Czech core inflation hinges on strong spending pass‑through

- 15 January

- Czech Republic

Real retail sales were strong in November, confirming our view that the recent quiet spell was only an intermezzo before rising real incomes lifted spending in the run-up to Christmas. The interplay between declining energy prices, ample spending, and core inflation will shape the Czech National Bank's next steps. We opt for one cut, but it's a close call

Retail sales move into their most fruitful years

Czech real retail sales excluding automotives rose 4.6% year-on-year and 0.8% month-on-month in November. Sales of motor vehicles increased by 0.2% YoY but fell 0.5% MoM. Purchases grew across all product groups in stores, except those selling predominantly computer and communication equipment and household products. Real sales of non-food goods gained 6.3% YoY, while fuel sales increased by 6.0% YoY, and food purchases by 1.1% YoY in November. When examining levels, real retail sales surpassed pre-pandemic levels for the first time.

Solid real income is translating into robust spending

The November pickup aligns with our view that Christmas preparations would break the stretch of stagnation seen from April to October. The resources are there, with annual real wage gains averaging 4.6% from the start of 2024 onwards. Indeed, the 4.6% rate in real retail sales points to strong household budgets, with spenders not afraid to use them. The economy expanded by 3.5% on average during the fruitful years of 2016-19, with annual retail sales growth averaging 4.8%. That said, we might be heading in that direction this year, as households will benefit from reduced energy bills.

Spending and core inflation interplay key to CNB

Once again, we highlight the twofold situation in the price domain: headline inflation will likely fall well below the target in January and stay there over the year, while core inflation will remain elevated, fostered by upbeat discretionary spending. It is not certain which will prevail: the deflationary effect from lower energy prices, even for businesses, or the inflationary effect linked to more free cash channelled to discretionary spending. Particularly as industry is just starting to rebound and hire after three years of pain and stagnation. The output gap will turn neutral next quarter, opening the door to positive territory thereafter, so the opportunity for firms to use the tailwinds and boost their margins is there.

Two different worlds for headline and core: we've seen that before

We expect core inflation to average 2.6% this year and decelerate to 2.4% in the second half, though this is on paper. The imbalances in the residential market are set to persist: demand should exceed supply, driving prices higher and boosting rents as part of the CPI consumer basket. Annual growth in house offer prices slowed slightly to 16.9% in the last quarter of the year, but the quarterly dynamic remained elevated at 2.4%, which will shape imputed rent dynamics early this year. That said, imputed rent growth picked up in both monthly and annual terms in December, reaching 5% YoY.

The disinflationary novelties for this year are the pronounced declines in regulated and fuel prices, along with the muted dynamics in food prices. Indeed, persistently low global energy prices, combined with the strong koruna, allowed energy distributors to reduce end-prices for both electricity and natural gas. Government subsidies on household electricity prices as of the start of the year are pushing regulated price dynamics into an even steeper decline. At the same time, lower energy prices for businesses represent a positive supply shock, typically leading to higher output at lower prices. In contrast, lower energy bills for households imply more relaxed budgetary constraints and more cash to spend on discretionary items, mostly part of core inflation.

Regulated and food prices bring headline down

One cut for now, but a close call

Considering the forecast for food prices, we have implemented a new, hopefully more robust, equation for food inflation, as the preliminary food prices survey will no longer be published. Anyway, not a big loss, since it had been getting increasingly messy since mid-2022. It is now replaced by producer prices in agriculture, for which Brent crude and wheat prices, along with FX, serve as exogenous variables. At the same time, the weights in the consumer basket will likely be adjusted in January, so we face the usual 'shaky' January – even at the start of a new quarter century.

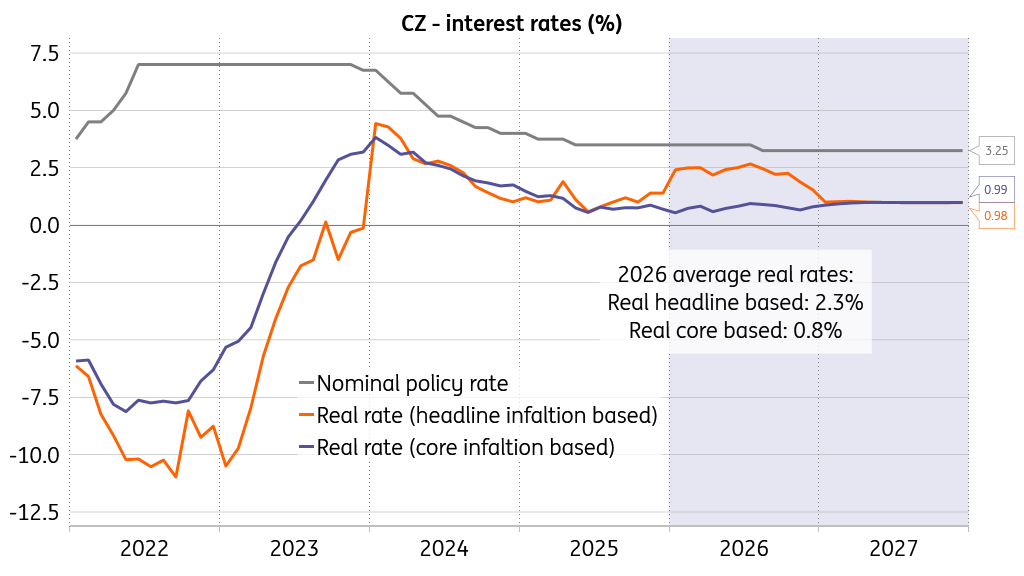

With headline inflation below the target this year and close to it next year, the interplay between low energy costs, ample spending, and core inflation will determine the next CNB's next move. For now, we see one summer cut as the most likely outcome, since the real interest rate, at 2.3% on average this year, seems a bit too restrictive. And we still take the position that the downward secondary effects on core inflation will marginally dominate the upward pressure from the extra spending power.

Ample real rate when measured against headline inflation

However, the odds for the other viable option, just sitting things out at 3.5%, are uncomfortably close. Indeed, you can always point to the robust economic expansion, the positive output gap, the risk of labour market re-tightening, inflation close to target in 2027, the forward-looking CNB, and hey presto! And yes, we have a soft spot for fans of the two-tailed heavy probability distribution – those favouring either no cut at one end or a one-two punch of cuts in March and August at the other. In the end, it’s just a matter of choosing your side, bearing in mind the old saying: to rule is to decide.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more