Credit Q&A: where do we go from here?

- 27 January 2023

- Credit

Credit markets have been rather constructive over the past couple of months, but have they become too tight? Where does credit go from here? We tackle some of the main questions being asked, illustrate where we see spreads going, and identify where there is value in credit

What are some recent market considerations?

A cry for yields and spreads started in early November – could it be that the credit market read our 2023 outlook (23 calls for 2023: A kind of magic)? – and we have seen a very positive and constructive credit market. EUR spreads have seen around 33bp tightening, alongside substantial fund inflows. After a year of mostly outflows, amounting to 7% year-to-date in October, there was a full retracement with flows ending the year marginally positive. Subsequently, the inflows have persisted to the tune of 2.9% over the past four weeks.

Supply has been rather strong at the beginning of this year, with corporate supply totalling €34bn, financials a substantial €58bn, and covered bonds a significant €37bn. Despite the influx of supply, spreads saw no weakness from indigestion. In fact, new issues were absorbed well by the market, with decent demand, oversubscription and rather low new issue premiums.

Where do you see credit spreads going from here?

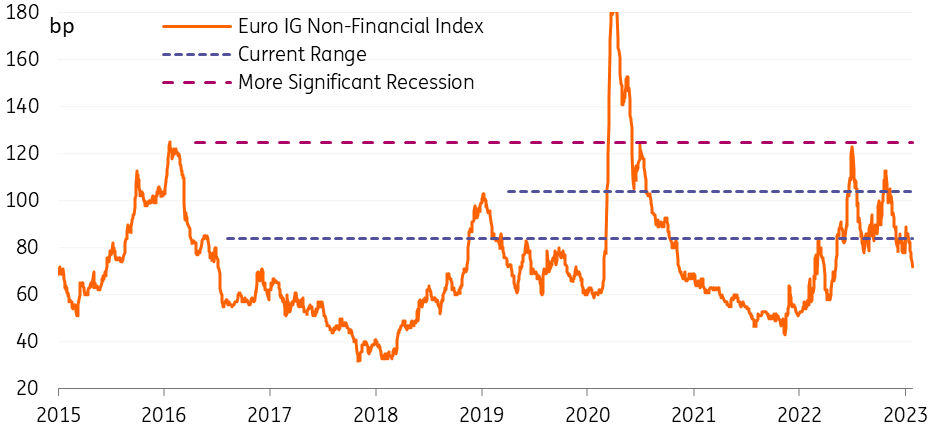

Corporate spreads are now sitting at the very bottom of the trading range, while financials are slightly wider than the bottom end of the range, as illustrated in the charts below. We feel spreads are somewhat tight/expensive at these levels considering the significant risks (potential volatility) and negative factors still very much present in the market. Thus, we struggle to see spreads tightening much more from this point.

The outperformance of cyclical/high beta sectors such as leisure, real estate, manufacturing and automotive proves the point that the market is being driven by yield and spread hunger rather than the all-important issuer or sub-sector selection. As such, we see room for widening but are wary of betting strongly against a positive market, particularly with such attractive yields and inflows. A move below the current trading range creates the ideal opportunity over the next few weeks to offload some of the outperforming segments mentioned above. Conversely, any widening will offer areas of more value within the credit space.

EUR IG non-financial spread range

EUR IG financial spread range

Is there any value left in credit?

In our outlook, we described the magic in credit markets to be valuations, valuations and valuations, while spreads are indeed tighter now we still do see some value in selective areas. The economic environment seems to show early signs of a less benign outlook and inflation in the US at least looks to be turning the corner, thus we remain constructive for credit markets in 2023, although it becomes more about carry than spread tightening. Value though is selective, the driver is on a company-by-company basis, mostly on the shorter end of the curve and selectively on subordinated instruments.

What is a bigger risk for the coming weeks? Tightening or a correction?

The bigger threat is certainly a squeeze as supply dries up going into full-year results-related black-out periods. Next week will also be a busy week for the central banks. Meantime mutual fund flow inflows continue and asset managers have been putting liquidity to work, and all that is accompanied by the current lack of availability of paper (ECB or CSPP holds about 25% of all non-financial outstanding). This squeeze is set to further reduce risk/returns and thus we would look to limit exposure to cyclical names and sectors.

What effect will quantitative tightening have on credit?

