Czech consumers see a strong start to 2024’s final quarter

Czech real retail sales picked up in October, exceeding market expectations. Given the strong prints we’ve seen for household consumption expenditure and both nominal and real wage growth as of late, we’re inclined to think the country’s economic rebound is on track – at least from the consumption perspective

Retail sales suggest consumption is humming

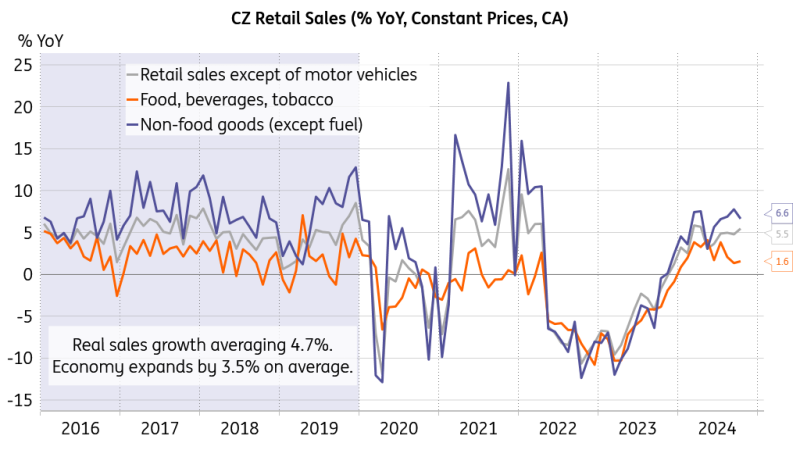

Czech real retail sales increased by 5.5% year-on-year in October and by 0.6% month-on-month. Sales and repairs of motor vehicles were up 2.3% YoY and 0.2% MoM. Both signal a good entry to the year's final quarter for the consumer, better than expected by market participants.

In annual terms, fuel sales rose by 12.2% in October, non-food goods by 6.6%, and food by 1.6%. The pickup in annual real retail sales growth in October was largely driven by a pickup in fuel sales, while the annual dynamic in non-food goods softened from its previous peak. When compared to the previous month, stronger sales were recorded in all main segments: fuel, non-food, and food. Online stores were again the frontrunners in sales gains.

Strong spending - such as in good times

The Czech spenders' strong entry to the final quarter suggests a decent outlook for a continued economic rebound, at least from the side of consumption.

We see higher-than-expected household consumption, more potent nominal and real wage growth, and now also upbeat retail spending. It looks like Czech consumers are enjoying the more relaxed budgetary constraints and are not afraid to continue closing the gap in consumption from pre-pandemic levels that still lingers. We see the Czech economy expanding by 0.9% this year, with its recovery gaining traction over the next year to add 2% in real GDP terms.

If you talk the talk, you better walk the walk

With the still-tight labour market and somewhat restrained supply side, this is a pull factor for consumer prices, when the appetite for spending will likely be met with that for price hikes. The question is whether the sequence of higher wages, higher spending, and higher price tags is entering into a feedback loop mode. And if that is the case, the next question is whether it will remain constrained or can start getting out of hand.

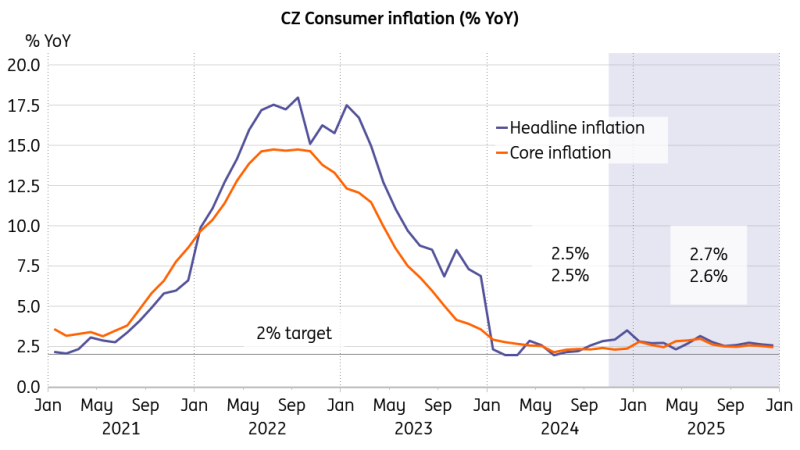

Our inflation forecast for next year is 2.7% for the headline rate and 2.6% for the core rate, which doesn't seem that far from the target.

However, we believe that central banks will soon come under scrutiny over what they mean by inflation being on target, in a more general link to their mandate of maintaining price stability. Is 2% inflation the goal? Or is it somewhere above 2.5%, the target inching further down the monetary policy horizon?

Of course, verbal communication will state the promised 2%. But if you talk the talk, you better be able to walk the walk.

Inflation to remain above the target

Such considerations will be in focus for policymakers during the upcoming meetings in December, February, and perhaps beyond. Our base case scenario is that board members will give themselves the benefit of seeing January’s inflation breakdown before they think about carrying on with further rate reductions. With inflation above the 3% threshold in December and an outlook of above-target inflation over the coming year, only January will show whether it brings another casus belli.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article