now been broken. Or will this spark of hope be extinguished by the German economy's weakness and the recent upsurge in uncertainty surrounding the global economic outlook?

Czech industry treads water

Construction output disappointed, as it fell 10.2% annually in June and declined by 0.8% from the previous month. That said, the indicative value of building permits issued fell 5.6% from a year earlier, and average wage growth in the construction segment softened to 5.7% YoY in June.

The foreign trade surplus surprised positively

According to preliminary data, the balance of foreign trade in goods at current prices ended with a surplus of CZK29.3bn in June, which was CZK11.2bn higher than the previous year. The overall balance of foreign trade in goods was favourably influenced primarily by a smaller deficit in trade in chemicals, oil, and natural gas. The positive balance increased for electrical equipment and motor vehicles. Considering the export and import side, most segments recorded an annual decline. In June, exports fell 4.2% YoY, while imports declined even more, by 7.3% from a year earlier. Meanwhile, exports added 3.4% and imports 0.9% from the previous month in June on a seasonally adjusted basis. Overall, the foreign trade data suggests a positive contribution of net exports to 2Q economic performance.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article