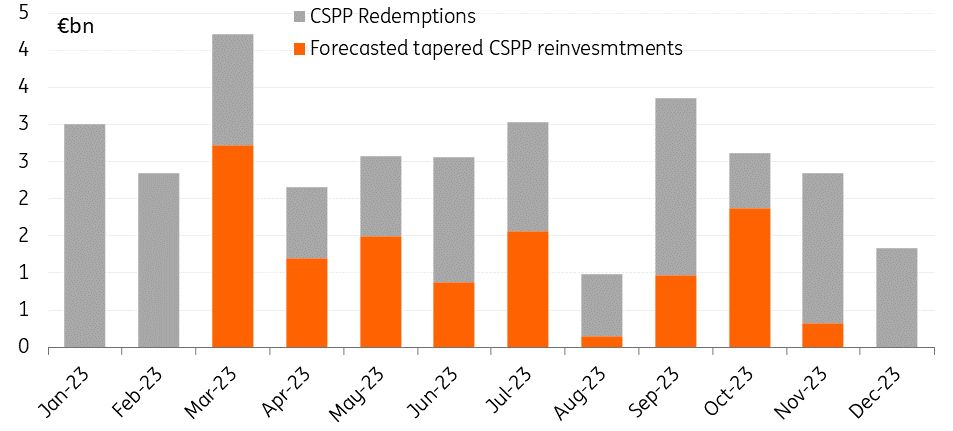

Amongst the list of risk factors and negative drivers is quantitative tightening. The ECB has already announced the tapering of CSPP (corporate sector purchase programme), with a €15bn reduction in APP (asset purchase programme) per month starting in March (with more details to follow at the February meeting).

We foresee the following:

- The lower level of support could add to the turbulence and increase volatility, potentially reprice spreads wider, ultimately adding more value to credit.

- Should there be even faster tapering then it will change the positive technical further and lead to spread widening in the case of faster tapering come July or an abrupt stop. Active selling of holdings will clearly have much more negative implications on spreads.

Forecasted CSPP reinvestments

What does tapering mean for the decarbonising of the ECB’s portfolio?

The tapering of CSPP sparks the debate regarding decarbonising of the ECB’s holdings. Of course with the reduction and eventual end of reinvestments of APP, the efficiency of decarbonising diminishes. As a result, last week the ECB’s Isabel Schnabel discussed the potential move from a flow-based to a stock-based tilting approach. This means the ECB may begin to sell bonds from corporates it considers as scoring low on its scoring system, in order to buy higher-scoring corporates and ESG (environmental, social, and governance) bonds.

The ECB’s ESG scoring system is not public nor are its assigned scores per corporate, thus it remains too much of a black box, but the scoring is based on three parameters; past carbon emissions, future carbon emissions, and the openness and availability of information by the corporate. Therefore, it is hard to predict exactly which names/bonds the ECB may sell, and we will need more information, such as how to account for renewable strategies and transition initiatives. It is likely to be more talk than action but the talk could still create underperformance of any carbon-intensive names and sectors as a result, the CSPP portfolio is simply too sizeable.

Are certain sectors getting too expensive?

We have seen some larger tightening in higher beta sectors in recent weeks, many of which we would still remain cautious of. Our sector selection has not changed; we dislike energy-intensive sectors, inflationary sensitive sectors, sectors that may see a drop in cash buffers, sectors that are more heavily reliant on CSPP and sectors with supply chain shortages. Some of these sectors such as leisure and real estate have been the best performing, we see this as an opportunity to reduce exposure to these sectors, particularly on the long end of the curve.

What is the favoured segment of the liability structure?

This view has not changed, we still see covered bonds as expensive and expect to underperform and widen a bit more in the first half of 2023, while we prefer senior debt, specifically bail-in senior, which has scope to tighten, particularly if the ECB’s rate-hiking cycle comes to an end and the prospects supporting future lower underlying yield levels become firmer. We also see value in callable T2 bonds but on a name-by-name basis, while we find bullet T2 expensive, trading close to Bail-in.

Does the quick start in financial supply mean a lot more issuance to come in 2023?

Looking into 2023 financials, bond supply is likely to face another strong year. For the banking sector, covered bonds remain the main funding alternative, with higher interest rates and as a substitute for collateralised central bank funding. We expect unsecured bank bond funding to edge up. In volatile market conditions, the funding split is likely to remain geared toward tighter spread funding alternatives including covered and preferred senior. Once market conditions improve, loss absorption eligible paper should see more activity.

Is there still value left in corporate hybrids?

We do believe there is selective value left in hybrids but it is far more limited now. We continue to like the frequent issuers with established curves and a proven track record in support of the product, such as Telefonica. Buying back the short-end under the 10% rule helps the attractiveness of that segment. We are, however, still worried about the infrequent hybrid issuers and real estate hybrids.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more